What Are Cryptocurrencies? Beginner Guide 2026

— By Tony Rabbit in Tutorials

Cryptocurrencies explained for beginners: what they are, how they are used, how they differ from traditional money and which categories matter in 2026.

What are cryptocurrencies? They are digital assets that use cryptography and distributed networks to record ownership and move value. Some are designed mainly for payments, others power smart contract platforms, stablecoins, DeFi systems, or tokenized communities.

This page focuses on the definition, main categories, and practical uses of cryptocurrencies. If you want the deeper technical flow, including blockchain records, transaction verification, mining, staking, and gas fees, read our step-by-step guide to how cryptocurrencies work.

Think of cryptocurrency as digital cash that you can send to anyone in the world without needing a middleman like a bank or payment processor. Transactions are processed by a distributed network of computers (called nodes), and the rules governing the system are enforced by code rather than by people.

Types of Cryptocurrencies

Key Properties of Cryptocurrency

Several fundamental characteristics make cryptocurrencies unique compared to any form of money that came before them:

Decentralization: No single authority controls a cryptocurrency network. Instead, thousands of computers around the world maintain copies of the ledger and validate transactions through consensus mechanisms. This removes the need to trust a central institution.

Transparency: All transactions on public blockchains are visible to anyone. You can look up any wallet address and see its entire transaction history. While wallet addresses are pseudonymous (not directly tied to real-world identities), the flow of funds is fully auditable.

🔑 Key Point

Understanding this concept is fundamental to navigating the crypto ecosystem. Take your time with each section before moving on.

🔑 Key Point

Understanding this concept is fundamental to navigating the crypto ecosystem. Take your time with each section before moving on.

Immutability: Once a transaction is confirmed and added to the blockchain, it cannot be altered or reversed. This prevents fraud and double-spending without relying on a central authority to enforce the rules.

Programmability: Many modern cryptocurrencies support smart contracts, which are self-executing programs stored on the blockchain. These enable everything from automated lending to decentralized exchanges, forming the backbone of what is known as decentralized finance (DeFi).

Finite Supply: Many cryptocurrencies have a capped supply written into their code. Bitcoin, for example, will never have more than 21 million coins. This scarcity model contrasts sharply with fiat currencies, which central banks can print in unlimited quantities. Understanding the economics behind token supply is a discipline known as tokenomics.

Permissionless Access: Anyone with an internet connection can create a cryptocurrency wallet and start sending or receiving funds. There are no applications, credit checks, or geographic restrictions. This is particularly significant for the estimated 1.4 billion adults worldwide who remain unbanked.

A Brief History of Cryptocurrency

The story of cryptocurrency did not begin overnight. It was the result of decades of research in cryptography and digital cash systems. Here is how the timeline unfolded.

🔑 Key Point

The crypto ecosystem moves fast. What matters is understanding the fundamentals - those do not change regardless of market conditions.

The Pre-Bitcoin Era (1980s to 2008)

Cryptographer David Chaum introduced the concept of digital cash with DigiCash in 1989. Later projects like b-money (by Wei Dai) and Bit Gold (by Nick Szabo) explored decentralized digital currency concepts in the late 1990s. While none of these projects gained mainstream traction, they laid the intellectual groundwork for what was to come.

Bitcoin Is Born (2009)

In October 2008, a pseudonymous individual (or group) named Satoshi Nakamoto published a whitepaper titled "Bitcoin: A Peer-to-Peer Electronic Cash System." On January 3, 2009, the Bitcoin network went live with the mining of the genesis block. Bitcoin introduced the world to a working decentralized digital currency, solving the long-standing "double-spend" problem without needing a trusted third party.

🔑 Key Point

The crypto ecosystem moves fast. What matters is understanding the fundamentals - those do not change regardless of market conditions.

The Rise of Altcoins (2011 to 2014)

Bitcoin's open-source code inspired the creation of alternative cryptocurrencies, commonly called altcoins. Litecoin launched in 2011 as a faster alternative to Bitcoin. Ripple (XRP) followed in 2012, targeting cross-border payments for financial institutions. Dozens of other projects emerged during this period, each attempting to improve on Bitcoin's design.

Ethereum and Smart Contracts (2015)

Vitalik Buterin launched Ethereum in July 2015, introducing a blockchain that could execute arbitrary programs called smart contracts. This was a game-changer. Ethereum turned blockchain from a simple payment ledger into a programmable platform capable of hosting decentralized applications (dApps). It opened the door to tokenized assets, decentralized exchanges, and entirely new economic models.

The ICO Boom and Bust (2017 to 2018)

Ethereum's ERC-20 token standard made it easy for anyone to launch a new cryptocurrency. This led to the Initial Coin Offering (ICO) craze of 2017, where thousands of projects raised billions of dollars. Bitcoin hit nearly $20,000 in December 2017. The subsequent crash in 2018 wiped out much of the speculation, but the technology continued to mature behind the scenes.

🔑 Key Point

This is where most people stop reading. If you made it this far, you understand more than 90% of crypto users. The next step is to actually try it with a small amount.

The DeFi Summer (2020)

In 2020, decentralized finance exploded. Protocols like Uniswap, Aave, and Compound enabled users to trade, lend, and borrow crypto without intermediaries. Yield farming became a popular way to earn returns on crypto holdings. Total value locked (TVL) in DeFi went from under $1 billion at the start of 2020 to over $15 billion by year's end.

NFTs, Institutional Adoption, and Layer 2s (2021 to 2023)

Non-fungible tokens (NFTs) captured mainstream attention in 2021. Institutional investors like Tesla and MicroStrategy added Bitcoin to their balance sheets. Layer 2 scaling solutions began addressing the high gas fees that had plagued Ethereum users. By 2023, the industry was recovering from the collapses of several centralized entities like FTX and Terra/Luna, leading to stronger demands for regulation and transparency.

Spot ETFs and Mainstream Integration (2024 to 2026)

The approval of spot Bitcoin ETFs in the United States in January 2024 marked a watershed moment, bringing billions of dollars of institutional capital into the market. Ethereum spot ETFs followed later that year. By 2026, cryptocurrency has become an accepted part of the global financial landscape, with clear regulatory frameworks emerging in major economies and integration with traditional banking becoming more common.

How Cryptocurrency Differs From Fiat Money

Understanding the differences between cryptocurrency and traditional fiat currency is essential for anyone entering this space. Here is a direct comparison of their key characteristics.

🔑 Key Point

This is where most people stop reading. If you made it this far, you understand more than 90% of crypto users. The next step is to actually try it with a small amount.

Issuance and Control: Fiat currencies like the US dollar, euro, or Japanese yen are issued and regulated by central banks. Governments can print more money, set interest rates, and implement monetary policy. Cryptocurrencies, by contrast, follow rules encoded in software. Bitcoin's supply schedule is predetermined and cannot be changed by any single entity.

Transaction Processing: Fiat transactions typically go through banks, payment processors, or clearinghouses, which can take days for international transfers and charge significant fees. Crypto transactions are processed on decentralized networks and can settle in minutes or seconds, regardless of geographic boundaries. A Bitcoin transfer from New York to Tokyo takes the same amount of time as one across the street.

Inflation Model: Central banks regularly increase the money supply, which can lead to inflation that erodes purchasing power over time. Many cryptocurrencies have fixed or decreasing supply schedules. Bitcoin's issuance rate halves approximately every four years through a process called "halving," making it inherently deflationary in its supply model.

Privacy and Surveillance: Bank transactions are monitored by financial institutions and can be accessed by governments. Cryptocurrency transactions on public blockchains are pseudonymous. While they are traceable on-chain, they are not automatically linked to real-world identities unless the user connects their identity to a wallet address through an exchange or other service.

Accessibility: Opening a bank account requires identification documents, proof of address, and often a minimum deposit. Creating a crypto wallet requires nothing more than an internet connection. This fundamental difference makes cryptocurrency a powerful tool for financial inclusion in regions with limited banking infrastructure.

Types of Cryptocurrencies: Coins vs. Tokens

Not all cryptocurrencies are created equal. The ecosystem includes several distinct categories, each serving different purposes.

Layer 1 Coins (Native Cryptocurrencies)

These are the native currencies of their own blockchain networks. They are used to pay transaction fees, reward validators, and serve as the base currency of their ecosystem. Examples include Bitcoin (BTC), Ether (ETH), Solana (SOL), and BNB. Each of these coins powers its own independent blockchain.

Tokens (Built on Existing Blockchains)

Tokens are created on top of existing blockchains using smart contracts. The most common standard is Ethereum's ERC-20, but other chains like Solana and BNB Chain have their own token standards. Tokens can represent almost anything: access rights, governance votes, real-world assets, or purely speculative value.

Utility Tokens

Utility tokens provide access to a specific product or service within a blockchain ecosystem. For example, Chainlink's LINK token is used to pay for oracle services that feed external data to smart contracts. Filecoin's FIL token is used to pay for decentralized file storage. The value of utility tokens is tied to the demand for the service they provide.

Governance Tokens

Governance tokens give holders voting rights over protocol decisions. If you hold Uniswap's UNI token, for example, you can vote on proposals that determine how the protocol evolves, including fee structures, treasury allocations, and technical upgrades. Governance tokens are a core component of decentralized autonomous organizations (DAOs).

Stablecoins

Stablecoins are designed to maintain a steady value, typically pegged to the US dollar. They bridge the gap between volatile crypto assets and stable fiat currencies. USDT (Tether), USDC (Circle), and DAI (MakerDAO) are the most widely used stablecoins. They are essential for trading, DeFi, and as a store of value during market downturns.

Memecoins

Memecoins are cryptocurrencies that originate from internet culture, jokes, or viral trends rather than technical innovation. Dogecoin (DOGE) and Shiba Inu (SHIB) are the most well-known examples. While some memecoins have achieved significant market capitalizations, they are generally considered highly speculative and carry substantial risk. Their value is driven primarily by community sentiment and social media hype rather than underlying technology or utility.

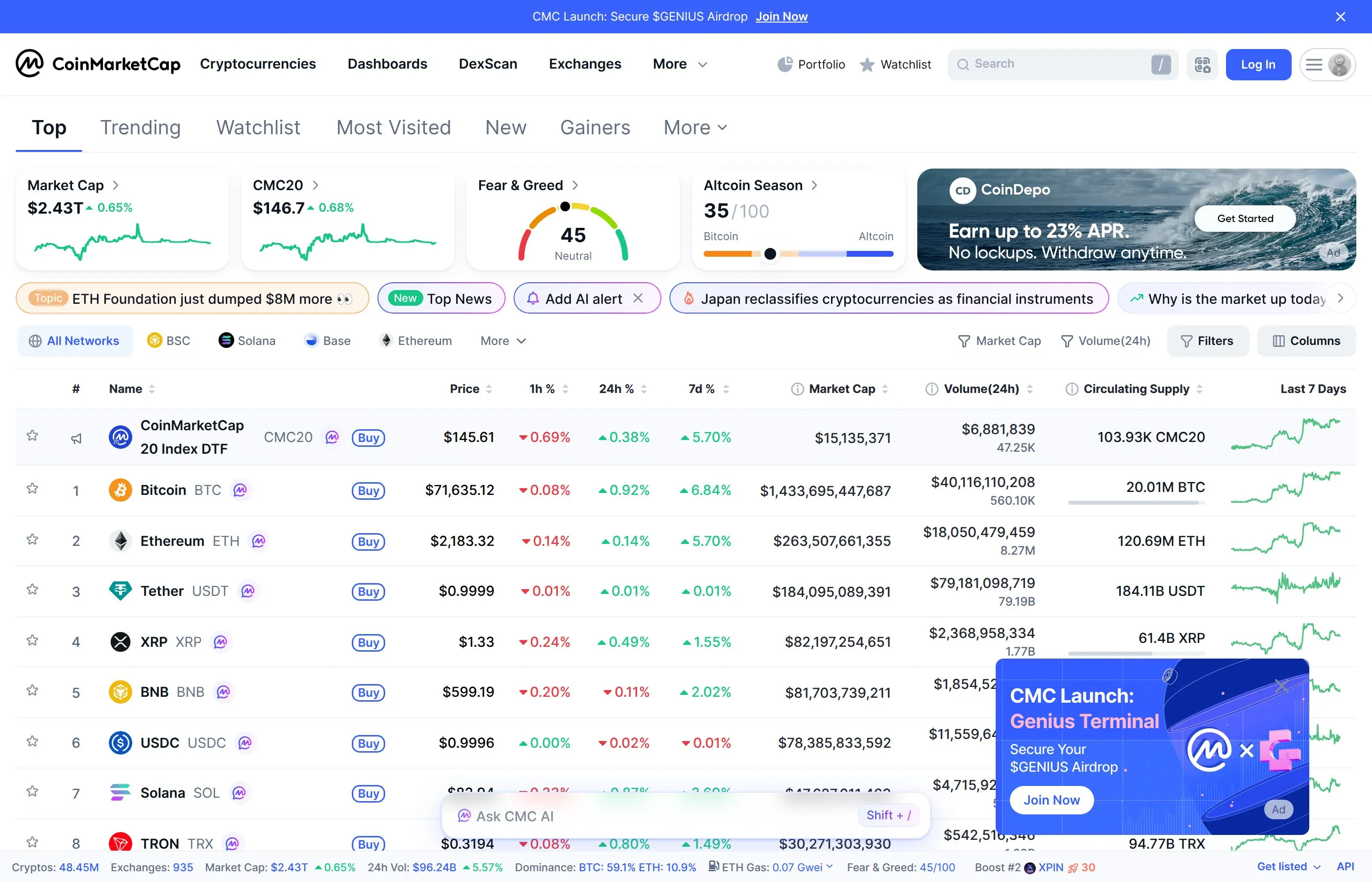

The Biggest Cryptocurrencies Explained

Let us take a closer look at the most significant cryptocurrencies by market capitalization and their roles in the broader ecosystem.

Bitcoin (BTC)

Bitcoin is the original cryptocurrency and remains the largest by market cap. It functions primarily as a store of value and a medium of exchange. Often called "digital gold," Bitcoin's appeal comes from its fixed supply of 21 million coins, its robust security model (secured by the largest proof-of-work mining network in the world), and its first-mover advantage. Bitcoin is the most widely held cryptocurrency among both retail and institutional investors, and it is the asset tracked by the first spot cryptocurrency ETFs.

Ethereum (ETH)

Ethereum is the leading smart contract platform, hosting the vast majority of DeFi protocols, NFT marketplaces, and decentralized applications. It transitioned from proof-of-work to proof-of-stake in September 2022 (an event called "The Merge"), dramatically reducing its energy consumption. Ethereum's ecosystem includes thousands of tokens and applications, making it the foundational infrastructure layer for much of the crypto economy.

Solana (SOL)

Solana is a high-performance Layer 1 blockchain known for its speed and low transaction costs. It can process thousands of transactions per second at a fraction of a cent per transaction. This makes it popular for applications requiring high throughput, including decentralized exchanges, gaming, and consumer-facing applications. Solana's ecosystem has grown rapidly, particularly in the areas of DeFi and NFTs.

BNB (BNB)

BNB is the native token of the BNB Chain ecosystem, which was created by the cryptocurrency exchange Binance. Originally launched as an ERC-20 token on Ethereum, BNB migrated to its own blockchain. It is used to pay trading fees on Binance (at a discount), fuel transactions on BNB Chain, and participate in token launches. BNB Chain is one of the most active blockchains by transaction volume.

XRP (XRP)

XRP is designed for fast, low-cost cross-border payments. The XRP Ledger can settle transactions in three to five seconds, making it one of the fastest payment networks in cryptocurrency. Ripple, the company most closely associated with XRP, has partnerships with financial institutions around the world. After years of legal battles with the SEC, XRP's regulatory situation has become clearer, contributing to renewed institutional interest.

How to Get Started With Cryptocurrency

If you are new to crypto, the process of getting started can feel overwhelming. Here is a step-by-step breakdown to help you navigate your first steps safely.

Step 1: Learn the Fundamentals

Before spending any money, invest time in education. Understand how blockchain works, what gives different cryptocurrencies their value, and the risks involved. Learning how to do your own research (DYOR) is one of the most valuable skills you can develop in this space. Do not rely solely on social media influencers or friends for investment advice.

Step 2: Set Up a Wallet

A cryptocurrency wallet is the software (or hardware) that stores your private keys and allows you to send and receive crypto. There are several types to choose from. Hot wallets (software wallets like MetaMask or Trust Wallet) are free, easy to use, and connect to your browser or phone. Cold wallets (hardware devices like Ledger or Trezor) store your keys offline, providing the highest level of security. For a detailed walkthrough, check out our guide on how to create a crypto wallet. If you plan to hold significant amounts, consider investing in one of the best cold wallets available.

Step 3: Choose an Exchange or On-Ramp

To convert fiat money into cryptocurrency, you will need to use an exchange or on-ramp service. Centralized exchanges (CEXs) like Coinbase, Kraken, and Binance are the most beginner-friendly option. They accept bank transfers, credit cards, and other payment methods. Decentralized exchanges (DEXs) like Uniswap and Jupiter let you trade directly from your wallet without creating an account, but they require you to already have crypto. Our guide on how to buy cryptocurrency walks through the entire process.

Step 4: Make Your First Purchase

Start small. You do not need to buy a whole Bitcoin or Ethereum. Cryptocurrencies are divisible, so you can buy $10, $50, or $100 worth. Many experienced investors recommend dollar-cost averaging (DCA), which means buying a fixed amount at regular intervals regardless of price. This strategy reduces the impact of short-term volatility on your overall position.

Step 5: Secure Your Holdings

Security is paramount in crypto because transactions are irreversible. If someone gains access to your private keys, your funds are gone with no recourse. Use strong, unique passwords. Enable two-factor authentication (2FA) on all exchange accounts. Never share your seed phrase (the 12 or 24 word recovery phrase for your wallet) with anyone. Consider moving larger holdings to a hardware wallet for cold storage.

Step 6: Stay Informed

The cryptocurrency market moves fast. Follow reputable news sources, join community forums, and keep up with the projects you have invested in. Understanding market cycles, regulatory developments, and technological upgrades will help you make better decisions over time.

Cryptocurrency Use Cases in 2026

Cryptocurrencies have evolved far beyond simple peer-to-peer payments. Here are the most significant use cases shaping the industry today.

Payments and Remittances

Cryptocurrency enables fast, borderless payments with lower fees than traditional methods. For international remittances, where traditional services can charge 5% to 10% in fees, crypto offers a dramatically cheaper alternative. Stablecoins have become particularly popular for payments because they avoid the volatility associated with assets like Bitcoin. In countries with unstable local currencies, stablecoins serve as a practical dollar-denominated alternative.

Decentralized Finance (DeFi)

DeFi recreates traditional financial services (lending, borrowing, trading, insurance) using smart contracts instead of banks. Users can earn interest on their crypto holdings, take out loans without credit checks, and trade assets 24/7 without intermediaries. By 2026, DeFi protocols collectively hold hundreds of billions of dollars in value, and the sector continues to innovate with real-world asset tokenization and institutional-grade products.

Non-Fungible Tokens (NFTs)

NFTs represent ownership of unique digital (or physical) items on a blockchain. While the speculative frenzy of 2021 has cooled, NFTs have found lasting applications in digital art, gaming, event ticketing, loyalty programs, and proof of authenticity for physical goods. Major brands, sports leagues, and entertainment companies continue to use NFTs for customer engagement.

Gaming and the Metaverse

Blockchain gaming allows players to truly own their in-game assets as NFTs and earn cryptocurrency through gameplay. This "play-to-earn" and "play-and-earn" model has created real economic opportunities, particularly in developing countries. Virtual worlds built on blockchain technology enable users to buy virtual land, create experiences, and participate in digital economies.

Decentralized Identity and Data Ownership

Blockchain-based identity solutions allow individuals to control their own personal data. Instead of relying on centralized databases (which are frequent targets for data breaches), users can store verifiable credentials on-chain and share only the information necessary for a given interaction. This has applications in healthcare, education, employment verification, and government services.

Supply Chain and Provenance

Enterprises use blockchain to track goods from origin to consumer. This is particularly valuable in food safety (tracking contamination sources), luxury goods (verifying authenticity), and pharmaceuticals (preventing counterfeits). The immutable nature of blockchain records provides an auditable trail that all parties in a supply chain can trust.

Tokenization of Real-World Assets (RWAs)

One of the fastest-growing sectors in 2026 is the tokenization of real-world assets. Treasury bills, real estate, commodities, and private equity are being represented as tokens on blockchain networks. This opens up traditionally illiquid and exclusive asset classes to a global pool of investors. Major financial institutions including BlackRock, Goldman Sachs, and JPMorgan have launched tokenized asset products.

Risks of Investing in Cryptocurrency

While the potential rewards of cryptocurrency are significant, so are the risks. Anyone entering this market should understand the following dangers.

Volatility: Cryptocurrency prices can swing 10%, 20%, or even 50% in a single day. While Bitcoin and Ethereum have become somewhat less volatile as they have matured, smaller altcoins can experience extreme price swings. Never invest more than you can afford to lose.

Security Risks: Hacks, exploits, and scams are ongoing threats. Smart contract vulnerabilities can lead to millions of dollars being drained from DeFi protocols. Phishing attacks target individuals through fake websites, emails, and social media messages. Personal security practices are your primary line of defense.

Regulatory Risk: While regulation has become clearer in many jurisdictions by 2026, the rules are still evolving. Changes in tax law, securities classification, or outright bans in certain countries can impact the value of your holdings. Understanding the tax implications of cryptocurrency in your jurisdiction is essential.

Project Failure: The vast majority of cryptocurrency projects that launch will eventually fail. Poor management, lack of product-market fit, insufficient funding, or technical vulnerabilities can all lead to a token becoming worthless. This is why thorough research before investing in any project is critical.

Liquidity Risk: While major cryptocurrencies like BTC and ETH are highly liquid, smaller tokens may have thin order books. This means you might not be able to sell your position at the price you want, especially during market downturns when everyone is trying to sell at the same time.

Irreversible Transactions: Unlike credit card payments or bank transfers, cryptocurrency transactions cannot be reversed. If you send funds to the wrong address or fall victim to a scam, there is no customer service department to call. This places a higher burden of responsibility on the individual user.

Cryptocurrency Regulation in 2026

The regulatory landscape for cryptocurrency has matured significantly. Here is where things stand in the major markets.

United States

The US has established clearer frameworks for classifying digital assets. The SEC and CFTC have defined jurisdictional boundaries, with the SEC overseeing tokens classified as securities and the CFTC handling those deemed commodities (including Bitcoin and Ethereum). Spot ETFs for both Bitcoin and Ethereum are actively traded, and stablecoin legislation has provided guidelines for issuers. Tax reporting requirements have been tightened, with exchanges now required to issue 1099 forms for user transactions.

European Union

The Markets in Crypto-Assets (MiCA) regulation, fully implemented by 2025, provides a comprehensive framework across EU member states. MiCA covers crypto-asset service providers (CASPs), stablecoin issuers, and token classifications. It has created regulatory clarity that has attracted significant industry investment to the EU.

Asia-Pacific

Regulation varies widely across the region. Japan and Singapore maintain progressive frameworks that encourage innovation while protecting consumers. Hong Kong has positioned itself as a crypto hub with licensing regimes for exchanges and funds. Other markets continue to develop their approaches, with varying degrees of openness to the industry.

What Regulation Means for You

As a cryptocurrency user in 2026, regulation primarily affects you in three ways. First, you will need to complete Know Your Customer (KYC) verification on most centralized exchanges, which means providing identification documents. Second, you are responsible for reporting cryptocurrency gains and losses on your taxes. Third, regulated exchanges and services offer stronger consumer protections than the unregulated alternatives, including custody standards and insurance on deposits.

Pros and Cons of Cryptocurrency

Pros

Financial Sovereignty: You control your own money without depending on banks or governments. No one can freeze your crypto wallet or block your transactions (as long as you hold your own keys).

Global Accessibility: Anyone with internet access can participate. Crypto removes barriers to financial services for billions of people who lack access to traditional banking.

Transparency: Public blockchains provide full auditability. You can verify the supply, distribution, and transaction history of any cryptocurrency at any time.

Innovation: The crypto ecosystem is one of the most rapidly innovating sectors in technology. DeFi, NFTs, decentralized identity, and tokenized real-world assets are just a few of the groundbreaking applications being built.

Potential Returns: Despite its volatility, cryptocurrency has been one of the best-performing asset classes over the past decade. Early adopters of Bitcoin and Ethereum have seen extraordinary returns on their investments.

Programmable Money: Smart contracts enable financial products and services that are impossible with traditional money. Automated lending, decentralized insurance, and programmable payments are just the beginning.

Inflation Hedge: Fixed-supply cryptocurrencies like Bitcoin offer protection against monetary inflation. In countries experiencing hyperinflation, crypto has served as a practical alternative store of value.

Cons

Volatility: Price swings can be extreme, making cryptocurrency unsuitable as a stable store of value for risk-averse individuals.

Complexity: The learning curve is steep. Understanding wallets, private keys, gas fees, and different blockchain networks requires significant time investment.

Security Responsibility: Being your own bank means being your own security team. Lost keys, forgotten seed phrases, and phishing attacks have cost users billions of dollars collectively.

Scams and Fraud: The crypto space attracts bad actors. Rug pulls, Ponzi schemes, and social engineering attacks are common, particularly with smaller, unestablished projects.

Environmental Concerns: While Ethereum's move to proof-of-stake dramatically reduced its energy consumption, Bitcoin's proof-of-work mining still requires significant electricity. The environmental impact remains a point of debate.

Regulatory Uncertainty: Although regulation has improved, rules differ by jurisdiction and continue to evolve. What is legal in one country may be restricted in another.

Limited Consumer Protections: Unlike bank deposits insured by the FDIC (in the US) or similar schemes, crypto held in personal wallets has no government backing if something goes wrong.

How Cryptocurrency Mining and Validation Work

Cryptocurrencies use consensus mechanisms to validate transactions and add them to the blockchain. The two dominant mechanisms are proof-of-work and proof-of-stake.

Proof-of-Work (PoW)

Bitcoin uses proof-of-work, where miners compete to solve complex mathematical puzzles. The first miner to find the solution gets to add the next block of transactions to the blockchain and receives a reward in newly minted Bitcoin (currently 3.125 BTC per block after the 2024 halving). This process requires specialized hardware (ASICs) and significant electricity. The difficulty of the puzzles adjusts automatically to maintain a roughly 10-minute block time, regardless of how much computing power is on the network.

Proof-of-Stake (PoS)

Ethereum and most newer blockchains use proof-of-stake. Instead of mining, validators lock up (or "stake") their cryptocurrency as collateral. The network selects validators to propose and confirm blocks based on the amount they have staked and other factors. Validators earn rewards for honest participation and risk losing their staked funds (called "slashing") if they act maliciously. Proof-of-stake uses a fraction of the energy required by proof-of-work.

Other Consensus Mechanisms

Several alternative approaches exist. Delegated proof-of-stake (DPoS) allows token holders to vote for a limited number of validators. Proof-of-history (used by Solana) creates a verifiable record of time to increase throughput. Proof-of-authority relies on a set of pre-approved validators, sacrificing decentralization for speed. Each mechanism makes different tradeoffs between security, speed, decentralization, and energy efficiency.

Understanding Gas Fees

When you make a transaction on a blockchain, you pay a fee to compensate the validators or miners who process it. On Ethereum and compatible networks, these fees are called gas fees. Gas fees fluctuate based on network demand. When many people are trying to use the network at the same time, fees increase. When the network is quiet, fees drop. Layer 2 solutions like Arbitrum, Optimism, and Base have emerged to process transactions off the main Ethereum chain at a fraction of the cost, making crypto more accessible for everyday use.

Cryptocurrency and Taxes

In most jurisdictions, cryptocurrency is treated as property for tax purposes. This means you owe taxes when you sell crypto for a profit, trade one cryptocurrency for another, or use crypto to buy goods and services. The specific tax rates depend on how long you held the asset and your local tax laws. Keeping accurate records of all your transactions is essential. Many crypto tax software tools can import your transaction history from exchanges and wallets to generate tax reports. For a comprehensive overview, read our crypto tax guide.

Common Cryptocurrency Scams and How to Avoid Them

The irreversible nature of crypto transactions makes the space attractive to scammers. Here are the most common threats and how to protect yourself.

Phishing Attacks: Fake websites, emails, or social media messages that mimic legitimate services and trick you into entering your private keys or seed phrase. Always double-check URLs, bookmark official sites, and never enter your seed phrase on any website.

Rug Pulls: Developers create a token, hype it up to attract investment, and then drain the liquidity pool and disappear with investor funds. Look for audited contracts, locked liquidity, and established team identities before investing in new projects.

Pump and Dump Schemes: Coordinated groups artificially inflate the price of a low-cap token and then sell their holdings, leaving later buyers with losses. Be wary of tokens being aggressively promoted in group chats or on social media by anonymous accounts.

Fake Airdrops and Giveaways: Scammers promise free tokens if you connect your wallet to a malicious website or send crypto to a specific address. Legitimate projects never ask you to send crypto to receive an airdrop.

Impersonation: Scammers impersonate well-known figures in the crypto space (like exchange CEOs or protocol founders) and offer fake investment opportunities. No legitimate figure will ever DM you asking for money or offering guaranteed returns.

The Future of Cryptocurrency

As we move through 2026, several trends are shaping the next chapter of cryptocurrency.

Institutional Integration: The line between traditional finance and crypto continues to blur. Major banks offer crypto custody, trading, and yield products. Tokenized assets are becoming a standard part of institutional portfolios.

Central Bank Digital Currencies (CBDCs): Over 130 countries are exploring or have launched CBDCs. While these are not cryptocurrencies in the decentralized sense, their development is accelerating the world's familiarity with digital money and blockchain infrastructure.

AI and Blockchain Convergence: The intersection of artificial intelligence and blockchain is creating new possibilities, from AI agents that can autonomously transact on-chain to decentralized AI model marketplaces. This convergence is one of the most closely watched trends in the industry.

Improved User Experience: Account abstraction, social recovery wallets, and embedded crypto experiences are making the technology more accessible. The goal is for users to benefit from blockchain technology without needing to understand the technical details, similar to how most people use the internet without understanding TCP/IP.

Cross-Chain Interoperability: Bridges and messaging protocols are making it easier to move assets and data between different blockchains. The future is not one chain to rule them all, but a connected ecosystem of specialized chains working together.

Video Explainer

Watch this video for a visual walkthrough of the concepts covered above.

Frequently Asked Questions

Is cryptocurrency real money?

Yes, cryptocurrency functions as money in many contexts. It can be used to buy goods and services, sent as payment between individuals, and exchanged for fiat currencies on regulated exchanges. While it is not issued by a government, its value is determined by supply and demand in global markets, much like any other asset. Several countries have recognized Bitcoin as legal tender or established frameworks for using crypto in everyday commerce.

How many cryptocurrencies exist?

There are over 20,000 cryptocurrencies listed on tracking sites, though only a few hundred have significant market capitalization and active development. Many tokens are created for experimental purposes, as jokes, or as outright scams. The vast majority of market value is concentrated in the top 20 to 50 projects.

Can I lose all my money in crypto?

Yes, it is possible to lose your entire investment in cryptocurrency. Individual tokens can and do go to zero. Even major cryptocurrencies can experience drawdowns of 50% to 80% during bear markets. Never invest more than you can afford to lose, and diversify your portfolio rather than putting everything into a single asset.

Is cryptocurrency anonymous?

Most cryptocurrencies are pseudonymous, not anonymous. Transactions are recorded on a public ledger and can be traced. While wallet addresses are not directly linked to real-world identities, blockchain analytics firms can often trace the flow of funds. Privacy-focused cryptocurrencies like Monero and Zcash offer stronger anonymity features, but even these are not perfectly untraceable in all circumstances.

What is the best cryptocurrency to buy as a beginner?

Most experts recommend starting with Bitcoin and Ethereum because they are the most established, most liquid, and have the longest track records. Bitcoin is the simplest to understand as a digital store of value. Ethereum offers exposure to the broader smart contract and DeFi ecosystem. After gaining experience with these two, you can research other projects and decide if you want to diversify into altcoins.

Do I need to buy a whole Bitcoin?

No. Bitcoin is divisible to eight decimal places. The smallest unit, called a satoshi (or "sat"), is 0.00000001 BTC. You can buy as little as a few dollars worth of Bitcoin on most exchanges. The same applies to Ethereum and virtually all other cryptocurrencies.

What is a seed phrase and why is it important?

A seed phrase (also called a recovery phrase) is a series of 12 or 24 words generated when you create a cryptocurrency wallet. It is the master key to your funds. If you lose access to your wallet, your seed phrase is the only way to recover it. If someone else gets your seed phrase, they can steal all your funds. Write it down on paper, store it in a secure location, and never enter it on any website or share it with anyone.

What is the difference between a coin and a token?

A coin is the native cryptocurrency of its own blockchain (like BTC on Bitcoin or ETH on Ethereum). A token is a digital asset built on top of an existing blockchain using smart contracts (like USDC or LINK on Ethereum). The distinction matters for understanding how assets interact with their underlying networks and for technical operations like transferring between wallets.

Can cryptocurrency be hacked?

Major blockchain networks like Bitcoin and Ethereum have never been successfully hacked at the protocol level. However, applications built on top of blockchains (like DeFi protocols and exchanges) have been hacked numerous times. Individual users are also vulnerable to phishing, malware, and social engineering attacks. The security of your funds depends on both the strength of the underlying network and your personal security practices.

How do I cash out cryptocurrency to my bank account?

The most common method is to sell your cryptocurrency on a centralized exchange (like Coinbase, Kraken, or Binance) and withdraw the fiat proceeds to your linked bank account. The process typically takes one to three business days for the bank transfer. Some services also offer crypto debit cards that let you spend your holdings directly without manually converting them first.

Is crypto legal?

Cryptocurrency is legal in most countries, including the United States, European Union member states, the United Kingdom, Japan, Australia, and Canada. A small number of countries have imposed outright bans. Regulation varies significantly by jurisdiction, so it is important to understand the specific rules where you live. In most places, while owning and trading crypto is legal, you are required to report gains and pay applicable taxes.

What happens if I send crypto to the wrong address?

Cryptocurrency transactions are irreversible. If you send funds to an incorrect but valid address, there is no way to recover them unless the owner of that address voluntarily sends them back. If you send them to an address that does not exist on that particular blockchain, the funds are typically lost permanently. Always double-check (or triple-check) the recipient address before confirming any transaction, and use test transactions for large amounts.

What is DeFi and should I use it?

Decentralized finance (DeFi) refers to financial services built on blockchain technology that operate without traditional intermediaries. DeFi offers opportunities like earning yield on your crypto, borrowing against your holdings, and trading assets directly from your wallet. However, it comes with risks including smart contract bugs, liquidation risk, and a steep learning curve. Beginners should thoroughly understand the basics of cryptocurrency before exploring DeFi, and should start with small amounts on well-established protocols.

How much should I invest in cryptocurrency?

Financial advisors commonly suggest allocating no more than 5% to 10% of your total investment portfolio to high-risk assets like cryptocurrency. The exact amount depends on your financial situation, risk tolerance, investment timeline, and existing portfolio diversification. The cardinal rule applies: never invest money you cannot afford to lose. Cryptocurrency should complement a broader financial plan, not replace savings, emergency funds, or retirement contributions.

Related Guides

- Top 5 NFT Marketplaces in 2026: Where to Buy and Sell Digital Assets

- What Is an Altcoin: Complete Guide to Alternative Cryptocurrencies (2026)

- How Do Cryptocurrencies Work? Complete Guide 2026

- 10 Best Crypto to Mine 2026: Real Profit per kWh Calculated

- What Is Unstoppable Domains: Web3 Domains, Identity and Digital Ownership (2026)