Tokenized Treasuries: Complete 2026 Guide to Onchain US T-Bills

— By Whatsertrade in Tutorials

Compare BUIDL, OUSG, USDM, USYC, and BENJI tokenized Treasuries by TVL, yield, minimums, regulatory model, and where to buy onchain in 2026.

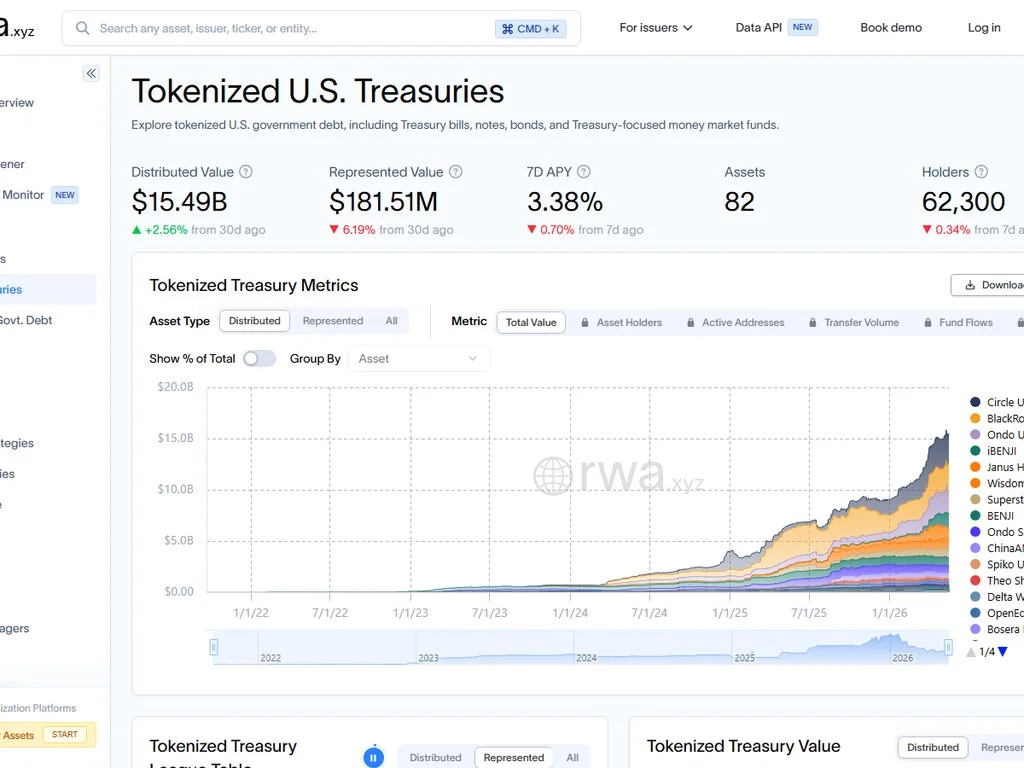

Tokenized treasuries are short-duration US Treasury bills wrapped into blockchain tokens that pay daily yield, settle in seconds, and trade 24/7. As of May 2026, more than $9.8 billion in onchain Treasury products are circulating across Ethereum, Solana, Stellar, Avalanche, Aptos, and Polygon, anchored by giants like BlackRock's BUIDL, Ondo's OUSG and USDY, Mountain Protocol's USDM, Hashnote's USYC, and Franklin Templeton's BENJI. This is the fastest growing segment of the real world asset (RWA) sector and the cleanest bridge between traditional fixed income and decentralized finance.

If you are sitting on idle stablecoins earning 0%, a tokenized Treasury fund pays you the same yield the US government pays primary dealers, currently around 4.2% to 4.8% APY net of fees, delivered as either a rebasing balance or an accruing share price. You hold a token in your wallet. The fund administrator holds the actual T-bills at BNY Mellon or State Street. The smart contract handles transfer logic, eligibility checks, and yield distribution. Settlement is atomic, transparent on a block explorer, and available outside of US banking hours.

This guide breaks down the five flagship tokenized Treasury products head to head, the regulatory wrappers behind them (Reg D 506(c), Reg S, BVI Professional Funds, qualified investor rules), exactly where and how to buy each one, the tax treatment in the US and EU, and the risks that the marketing decks tend to skip. By the end, you will know which product fits a corporate treasury, a DAO reserve, a high net worth individual, or a yield-hungry DeFi user.

What Are Tokenized Treasuries?

A tokenized Treasury is an ERC-20, SPL, or Stellar token that represents a beneficial interest in a regulated fund or special purpose vehicle that holds short duration US government debt. The underlying portfolio is typically 1-month to 6-month Treasury bills, sometimes mixed with overnight reverse repos and a small cash buffer for liquidity. The token is the digital wrapper. The yield comes from the bills.

The product sounds boring on purpose. That is the point. Tokenized Treasuries are not designed to ten-x. They are designed to give blockchain users access to the safest yield in dollar denominated fixed income, distributed natively through wallets, and composable with DeFi protocols. Corporates that previously parked cash in money market funds now park it in BENJI or BUIDL. DAOs that held bare USDC now allocate to USDY or USDM. Market makers use USYC as posting collateral on prime brokers like FalconX and Hidden Road.

The economics are simple. The fund earns the prevailing T-bill yield, deducts a management fee (usually 15 to 50 basis points), and passes the rest to token holders. Distribution mechanics differ by product. BUIDL and BENJI mint new tokens daily to represent accrued interest, so your balance grows. OUSG, USYC, and Mountain's USDM use a price accrual or rebasing approach. In every case, the token holder receives the Treasury yield without ever touching a brokerage account or filing a custody agreement.

How Tokenized Treasuries Work Under the Hood

Every tokenized Treasury product follows the same five-layer architecture. The asset layer is the actual portfolio of T-bills, held by a qualified custodian like BNY Mellon, State Street, or Anchorage Digital. The fund layer is a legal entity (Delaware statutory trust, BVI segregated portfolio, Luxembourg SICAV) that owns the assets and issues units. The transfer agent layer maintains the official register of token holders and processes subscriptions and redemptions, typically run by Securitize or Zeconomy. The token layer is the onchain ERC-20 with built-in allowlist logic that blocks transfers to non-whitelisted wallets. The distribution layer covers exchanges, brokers, DeFi integrations, and direct subscription portals.

The allowlist is the part that confuses crypto-native users coming from permissionless stablecoins. Every tokenized Treasury enforces transfer restrictions at the smart contract level. You cannot send BUIDL to an arbitrary Ethereum address. The receiving address must have completed KYC, signed the subscription agreement, and been added to the transfer agent's whitelist. This is a regulatory requirement, not a technical limitation. Without the allowlist, the issuer would be running an unregistered securities exchange.

Some products work around this with a parallel permissionless wrapper. Ondo's USDY, for example, can be held by non-US persons without an allowlist on its issuer-defined retail tier. Mountain's USDM is fully permissionless but excludes US persons through geofencing and IP blocks at the issuance gateway. The product team chooses the regulatory model, and the smart contract enforces it.

BUIDL vs OUSG vs USDM vs USYC vs BENJI: Full Comparison

These five products together hold more than 80% of the tokenized Treasury market by total value locked. Each was built for a different audience and a different distribution model. Here is the side by side breakdown as of May 2026.

A few patterns jump out of this table. BUIDL is the institutional whale. BlackRock built it for funds, market makers, and prime brokers who needed a single tokenized cash management product they could trust. The $5 million minimum makes it inaccessible to anyone outside of a corporate treasury or a large DAO. BENJI is the retail product. Franklin Templeton's FOBXX has been a registered '40 Act money market fund since 2021, which is why the SEC was comfortable letting them tokenize it on Stellar and later Ethereum. Retail US investors can buy BENJI directly through the Benji Investments app.

OUSG and USYC sit in the middle. Both target accredited investors and qualified institutions with $100,000 entry tickets. USDY is Ondo's offshore retail wrapper, sold under Reg S to non-US persons through DEX integrations like Jupiter on Solana. USDM is the most DeFi-native option, fully permissionless, but explicitly geo-blocks US persons at the gateway and operates under BVI Professional Fund rules.

BUIDL: The Institutional Anchor

BlackRock launched BUIDL in March 2024 in partnership with Securitize as the transfer agent. Within 18 months it crossed $2 billion in TVL, and as of May 2026 it sits at roughly $2.9 billion. It is the largest single tokenized Treasury product on the market and the de facto institutional reference point. The fund is structured as a Delaware-domiciled BlackRock USD Institutional Digital Liquidity Fund Ltd, and it invests in cash, US Treasury bills, and repurchase agreements.

The token is an ERC-20 deployed across Ethereum, Arbitrum, Optimism, Polygon, Avalanche, and Aptos. Distribution is daily and automatic. New BUIDL tokens are minted to your wallet every business day to represent accrued interest, so 1 BUIDL is always worth $1 of NAV and your balance grows over time. Redemptions back to USDC can be processed by Circle through a partnership that gives BUIDL holders a 24/7 instant redemption window using Circle's settlement infrastructure.

The friction is real. You need to be a qualified purchaser under US securities law (typically $5 million in investments) or an institutional accredited investor outside the US. You go through Securitize's full KYC and AML check, sign the subscription documents, and wire fiat or send USDC to the fund's custodian. Once your wallet is on the allowlist, you can hold and transfer BUIDL to other whitelisted wallets. The redemption process is operationally smooth but legally restrictive. This is not a product for a retail DeFi user.

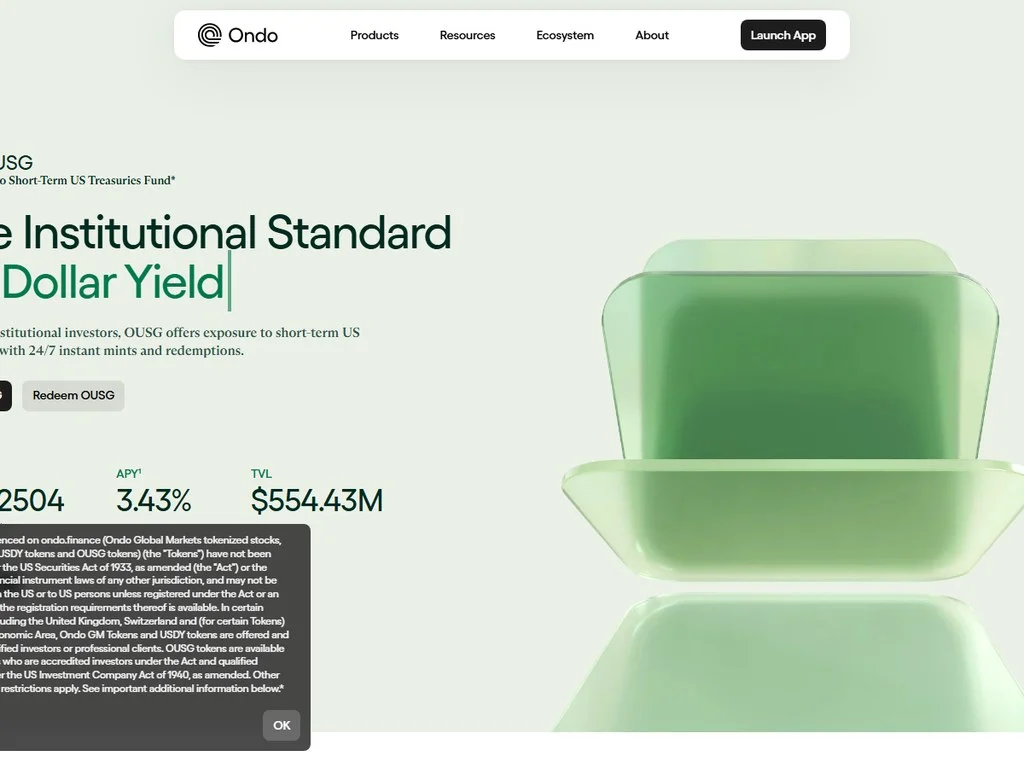

OUSG and USDY: The Ondo Stack

Ondo Finance operates two parallel products that together cover both institutional and retail demand. OUSG (Ondo Short-Term US Government Bond Fund) is the original institutional product, launched in early 2023. It originally held shares of BlackRock's iShares Short Treasury Bond ETF (SHV), but in 2024 Ondo migrated OUSG into BUIDL itself. So when you buy OUSG today, you are essentially buying a smaller-minimum wrapper around BUIDL, with Ondo charging a thin management fee on top.

USDY (Ondo US Dollar Yield) is Ondo's permissionless yield-bearing stablecoin alternative for non-US persons. Structured under Regulation S of the Securities Act, USDY is restricted from US persons but freely transferable among non-US holders after a 40 to 50 day distribution compliance period. After the seasoning period, USDY can be moved into Uniswap pools, lent on lending markets, used as collateral, or deposited in RWA-focused DeFi protocols.

USDY is the most DeFi-integrated tokenized Treasury after USDM. On Solana, it has deep Jupiter Aggregator support. On Sui and Mantle, it is integrated into lending markets. The token uses a share price accrual model, so 1 USDY starts at $1.00 and grows over time. You receive a fixed token amount on subscription and that token value rises with the yield curve.

USDM: Permissionless Tokenized Treasury

Mountain Protocol's USDM took a different regulatory path. Mountain incorporated in the British Virgin Islands and registered USDM under the BVI Professional Funds regime, which is designed for sophisticated and accredited investors but does not require strict ongoing KYC for token transfers. The result is a fully permissionless ERC-20 that rebases daily to deliver Treasury yield directly into the token balance. There is no allowlist on the smart contract. You can hold USDM in MetaMask, a hardware wallet, a Safe multisig, or any standard wallet.

The catch is jurisdictional. USDM is geo-blocked at the issuance and redemption gateway for US persons, UK retail, and several other restricted jurisdictions. Mountain enforces this through IP detection and KYC on the mint/redeem flow, not on the token itself. So a non-US holder can mint USDM, send it to anyone, and that recipient can hold or use it in DeFi. The recipient just cannot redeem to USDC directly through Mountain if they are in a restricted jurisdiction. Secondary market redemption through DEX pools or OTC desks is possible.

USDM is used extensively in DeFi. It has been integrated into Aave's Permissioned Markets, Maker's RWA collateral list, Pendle for yield trading, and Curve for stablecoin liquidity. The rebasing mechanism makes it composable with money markets that accept rebasing tokens, and Mountain publishes daily attestations from a Big Four-tier auditor confirming the underlying T-bill backing.

USYC: The Hashnote and Circle Story

USYC was originally a Cumberland Labs product called Hashnote Short Duration Yield Coin, structured as a regulated fund under the Cayman Islands Monetary Authority (CIMA). In early 2025, Circle acquired Hashnote outright, folding USYC into the Circle ecosystem alongside USDC, EURC, and the broader Circle Payments Network. As of May 2026, USYC sits at roughly $420 million in TVL and is the preferred collateral for crypto prime brokers.

The USYC differentiator is collateral utility. FalconX, Hidden Road, Cumberland, and BitGo Prime all accept USYC as posting collateral for derivatives trading. This means a fund can post USYC to a prime broker, continue earning the underlying Treasury yield, and use that collateral to trade perpetuals or options. Compare that to posting USDC, where the yield is zero (or captured by the broker as float). USYC effectively gives institutional traders an extra 400 basis points of carry on their margin.

Subscription requires accredited investor status, a $100K minimum, and a full KYC process through Hashnote's portal. Settlement is on Ethereum mainnet primarily, with Canton Network integration for institutional rails. The acquisition by Circle means USYC will likely become deeply integrated with USDC over the next 18 months, with proposals on the table to allow USYC-to-USDC instant conversion at NAV through Circle Mint.

BENJI: The Retail On-Ramp

Franklin Templeton's BENJI represents shares of the Franklin OnChain US Government Money Fund (ticker FOBXX), which has been a registered '40 Act money market fund since 2021. Franklin was the first major asset manager to use blockchain as the official record of fund ownership, with the Stellar network serving as the system of record. Each BENJI token represents one share in the fund, valued at $1.00 with daily yield distributed via new token issuance.

BENJI is the retail-friendliest tokenized Treasury. There is no minimum investment. US retail investors can open an account in the Benji Investments app, link a bank account via ACH, and buy BENJI in dollar amounts. The fund is registered with the SEC, so the disclosure obligations are the same as any other money market fund. As of 2025, Franklin expanded BENJI from Stellar to Ethereum, Polygon, Arbitrum, Base, Avalanche, Solana, and Aptos, with cross-chain transfers managed through the BENJI smart contract suite.

For a retail user in the US who wants tokenized Treasury yield without the qualified purchaser hurdles of BUIDL or the offshore restrictions of USDY, BENJI is the answer. The trade-off is that BENJI is not yet as deeply integrated into DeFi protocols as USDM or USDY, since the regulatory framework around a '40 Act fund traded onchain is still being clarified. But for self-custody yield without leaving US compliance, BENJI is the clearest path.

Regulatory Models Explained

The legal structure behind each tokenized Treasury determines who can buy it, how it can move, and what happens if something goes wrong. Three regimes dominate the market: Reg D 506(c), Reg S, and offshore professional fund regimes like BVI and Cayman.

For US accredited and qualified investors only. Allows general solicitation. Requires verification of accredited status. Used by BUIDL, OUSG, USYC.

For non-US persons only. 40 to 50 day distribution compliance period. Cannot solicit US investors. Used by USDY and offshore wrappers.

Offshore regulated fund for sophisticated investors. Lighter ongoing reporting. Used by USDM (BVI) and USYC (CIMA).

Full SEC-registered open-end fund. Daily NAV, prospectus, public disclosures. Used by BENJI (FOBXX). Retail accessible.

Under Regulation D 506(c) of the Securities Act of 1933, an issuer can sell unregistered securities to verified accredited investors. The accredited threshold for individuals is currently $200,000 in annual income, $300,000 with a spouse, or $1 million in net worth excluding primary residence. Qualified purchasers, a higher bar used by BUIDL, requires $5 million in investments. Reg D issuers must verify accredited status through bank statements, brokerage statements, or a third-party verification letter, not just self-certification.

Regulation S allows offerings outside the United States to non-US persons, with no SEC registration. After a distribution compliance period (40 days for debt-like securities, longer for equity-like), Reg S securities can be freely transferred among non-US persons. This is why USDY can sit in any wallet and trade on DEXs, as long as the buyer can certify non-US status. The token contract enforces no transfer restrictions, but the legal wrapper restricts who can subscribe.

Offshore regimes like the BVI Professional Funds Act or the Cayman Islands Mutual Funds Law provide a middle path. The fund is regulated by a financial services authority but the disclosure obligations are calibrated for sophisticated investors. The product can be sold globally except where local rules prohibit it. The issuer maintains compliance through gateway-level controls rather than smart contract allowlists, which is how USDM achieves a permissionless token model.

Where to Buy Tokenized Treasuries

The distribution channels vary widely by product. Here is the practical buying guide for each of the five flagship tokens.

To buy BUIDL or OUSG, you sign up on Securitize or Ondo, complete accredited investor verification, sign the subscription agreement, and wire either fiat USD or send USDC to the fund custodian. Securitize processes BUIDL subscriptions in T+0 most days. Ondo processes OUSG subscriptions in T+0 within Ondo Markets hours and T+1 outside of them. Both products allow same-day redemption for an additional fee.

For USDY, the buying process is similar to OUSG but the eligibility check is non-US person status rather than accredited status. Non-US individuals can buy USDY through the Ondo app with a passport scan and proof of address. After the 40-day distribution compliance period, USDY can be traded freely on DEXs. Most onchain USDY liquidity sits on Jupiter on Solana, with deep DEX vs CEX arbitrage opportunities to bring USDY to NAV.

USDM is the most flexible. Non-US sophisticated investors mint through the Mountain Protocol gateway with KYC, but once minted, USDM transfers permissionlessly. You can swap any stablecoin for USDM on Uniswap V3 Ethereum pools, on Aerodrome on Base, or on Curve. The DEX route bypasses the gateway entirely. You simply buy USDM on the open market like any token. Yield accrues to your balance daily through the rebasing mechanism. The only restriction is that minting fresh USDM at NAV from Mountain requires going through the gateway KYC flow.

BENJI is bought through the Franklin Templeton Benji Investments app for US retail. Non-US institutional investors can access BENJI through Franklin's institutional onboarding, with minimums starting at $100K for institutional share classes. Direct DEX access for BENJI is still limited as of May 2026 because the SEC has been cautious about secondary market trading of a '40 Act fund's shares outside of the issuer's authorized channels.

Tax Treatment of Tokenized Treasuries

Tax treatment depends entirely on the legal structure of the underlying fund, not on the fact that ownership is represented onchain. Holding BUIDL is, for tax purposes, identical to holding a share of the BlackRock USD Institutional Digital Liquidity Fund. Holding BENJI is identical to holding a share of the Franklin OnChain US Government Money Fund. The blockchain wrapper does not change anything for the IRS.

For US holders, the typical treatment is as follows. Interest accrued on the underlying Treasuries is reported as ordinary interest income on Form 1099-INT, exempt from state and local income tax (because they are US government obligations). Capital gains on sale or redemption of the tokens are reported on Form 1099-B. For products that use daily token minting (BUIDL, BENJI), the new tokens are interest income with a $1 cost basis. For products that use share price accrual (OUSG, USYC), the gain on redemption is interest income if structured as a money market fund, or capital gain if structured as a bond fund.

For EU holders, tokenized Treasury yield is generally treated as foreign interest income, with tax credits available for any US withholding tax (typically zero on Treasury interest for tax treaty residents). Local capital gains rules apply to sale or redemption. Crypto-to-crypto swaps involving tokenized Treasuries (for example, swapping USDC for USDM on Uniswap) are taxable events in most EU jurisdictions, just like any other token swap. Always consult a tax professional familiar with both crypto taxation and securities holdings.

DeFi Integrations and Composability

The defining feature of tokenized Treasuries versus traditional money market funds is composability. A T-bill in a brokerage account does nothing for you beyond paying interest. A tokenized Treasury can be used as collateral, lent into a market, deposited in a yield strategy, or wrapped into a synthetic asset. This composability is currently strongest with USDM and USDY because of their permissionless transfer model.

The flagship DeFi integration is MakerDAO's RWA collateral portfolio. Maker (now operating as Sky) has allocated billions of DAI's backing to tokenized Treasury vaults run through Monetalis, BlockTower, and Centrifuge. The Maker reserves have been one of the largest single buyers of BUIDL and similar products, using them to back DAI and USDS issuance while capturing Treasury yield for the protocol surplus buffer. This has been so successful that DAI's reserve composition is now majority tokenized Treasury exposure rather than crypto collateral.

Aave has launched permissioned markets where institutional users can post BUIDL or USYC as collateral and borrow USDC or other stablecoins against it. The collateral factor is generous (often 90% or higher) because the underlying T-bills are essentially the safest dollar asset that exists. This unlocks yield-bearing collateral that earns ~4.4% from the Treasury plus any rebates from the lending protocol.

Pendle has built deep markets for tokenizing the yield on USDM and USDY. You can buy the principal token (PT) at a discount to face value and lock in a fixed yield, or buy the yield token (YT) to speculate on Treasury yield curves. This effectively brings interest rate trading onchain, with retail users able to take views on Fed rate cuts using a few clicks of a DEX swap.

Other notable integrations include Morpho lending markets accepting tokenized Treasuries as collateral, Curve Finance hosting deep USDM and USDY stablecoin pools that allow zero-slippage swaps, and various structured product platforms like Ethena and Resolv using tokenized Treasury yield as a base layer for delta-neutral strategies. The composability story is still developing rapidly.

Risks You Need to Understand

Tokenized Treasuries are the lowest risk product in the RWA category, but they are not riskless. Here are the seven specific risks every buyer should price in before allocating.

- Smart contract risk: The token contract could have a bug. Even audited contracts have failed. Look for products audited by Trail of Bits, Halborn, Code4rena, or similar Tier 1 firms.

- Custodian risk: The bank holding the underlying T-bills could fail. BNY Mellon, State Street, and Anchorage Digital are well capitalized, but no custodian is infallible.

- Issuer risk: The fund manager could fail operationally. Mountain, Ondo, and Hashnote are smaller entities than BlackRock or Franklin.

- Liquidity mismatch: Tokens trade 24/7, but the underlying T-bills do not. Large redemptions outside of US Treasury market hours might face gating or delay.

- Regulatory risk: The SEC, MAS, or local regulators could rule that a product violates securities or money market fund rules. Settlements have happened (Linqto, INX).

- Bridge and chain risk: Cross-chain tokenized Treasuries depend on the security of the bridges they use. A bridge exploit could disconnect the wrapped token from its native chain backing.

- De-pegging risk: Most tokenized Treasuries claim a $1 NAV peg. In a stressed market, secondary market price can deviate significantly from NAV, especially for permissionless products.

Smart contract risk is the most underdiscussed. Most tokenized Treasury contracts are upgradeable proxies, meaning the issuer can change the contract logic. This is necessary for compliance (sanctions blocking, allowlist updates) but it also means the contract behavior can change. A user trusting BUIDL or OUSG is trusting that Securitize and Ondo will not abuse upgrade powers. The contracts publish multi-signature governance configurations and time delays, but the trust assumption is real.

Liquidity mismatch is the most material risk for active users. T-bills settle on US bank business days. The blockchain settles 24/7. If everyone tries to redeem on a Sunday morning, the issuer cannot actually sell the underlying T-bills until Monday at 9am ET. Most products have a USDC liquidity buffer to handle weekend redemptions, but in a tail event, gates can be imposed. Read the offering documents on the specific redemption SLA before allocating size.

Tokenized Treasuries vs Yield-Bearing Stablecoins

The line between a tokenized Treasury and a yield-bearing stablecoin like USDe (Ethena's synthetic dollar) or sDAI (the rebasing version of DAI from MakerDAO) is fuzzy and getting fuzzier. Here is the practical distinction. A tokenized Treasury is backed 1:1 by short-duration US government debt held in regulated custody. A yield-bearing stablecoin can be backed by anything, including crypto basis trades, lending markets, or even other tokenized Treasuries.

USDM, USDY, and BENJI all function as yield-bearing stablecoins in user wallets, in the sense that 1 token approximates $1 and they pay yield. The difference is that the yield source is fully transparent (T-bills) and the regulatory wrapper is well established (fund registration). A protocol like Ethena, by contrast, generates yield from perpetual futures funding rates plus staked ETH yield, which carries very different risk than Treasury yield. Both can be called yield-bearing stablecoins, but they are not the same product.

For corporate treasuries, DAOs, and institutional users, the tokenized Treasury route is almost always preferable to a synthetic yield-bearing stablecoin. The risk profile is closer to a traditional money market fund. For DeFi-native users chasing higher yields, the synthetic options can offer 8-12% APY versus 4-5% for tokenized Treasuries, but the risk increase is more than commensurate.

The Outlook: Where Tokenized Treasuries Go Next

The tokenized Treasury market grew from roughly $750 million in early 2024 to over $9.8 billion by May 2026, a 13x expansion in 28 months. Most of that growth came from institutional allocations rather than retail buying. The next leg of growth is being driven by three vectors: corporate treasury adoption, DeFi integration deepening, and emerging market dollar demand.

Corporate treasury adoption is happening fastest among crypto-native companies. Coinbase, Kraken, and most major exchanges hold portions of their corporate cash in tokenized Treasury products. Public crypto companies have started reporting tokenized Treasury holdings on their balance sheets. The next wave is traditional public companies, who are slowly evaluating whether tokenized products like BUIDL can replace some of their commercial paper allocations.

DeFi integration deepening is making tokenized Treasuries more useful in onchain workflows. As more lending protocols, derivatives platforms, and structured products accept tokenized Treasuries as collateral, the opportunity cost of holding bare USDC keeps rising. Why hold an asset paying 0% when an equally liquid asset pays 4.4% and is accepted everywhere?

Emerging market dollar demand is the largest opportunity. Across Latin America, Africa, and Southeast Asia, there is enormous demand for dollar-denominated yield instruments. Local banking systems often cannot provide them efficiently. Tokenized Treasuries delivered through wallets give a Argentine, Nigerian, or Vietnamese user direct access to US Treasury yield without needing a US brokerage account. This is the long tail demand that could push tokenized Treasuries past $50 billion by 2028.

Practical Allocation Framework

If you are deciding which tokenized Treasury product to use, the answer depends on three factors: your jurisdiction, your size, and your composability needs.

Best fit: BENJI. Direct retail access, '40 Act regulated, no minimums, US compliant.

Best fit: OUSG or BUIDL. Reg D access with onchain delivery. OUSG for $100K+, BUIDL for $5M+.

Best fit: USDY or USDM. Lower minimums, deep DeFi integration, jurisdiction-friendly.

Best fit: USDM for permissionless. BUIDL via Securitize if KYC acceptable.

Best fit: USYC. Native acceptance at FalconX, Hidden Road, Cumberland.

Best fit: BUIDL or BENJI. Highest trust, biggest issuer names, established structures.

Within each category, a diversified allocation across two or three products often makes sense. A DAO treasury might hold 60% USDM for permissionless flexibility, 30% BUIDL for institutional credibility, and 10% USDY for Solana DeFi exposure. A US accredited investor might hold OUSG for the bulk and BENJI for the share that needs SEC-registered tax treatment. The products are not mutually exclusive.

Step by Step: Buying Your First Tokenized Treasury

Here is a concrete walkthrough for the most accessible path: buying USDM as a non-US person directly through the Mountain Protocol gateway. The same general flow applies to USDY through Ondo and BENJI through Franklin's Benji Investments app.

Step 1: Set up a wallet. Use a non-custodial wallet you control like MetaMask or a hardware wallet. Make sure you have enough ETH for gas on the chain you plan to use. USDM is available on Ethereum, Arbitrum, Base, Optimism, and Polygon. Base typically has the lowest gas costs.

Step 2: Complete KYC at the gateway. Go to the Mountain Protocol app and complete the KYC flow with a passport scan and proof of address. Verification typically takes 1-3 business days. Confirm you are not in a restricted jurisdiction (US, UK, Canada, etc.). The gateway operates separately from the token itself.

Step 3: Subscribe with USDC. Once approved, you can mint USDM by sending USDC to the Mountain Protocol mint address. The mint happens at NAV with no spread. Minimum is typically $10K for primary mint, lower thresholds available on secondary markets.

Step 4: Hold or deploy. Your USDM accrues Treasury yield daily through rebasing. Your wallet balance grows automatically without any action required. You can hold it as-is for yield, deposit it in a Pendle pool to lock in fixed yield, or use it as collateral on Aave or Morpho.

Step 5: Redeem when needed. When you want to exit, you have two paths. Redeem at NAV through the Mountain Protocol gateway (1-2 business days, KYC required), or swap directly on Curve or Uniswap V3 USDM/USDC pools. The DEX route is instant but may incur a small spread depending on pool depth.

Frequently Asked Questions

What are tokenized treasuries in simple terms?

Tokenized treasuries are blockchain tokens that represent shares in a fund holding short-duration US Treasury bills. You hold the token in your wallet and it pays you the Treasury yield (currently around 4.2% to 4.8% APY) either by minting new tokens to your balance daily or by increasing the share price. Major products include BlackRock's BUIDL, Ondo's OUSG and USDY, Mountain's USDM, Hashnote's USYC, and Franklin Templeton's BENJI.

How big is the tokenized Treasury market in 2026?

As of May 2026, the total tokenized Treasury market sits at approximately $9.8 billion in TVL across Ethereum, Solana, Stellar, Avalanche, Aptos, Polygon, and other chains. BlackRock's BUIDL leads at around $2.9 billion, followed by BENJI at $780M, USDY at $720M, OUSG at $680M, USYC at $420M, and USDM at $240M. The market grew 13x from early 2024 to mid 2026.

Can US retail investors buy tokenized treasuries?

Yes, US retail investors can buy BENJI directly through Franklin Templeton's Benji Investments app with no minimum and standard retail KYC. Most other tokenized Treasury products (BUIDL, OUSG, USYC) require accredited investor status or qualified purchaser status. USDY and USDM are restricted from US persons because they operate under Reg S or BVI rules.

What is the difference between BUIDL and OUSG?

BUIDL is BlackRock's institutional product issued through Securitize, with a $5 million minimum and direct access to qualified purchasers. OUSG is Ondo Finance's wrapper that holds BUIDL underneath, offering a lower $100,000 minimum and access to a broader accredited investor base. Operationally, OUSG is essentially a smaller-ticket gateway into BUIDL, with Ondo charging a thin management fee.

Are tokenized treasuries safe?

Tokenized Treasuries are the lowest-risk product in the RWA category because the underlying asset is short-duration US government debt. However, they are not risk-free. The main risks are smart contract bugs, custodian failure, issuer operational failure, liquidity mismatch between 24/7 tokens and weekday T-bill settlement, regulatory changes, and bridge risk for cross-chain wrappers. Diversifying across two or three issuers reduces issuer-specific risk.

How are tokenized treasuries taxed?

Tax treatment follows the underlying fund structure, not the blockchain wrapper. For US holders, Treasury interest is generally taxable as ordinary income (Form 1099-INT) and exempt from state and local tax. Capital gains on redemption follow standard rules. For EU holders, the yield is foreign interest income. Always consult a tax professional familiar with crypto and securities holdings, especially for cross-border situations.

Can I use tokenized treasuries as DeFi collateral?

Yes, depending on the product. USDM and USDY are widely accepted as collateral on Aave's permissioned markets, Morpho, MakerDAO RWA vaults, and many other lending protocols. BUIDL and USYC are accepted on prime brokers like FalconX and Hidden Road, and on permissioned DeFi venues like Aave Permissioned Pools. The permissionless products (USDM especially) offer the broadest DeFi composability.

Related Guides

- What Is Tokenization? How Real World Assets Become Onchain Claims (2026)

- What is Centrifuge (CFG)? Real-World Assets on Chain

- What Are Real World Assets (RWA) in Crypto? Asset Types, Yield and Risks (2026)

- Top 5 Real World Asset (RWA) Tokens in 2026: Tokenized Finance Goes Mainstream

- RWA Tokenization: A Beginner’s Guide to Real-World Assets