What Is Convex Finance? CVX & Curve Booster Guide 2026

— By Whatsertrade in Tutorials

Convex Finance boosts Curve LP yields, locks veCRV, powers the Curve Wars and bribes. Full 2026 guide to CVX, vlCVX, cvxCRV and Votium.

If you have ever deposited liquidity on Curve Finance, you have probably noticed something strange: the advertised rewards are much higher than what regular depositors actually earn. The difference comes down to a single mechanic called veCRV, the vote-escrowed version of the CRV token that boosts liquidity provider yields by up to 2.5x. Most users never get that boost because locking CRV for four years to obtain veCRV is an enormous commitment. Convex Finance solved this problem in May 2021 and quickly became one of the most influential protocols in all of decentralized finance (DeFi).

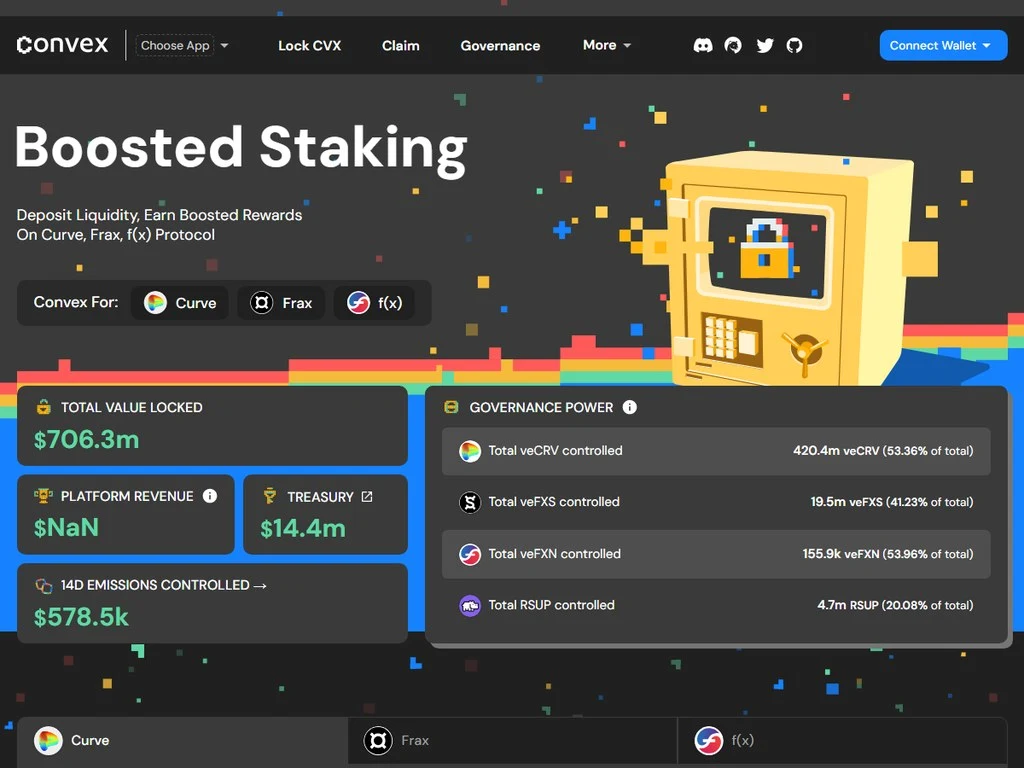

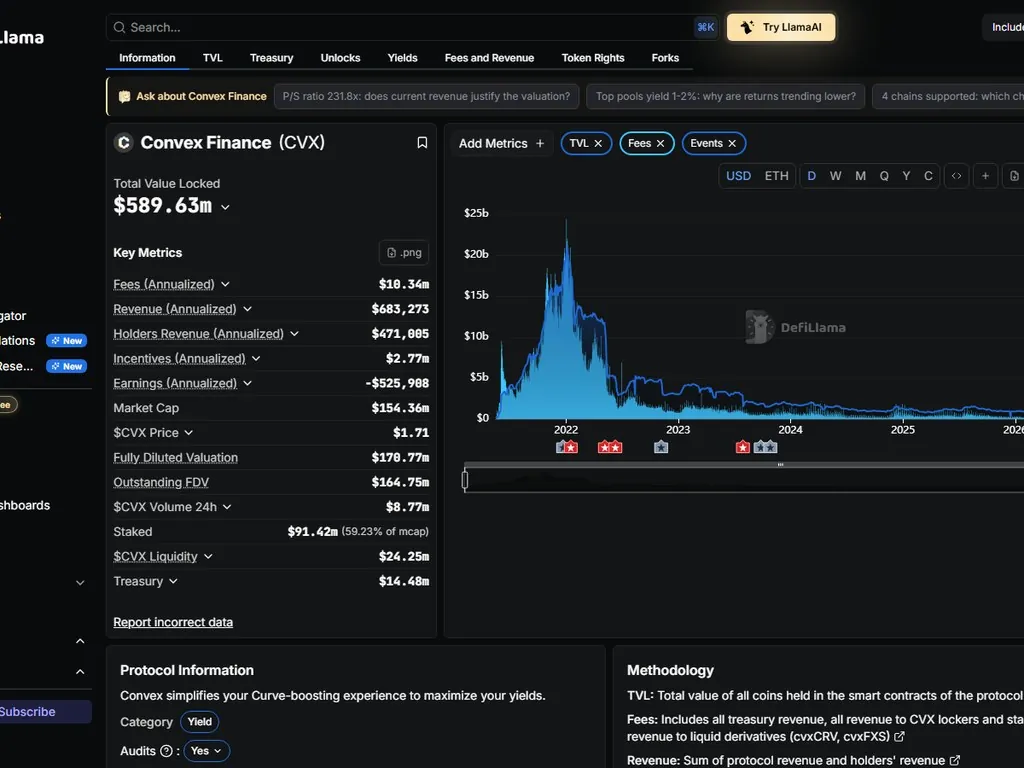

Convex Finance is a yield optimization protocol built on top of Curve. It allows users to deposit their Curve LP tokens, earn boosted CRV emissions, trading fees, and additional CVX rewards, all without having to lock any CRV themselves. By aggregating hundreds of millions of dollars in CRV through a smart locking mechanism, Convex secures the maximum 2.5x boost for every depositor and shares the benefit across its user base. The protocol still holds more than $1 billion in total value locked in May 2026 and remains the largest single voter in Curve governance.

This guide walks through everything you need to know about Convex Finance: how it works, the role of CVX and vlCVX, the Curve Wars that made Convex famous, the Votium bribe economy, how to deposit LP tokens step by step, how Convex integrates with Frax, and where the protocol stands in 2026. You will also find a detailed comparison against Yearn and Stake DAO, a tokenomics breakdown, and a list of honest risks every depositor should weigh before clicking confirm on a transaction.

What Is Convex Finance?

Convex Finance is a DeFi protocol that boosts the yield of Curve liquidity providers and CRV stakers without requiring them to lock CRV directly. Users deposit Curve LP tokens or CRV into Convex, and the protocol aggregates the deposits to obtain the maximum 2.5x veCRV boost, then distributes the enhanced rewards to depositors along with extra CVX tokens.

The protocol launched on Ethereum mainnet on May 17, 2021, exactly five years before this article was written. It was created by an anonymous developer team led by a pseudonymous founder known as C2tP. Within three months Convex had absorbed more CRV than any other protocol in existence, and by late 2021 the protocol controlled more than 50% of all veCRV voting power. That dominance never really faded, and in May 2026 Convex still controls roughly 49% of the veCRV supply through its convex-locked CRV (cvxCRV) treasury.

A Short History of Convex and the Curve Wars

To understand why Convex matters, you have to understand the Curve Wars. Curve Finance, launched in January 2020 by Michael Egorov, became the dominant venue for stablecoin and pegged-asset trading thanks to its low-slippage StableSwap algorithm. In August 2020 Curve introduced the CRV token along with a vote-escrow model: lock CRV for up to four years and receive veCRV, which grants three privileges at once. Boosted LP rewards up to 2.5x, a share of trading fees through 3CRV admin fees, and the right to vote on gauge weights that decide where weekly CRV emissions flow.

That third privilege turned Curve gauges into one of the most valuable real-estate markets in DeFi. Stablecoin protocols like Frax, MIM, mUSD, and LUSD depended on Curve liquidity to stay pegged. The more CRV emissions flowing to their pool, the higher the LP yield, the deeper the liquidity, the tighter the peg. Whoever controlled the most veCRV controlled the gauges, and whoever controlled the gauges controlled stablecoin destiny.

The Curve Wars officially began when Yearn Finance, Stake DAO, and Convex started competing to accumulate veCRV. Yearn built yvBOOST and yveCRV vaults. Stake DAO offered sdCRV. But Convex won the war within a year. The protocol's design was simple, transparent, and offered better rewards. By the end of 2021 Convex controlled the majority of veCRV, and a secondary war was already starting: the battle for vote-locked CVX, the only way to influence Convex's own voting power.

How Convex Finance Works

The mechanism behind Convex is elegant. There are two separate user flows, and they interact through a shared veCRV treasury that the protocol controls forever, since veCRV locks cannot be undone.

The first flow is for Curve LPs. A user deposits, say, the 3CRV LP token (DAI/USDC/USDT) into Convex. The protocol's contracts take that LP and stake it into the corresponding Curve gauge on behalf of the depositor. Because Convex holds an enormous veCRV balance, the gauge applies the full 2.5x boost to the deposit. CRV emissions flow back to Convex, the protocol takes a 17% performance fee (10% to cvxCRV stakers, 5% to vlCVX holders, 1% to the treasury, 1% to harvest callers), and the remaining 83% is paid out to the LP depositor along with bonus CVX tokens minted at the source.

The second flow is for CRV holders who want yield without managing LP positions. They deposit CRV into Convex and receive cvxCRV, a tokenized representation of CRV that has been locked permanently in Convex's veCRV vault. cvxCRV stakers earn the 3CRV admin fees from Curve, plus 10% of all CRV harvested from LP positions, plus extra CVX. The tradeoff is that cvxCRV is not directly redeemable for CRV. Convex never unlocks its veCRV, so cvxCRV trades against CRV on a Curve pool, usually at a slight discount.

cvxCRV vs sdCRV vs Locking CRV Directly

If you hold CRV, you have three options. Lock it yourself for up to four years to get veCRV. Wrap it as cvxCRV through Convex. Or wrap it as sdCRV through Stake DAO. Each path has different tradeoffs that matter a lot for long-term yield.

The trick with cvxCRV is that you are giving up the optionality of unlocking your CRV in exchange for permanent liquidity and stacked rewards. For most retail users this is a fair trade because four-year lock decay is brutal. veCRV with one year of lock remaining grants only one quarter of its initial voting power. By contrast cvxCRV always sits on top of permanently locked CRV, so its rewards never decay.

The CVX Token and vlCVX

CVX is Convex's native governance token. It has a hard maximum supply of 100 million tokens, which is one of the most respected supply caps in DeFi. Tokens are minted as a function of CRV earned by the protocol: for each CRV that Convex receives, a proportional CVX is minted and distributed to depositors. The minting rate decreases over time on a logarithmic curve, so by May 2026 more than 99 million CVX has already been minted and the remaining supply is trickling out slowly.

Holding CVX in your wallet earns nothing on its own. To extract real value from the token, you have to lock it. The mechanism is called vlCVX, vote-locked CVX, and it works on a 16-week lock cycle. Once you lock CVX you receive vlCVX, which gives you three things: voting power inside Convex on which Curve gauges to support, eligibility to receive bribes from protocols that want your votes, and a share of platform fees.

Vote every two weeks on which Curve gauges Convex's veCRV treasury should boost. Each vote influences hundreds of millions in liquidity.

Protocols pay vlCVX holders directly through Votium, Llama Airforce, and Hidden Hand for their votes each round.

Receive 5% of all CRV harvested by Convex and a portion of cvxFXS revenue, paid as cvxCRV.

The 16-week lock is the critical detail. Once you lock CVX, it is non-transferable and unwithdrawable for the next 16 weeks. After the period ends the position can be relocked for another 16 weeks, or withdrawn and converted back into liquid CVX. Most serious vlCVX holders configure their position to auto-relock so they never miss a bribe round. Voting happens every two weeks (one Convex epoch), and each round distributes between $1 million and $5 million in bribes across active gauges.

The Bribe Economy: Votium, Llama Airforce, Hidden Hand

The bribe economy is the most interesting and most misunderstood part of Convex. The short story: protocols that need Curve liquidity pay vlCVX holders to vote for their gauge instead of someone else's. This started as a grey-area incentive in late 2021 and has since become a formalized marketplace handled by dedicated platforms.

Votium was the first dedicated Convex bribe platform. Built by an anonymous team in November 2021, it became the standard layer for buying and selling vlCVX votes. Protocols deposit incentives in advance of each voting round (every two weeks), vlCVX holders vote on Snapshot, and after the round closes Votium distributes the incentives proportionally to all voters who supported the relevant gauges. As of May 2026, Votium has processed more than $1.4 billion in cumulative bribes, with each individual round currently averaging between $2 million and $4 million.

Hidden Hand by Redacted Cartel competes with Votium, offering a multi-protocol bribe marketplace covering Convex, Aura (Balancer's equivalent), and a few smaller systems. Hidden Hand pioneered the bribe-vote-claim user experience with a single dashboard and inspired Votium to redesign its own interface in 2024. Llama Airforce is more of a research and dashboard project: it publishes vote-by-vote analytics, optimal bribe-to-vote ratios, and a tracker of historical vlCVX APR. Most active vlCVX holders use Llama Airforce to plan their votes and then claim rewards through both Votium and Hidden Hand.

vlCVX Voter ROI 2026: What the Returns Actually Look Like

The honest answer is that vlCVX yield has compressed significantly from its 2021-2022 peak. In late 2021, when CVX traded above $40 and CRV emissions still favored a small handful of stablecoins, voter APR routinely exceeded 40%. By May 2026, after years of competing inflation-style emission cuts and a more crowded gauge landscape, the average voter is earning between 17% and 24% in stablecoin-equivalent bribes, paid mostly in CRV, FXS, mkUSD, and various LST governance tokens.

The figures above assume you compound bribes back into CVX or claim them as stablecoins through Votium's auto-swap feature. Higher returns are possible if you correctly time CRV-denominated bribes during periods of CRV weakness, or if you negotiate direct bribes (sometimes called over-the-counter or OTC bribes) with a single protocol for a fixed CVX commitment. In contrast, blindly voting on the highest dollar bribe without optimizing for token volatility often delivers below-average returns.

Convex on Curve V2: Tricrypto and crvUSD Pools

Curve started as a stablecoin venue, but Curve V2 expanded the protocol to volatile assets through a different invariant called CryptoSwap. By 2023 Curve V2 pools like tricryptoUSDC (USDC/wBTC/ETH) and tricryptoUSDT were absorbing serious volume from other AMMs, especially for large traders looking to sell large ETH amounts efficiently. Convex integrated all these pools and continues to offer them with the same boosted rewards stack as stable pools.

The launch of crvUSD in 2023 added another layer to Convex. crvUSD is Curve's native stablecoin, minted against ETH, wBTC, sfrxETH, wstETH, and tBTC collateral through an algorithm called LLAMMA. Curve incentivizes crvUSD pools with CRV emissions, and Convex offers boosted access to all of them. The most prominent crvUSD pools on Convex in May 2026 are crvUSD/USDC, crvUSD/USDT, crvUSD/FRAX, and the tBTC/crvUSD pool, with combined Convex TVL hovering around $280 million. These pools usually produce yields between 4.5% and 8.5% on a stablecoin basis, which makes them attractive against alternatives like tokenized treasuries from Ondo Finance.

Convex Frax: The cvxFXS Integration

One of Convex's smartest strategic moves was integrating directly with Frax Finance in 2022. Frax launched its own vote-escrow system called veFXS, modeled on Curve's veCRV. To save Frax users from the same lock-up dilemma that drove the Curve Wars, Convex offered cvxFXS: a wrapped version of permanently locked FXS that earns boosted FXS emissions, Frax Pool yield, and additional CVX rewards.

The cvxFXS system mirrors cvxCRV. FXS holders deposit FXS into Convex, receive cvxFXS in return, and Convex locks the FXS permanently into veFXS to maintain maximum boost on Frax LP positions held inside its platform. Stakers of cvxFXS receive a portion of Frax protocol revenue, FXS emissions, CRV (yes, CRV, because Convex's Frax integration captures CRV from Frax-related Curve pools), and CVX. As of May 2026 the cvxFXS pool has roughly $90 million in TVL with yields between 7% and 13% depending on FXS price and bribe season.

Convex also operates a Frax Pool program where LP positions on Fraxswap and Frax-related Curve pools get boosted FXS rewards through cvxFXS's veFXS treasury. This means Frax stablecoin LPs on Convex earn three layers: trading fees, CRV emissions, and boosted FXS emissions, often producing the highest stablecoin yields in DeFi during good market conditions.

Convex vs Stake DAO vs Yearn: Honest Comparison

Choosing between Convex, Stake DAO, and Yearn for Curve yield depends on what you optimize for: governance flexibility, raw APR, auto-compounding, or platform risk.

The pattern is clear. Convex is the choice when you want maximum yield and are willing to claim rewards manually every few weeks (or use a third-party auto-compounder). Yearn is the choice when you want a hands-off experience and do not mind paying a slightly higher performance fee. Stake DAO is competitive but has consistently smaller TVL, which means its boosts on smaller pools are sometimes less efficient than Convex's.

Top Convex Pools by TVL in 2026

Convex hosts around 120 active gauges, but most of the TVL is concentrated in 10-15 pools that have either earned consistent bribes, attracted major LST integrations, or anchored a stablecoin's peg. Here is a snapshot of the dominant pools as of May 2026.

Lido's largest external venue. Earns CRV, CVX, and LDO rewards. Yield 3.8-5.5%.

USDC/wBTC/ETH volatile pool. High trading fees, yield 6-12% with bribe rotation.

The foundational stablecoin pool. Lower yield (3-4.5%) but battle-tested reliability.

Anchor pool for Curve's native stablecoin. Yield 5-7%, supported by ongoing emissions.

Frax LST anchor. Stack of CRV + CVX + FXS makes this often the highest LST pool.

Threshold's decentralized Bitcoin paired with crvUSD. Yield 8-14% in active periods.

Beyond the top six, Convex hosts many smaller pools covering pairs like rETH/wstETH, mkUSD/crvUSD, USDe/USDC, EURe/USDC, and various Pendle-related LST positions. Smaller pools sometimes deliver outsized yield because bribes per dollar of TVL are higher, but the tradeoff is thinner liquidity and faster yield decay if the pool grows quickly.

Step-by-Step: How to Use Convex Finance

Now that you understand the mechanics, here is the actual user flow. You will need an Ethereum wallet (MetaMask, Rabby, or a hardware wallet through a software interface), some ETH for gas, and either CRV, FXS, or Curve LP tokens. Before signing transactions, double-check the contracts following the same hygiene rules you would use for general wallet security, and consider using a fresh address for new strategies similar to a burner wallet for airdrops.

Step 1: Deposit LP Tokens for Boosted Yield

Start by acquiring a Curve LP token. The easiest way is to go to curve.fi, pick a pool (3Pool, stETH/ETH, or crvUSD/USDC are great starting points for stablecoin yield), and deposit one or several of the underlying assets. Curve will mint you the corresponding LP token. Do not stake it on Curve directly. Instead, head to convexfinance.com, connect your wallet, and look for the same pool in the Convex dashboard.

Click Deposit. The Convex interface will ask you to approve the LP token (one-time transaction) and then deposit it. After confirming the second transaction, your LP is staked in the Curve gauge through Convex's smart contracts, you start earning the boosted CRV plus CVX rewards automatically, and a small amount of cvxLP appears in your wallet to represent your position.

Step 2: Claim Rewards

Convex does not auto-compound by default. Rewards accumulate as a claimable balance, and you choose when to harvest. Inside the dashboard, expand your active position, click Claim and Stake or Claim. The first option claims your CRV plus CVX and restakes the CRV portion into cvxCRV. The second simply claims everything to your wallet. Most users harvest every two to six weeks depending on gas conditions and position size, because claiming small amounts during high Ethereum gas prices can wipe out a chunk of the yield.

Step 3: Lock CVX as vlCVX

Once you have accumulated CVX from your LP positions or bought CVX on the open market, you can lock it. Go to the Lock CVX page on the Convex dashboard, enter the amount, approve, and confirm the lock. From that moment your tokens are vlCVX for 16 weeks. Enable the Auto-Relock option if you intend to stay locked long-term, otherwise you will need to manually relock at the end of each cycle.

Step 4: Vote on Gauge Weights

Voting happens on Snapshot. Every two weeks (one Convex voting round) Votium publishes the list of incentivized gauges with the bribe size per CVX vote. You can vote manually on the Snapshot proposal, or you can delegate your voting power to Llama Airforce, which votes optimally on your behalf. After the round closes (usually Thursday morning UTC), Votium prepares the bribes and you can claim them from votium.app.

CVX Tokenomics in Detail

Understanding CVX supply and distribution helps you evaluate the long-term value of locking. The maximum supply is fixed at 100 million CVX, hardcoded into the contract. Distribution at launch was: 50% to Curve LP rewards (minted as users earn CRV), 25% to liquidity mining incentives during the first months, 9.7% to the Convex treasury (vesting), 9.7% to investors (vesting), 1% to veCRV bootstrappers, 1% to the team (vesting), and the rest to grants and partnerships.

The CRV-to-CVX emission curve is the most important element. For every CRV harvested by Convex, a number of CVX is minted, but the rate decreases logarithmically. In the first months 1 CRV produced about 1 CVX. By 2026 the rate is below 0.05 CVX per CRV, and once the 100 million hard cap is reached, no new CVX will ever be minted regardless of how much CRV the protocol harvests. This means Convex's revenue (the 17% performance fee) is no longer being diluted by ongoing CVX issuance, which is a key bullish argument for vlCVX holders in 2026 and beyond.

Risks of Using Convex Finance

Convex is one of the most battle-tested protocols in DeFi but it is not risk-free. Honest risk awareness is essential before allocating capital.

Convex sits on top of Curve, so you inherit both protocols' attack surface. Curve was exploited for $73M in July 2023 (Vyper bug). Convex was unaffected but TVL dropped 35% briefly.

CVX value is fundamentally tied to the value of CRV emissions. If CRV crashes, the value of vlCVX votes crashes too. Bribers stop bidding aggressively, and yield compresses.

vlCVX is illiquid for 16 weeks. If the CVX market price crashes during your lock you cannot exit. cvxCRV is also non-redeemable for CRV directly, so you depend on the cvxCRV/CRV pool peg.

Convex's anonymous team retains administrative privileges over some upgrades. Governance is functional but not fully decentralized. Treasury actions still depend on the multisig.

Curve LP token prices are read from internal Curve oracles. Manipulating those prices is hard but not impossible during periods of extreme volatility. Use trusted oracles for monitoring.

Many Convex pools contain USDT, USDC, FRAX, crvUSD, mkUSD, or USDe. Any of those can depeg under stress. A 5% depeg can produce real loss for LPs.

Other risks worth noting include impermanent loss on Curve V2 volatile pools (StableSwap pools have negligible IL but tricryptoUSDC and similar pools do not), regulatory uncertainty around veToken structures in certain jurisdictions, and gas-fee risk on smaller positions where claiming rewards can become economically inefficient.

Pros and Cons of Convex Finance

- Maximum 2.5x veCRV boost without locking CRV personally

- Five years of operation without a single major exploit

- Bonus CVX rewards on top of standard CRV emissions

- vlCVX bribe yield consistently 17-24% in 2026

- cvxCRV provides liquidity that pure veCRV lacks

- Frax integration adds an additional emission layer

- cvxCRV is not redeemable for CRV directly

- vlCVX is illiquid for 16 weeks once locked

- 17% performance fee on CRV harvests

- Manual claiming, no native auto-compounding

- Anonymous team, limited transparency on treasury

- Yield correlates with overall CRV emission schedule

Best Practices for Convex Users

Years of community experience have produced a clear playbook. First, never deposit into the wrong pool. Convex pool names match the Curve pool, but typo'd tickers or impersonator contracts have caused losses before. Always navigate to Convex through the official URL convexfinance.com and verify the pool's underlying assets on Curve before deposit.

Second, optimize claim frequency around gas. For small positions (under $5,000), claim every six to eight weeks. For mid-sized positions ($5,000-$50,000), every three to four weeks. For large positions ($50,000+), claim weekly or use a third-party auto-compounder like Concentrator or Pirex. The gas math is the deciding factor.

Third, if you are using vlCVX for bribe income, calibrate your strategy to your time budget. If you have 15 minutes every two weeks, delegate to Llama Airforce. If you have an hour per epoch, vote manually for the highest dollar-per-CVX bribes. Either path is fine, but constantly switching strategies often produces worse results than committing to either approach for a full quarter.

Fourth, monitor the cvxCRV/CRV peg before significant deposits or withdrawals. The peg usually sits between 0.85 and 1.00 (cvxCRV trades slightly below CRV because of its non-redeemable nature). If you see cvxCRV trading below 0.85, that is often a buying opportunity for users who plan to stake long term. If above 1.00 (rare), consider claiming CRV-denominated rewards as CRV directly rather than wrapping into cvxCRV.

Fifth, use a transaction simulator on every major Convex interaction to catch silent approval scope issues. Tools that perform transaction simulation before signing will tell you exactly which tokens move and which approvals are granted. This is also a strong defence against address poisoning and clipboard-replacement attacks on the contract addresses you paste.

The Curve Wars in 2026: Where Convex Stands

Five years after launch, the Curve Wars are in a stable equilibrium. Convex still controls roughly 49% of veCRV. The next closest competitor (excluding Curve's own treasury locks) is Stake DAO at roughly 6%. There has not been a serious challenger to Convex's dominance since the failed Mochi attack in late 2021 and a brief moment in 2022 when Yearn briefly considered re-engaging through Cove. None of those threats materialized into meaningful veCRV accumulation.

What has changed is the structure of the bribe market. In 2021-2022 bribes were heavily skewed toward stablecoin protocols (FRAX, MIM, alUSD, mUSD) trying to defend their pegs. By 2026 the bribe market is dominated by three categories: liquid staking tokens (stETH, rETH, sfrxETH, ezETH) which still account for roughly 35% of all bribes, native stablecoin issuers (FRAX, crvUSD, mkUSD, USDe) at about 30%, and a long tail of newer assets including RWA-backed stablecoins at around 20%. The rest is shared among LRT protocols, BTC LSTs, and a handful of niche pools.

The other shift is on the Convex side itself. The protocol launched a sidechain expansion in 2023 covering Convex on Arbitrum, Optimism, Base, and Polygon for Curve pools that exist on those L2s. By May 2026 the L2 Convex deployments combined hold roughly $90 million in TVL, a small fraction of the mainnet $1.1 billion but growing as Curve V2 expands its multichain reach. Voting still happens only on Ethereum mainnet for vlCVX, however, because the veCRV treasury lives there.

Convex Compared to Pure DeFi Alternatives

It is worth situating Convex against the broader landscape of DeFi yield. Stablecoin LPs on Convex typically earn 4-8%, which is in the same ballpark as supplying USDC on Aave V3 or Compound V3 (3-6%), Pendle fixed yields on stablecoin LSTs (5-10%), or holding tokenized treasuries through RWA platforms like Ondo and Backed. The difference is that Convex carries both Curve and Convex smart contract risk on top of the stablecoin risk, while treasuries carry mostly counterparty risk.

Compared to Rocket Pool's rETH or Lido's stETH, depositing the LST into Convex on the corresponding LP pool typically adds an extra 1-3% on top of the base staking yield, in exchange for accepting LP smart contract risk and minor exposure to the ETH/LST peg. For users who already hold LSTs and want extra yield, depositing into Convex is one of the cleanest ways to compound.

Compared to using a DEX aggregator like 1inch for straight trading, Convex is a yield product, not a swap product. The use cases do not overlap, but they often complement each other: you might swap into a Curve LP base asset through 1inch, deposit the LP into Convex, and rotate periodically based on which pools have the most bribes.

Frequently Asked Questions

Q Is Convex Finance safe in 2026?

Convex has operated for five years without a major direct exploit. Its smart contracts have been audited by MixBytes and others, and the protocol survived the 2023 Curve Vyper incident without contagion. However, Convex inherits Curve smart contract risk, since LP tokens are ultimately deposited into Curve gauges. The protocol is among the safer veToken platforms but is not risk-free.

Q What is the difference between CVX and vlCVX?

CVX is the liquid governance token of Convex. vlCVX is CVX that has been locked for 16 weeks. Only vlCVX can vote on Convex governance and receive bribes through Votium and Hidden Hand. Plain CVX in your wallet does not earn anything by itself; it must be locked to capture protocol value.

Q Can I unlock vlCVX before 16 weeks?

No. Once you lock CVX as vlCVX, the position is non-transferable and non-withdrawable for the full 16-week period. After the lock expires you can withdraw to liquid CVX or auto-relock for another 16 weeks. This illiquidity is the main risk vector for vlCVX holders during volatile markets.

Q Why does cvxCRV sometimes trade below CRV?

cvxCRV is permanently locked CRV from Convex's perspective. Holders who want immediate CRV must sell cvxCRV on the Curve cvxCRV/CRV pool, where it usually trades at a small discount (typically 0.90-0.99) because the supply side is structurally larger than redemption demand. The discount is a natural feature, not a depeg.

Q How much vlCVX do I need to make bribe income worthwhile?

At current CVX prices (around $3-5 in May 2026) and Ethereum gas costs, around 100 CVX (about $400) is the practical floor for bribe income to make economic sense after claiming gas. Positions below this often have claim gas eating a meaningful percentage of monthly bribes. Many small holders simply use Llama Airforce's delegation rather than claiming themselves.

Q Are Convex rewards taxable?

In most jurisdictions, yes. CRV, CVX, FXS, and bribe payments received from Convex or Votium are typically treated as ordinary income at the time of claim, valued at the spot price. The subsequent sale of those tokens creates a capital gain or loss. Tax treatment varies by country, so consult a crypto-aware tax professional before assuming any specific framework applies to you.

Q What is the difference between Convex and Aura Finance?

Aura Finance is to Balancer what Convex is to Curve. Aura aggregates veBAL voting power and offers boosted Balancer LP rewards plus an AURA governance token. The mechanics mirror Convex closely. Some Convex contributors helped design Aura, so the architecture is intentionally similar. Both protocols also share Hidden Hand as a bribe platform.

Q Does Convex run on layer 2 networks?

Yes, Convex has deployed sidechain LP staking on Arbitrum, Optimism, Base, and Polygon. These deployments boost Curve pools that exist natively on those L2s and offer the same fee structure as mainnet. However, vlCVX voting and the main veCRV treasury remain on Ethereum mainnet, so the most lucrative bribe activity is still mainnet-exclusive.

Q Can Convex's veCRV ever be unlocked?

No. Convex permanently relocks all veCRV at maximum duration, and the protocol's smart contracts do not contain an unlock function for the treasury. This was a deliberate design choice that gave depositors confidence that the CRV they wrapped as cvxCRV would never be sold by Convex. It is also why cvxCRV cannot be directly redeemed.

Q What happens if CRV emissions stop?

Curve's emission schedule is fixed by smart contract until approximately year 2050. Annual emissions decrease by roughly 15% each year (Curve's "epoch" model). Even at compressed emission rates, gauge voting will remain valuable because Curve trading fees alone generate significant revenue. However, vlCVX yield would compress substantially if base emissions fell below a threshold that makes bribes uneconomical.

Conclusion: Why Convex Still Matters

Convex Finance occupies a strange and powerful position in DeFi. It is not the largest protocol by TVL, it is not the flashiest, and its anonymous founders rarely give interviews. Yet for five years it has quietly controlled the gauge weights of one of the most important liquidity venues in crypto, and through that control it has shaped the destinies of dozens of stablecoins, liquid staking tokens, and yield strategies. If you have ever used a stablecoin that depends on Curve liquidity, you have been indirectly affected by a vlCVX vote.

For users who deposit Curve LP tokens, Convex is still the highest-yield option in most cases, with a consistent boost of 1-3% over unboosted Curve, plus CVX bonuses. For users who hold CRV, cvxCRV is the best compromise between yield and liquidity. For users who want to participate in DeFi governance from a position of real economic power, locking CVX for vlCVX remains one of the most concentrated, lucrative voting positions in all of crypto. The protocol is mature, battle-tested, and has survived multiple market cycles without a major direct exploit.

The Curve Wars never really ended. They settled into an equilibrium, and Convex sits at the center of that equilibrium. Anyone serious about yield strategies on Ethereum should understand Convex at a deep level, even if they choose not to use it directly. The mechanisms it pioneered (vote-wrapping, bribe markets, permanent locks) have been copied by Aura, Equilibria, Penpie, and dozens of smaller protocols. Convex Finance is not just a yield product, it is the canonical template for how to harvest value from veToken systems, and that template will continue to shape DeFi for years to come.

Ready to put what you have learned into practice? Start by understanding the underlying mechanics of DeFi fundamentals, study the gas dynamics that determine when claiming makes sense, then consider whether a small position in vlCVX matches your risk tolerance. Whether you choose to deposit, lock, or simply observe, Convex Finance offers one of the clearest windows into how power, liquidity, and yield interact in modern DeFi.

Related Guides

- What Is Curve Finance? Stablecoin AMM, veCRV and CRV Token Explained (2026)

- How to Use Curve Finance: Stablecoin Swaps, Pools and Slippage Guide (2026)

- Bonding Curve Math in Crypto: Linear, Exponential and Sigmoid Models (2026)

- Curve vs Uniswap: DeFi DEX Models Compared (2026)

- Pendle Finance Explained: Yield Tokenization, PT, YT and Fixed-Rate DeFi (2026)

- What Is Aftermath Finance? Sui DeFi Perps CLOB Guide 2026