What Is OTC Trading in Crypto: Complete Guide to Over-the-Counter Desks (2026)

— By Tony Rabbit in Tutorials

What is OTC trading in crypto? Complete guide: trade lifecycle, top desks (Cumberland, Wintermute, B2C2, Coinbase Prime), settlement models and when to use OTC vs exchange (2026).

If you tried to buy 200 BTC on a public exchange order book, the price would move against you before your order was even half filled. That is not a flaw in the exchange. That is just how thin order books behave when a single trade is larger than the visible liquidity. This is exactly why institutional traders, family offices, miners, and crypto-native funds almost never execute size on the open market. Instead, they pick up the phone (or open a chat) and talk to an OTC desk.

Over-the-counter trading is the silent layer that sits underneath crypto. Every day, billions of dollars in BTC, ETH, USDT, and altcoins change hands without ever appearing on a Coinbase or Binance chart. Whales sell into desks. ETF issuers buy from desks. Miners liquidate monthly production through desks. The price you see flickering on a public chart is shaped by these private trades, but the trades themselves stay invisible.

In this guide you will learn exactly what crypto OTC trading is, how a real OTC trade flows from quote request to settlement, why the spread is the true cost (not the commission), how principal desks differ from agency desks, which firms dominate the 2026 landscape, and where retail traders can access OTC-style execution through platforms like Coinbase Prime, Kraken OTC, and Binance VIP. By the end you will understand a part of the market that most retail content never explains properly.

What Is OTC Trading in Crypto?

OTC stands for over-the-counter. In traditional finance, OTC refers to any transaction that happens off-exchange, directly between two counterparties, instead of being routed through a central limit order book. Bond markets, foreign exchange, and private equity all trade OTC. Crypto inherited the same concept and the same naming convention. A crypto OTC trade is a privately negotiated transaction in digital assets between a buyer and a seller, with a desk usually acting as the intermediary or principal counterparty.

The defining feature of OTC is that the trade does not hit the public order book. There is no live bid or ask shown to the rest of the market. Two parties agree on a price for a specific size, sign off, and settle. The world only learns about the trade afterward, if at all. Most desks publish weekly volume reports but never disclose individual fills. This privacy is not a bug. It is the entire point of the product.

In crypto, OTC desks typically handle minimum ticket sizes of $100,000 to $250,000, with most flow concentrated in the $1M to $50M range. The largest trades, what insiders call block trades, can exceed $500M for a single counterparty. These are the kinds of orders that would shatter the price on centralized exchanges if executed at market. Instead, they get worked quietly between a handful of professional liquidity providers.

Why OTC Exists: The Slippage Problem on Public Order Books

To understand why OTC desks exist, you need to understand what happens when a large market order hits a thin order book. Public exchanges display a stack of resting limit orders at various price levels. When you submit a market buy, your order eats through those resting sell orders starting from the lowest price and working upward. The bigger your order, the deeper you eat into the book, and the worse your average fill price becomes. This effect is called slippage, and on large trades it is the single biggest hidden cost in crypto.

Let us put real numbers on this. Imagine a fund needs to buy $10M worth of BTC at a moment when BTC is trading around $100,000. On a major exchange, the top of the order book might have around $500,000 in sell orders within 10 basis points of the mid price. Once those are eaten, the next layer might be 20 bps higher, then 50 bps, then 100 bps. A $10M market buy realistically pushes the fill price up by 200 to 500 basis points depending on the venue and the time of day. That is $200,000 to $500,000 of slippage cost on a single trade, before fees.

OTC desks solve this by quoting a single firm price for the entire size. The desk takes on the risk of unwinding the position itself, either by selling from its own inventory or by hedging on futures markets. The buyer pays a small premium over mid (the bid/ask spread) and walks away with the full $10M filled at one clean price. No screen impact, no front-running, no order book footprint.

Slippage cost: $450,000

Plus exchange fee: $10,000

Plus visible market impact

Spread cost: $50,000

No exchange fees

Zero market impact

That gap is why every serious crypto institution has at least one OTC relationship. On a single trade the savings can dwarf an entire year of subscription fees, data costs, and prime brokerage charges combined. For an entity that trades $500M a month, OTC is not optional. It is the only economically viable way to operate.

Exchange Order Book vs OTC Desk

The two execution venues serve very different needs. Public order books are perfect for small, frequent, price-discovery trades. OTC desks are perfect for large, infrequent, size-sensitive trades. Understanding the trade-offs is essential before you decide where to execute.

Notice the trade-off pattern. Order books give you price discovery and instant settlement but punish size. OTC gives you size and privacy but requires a relationship, a KYC process, and a willingness to accept the spread as your cost. Neither is universally better. They serve different jobs.

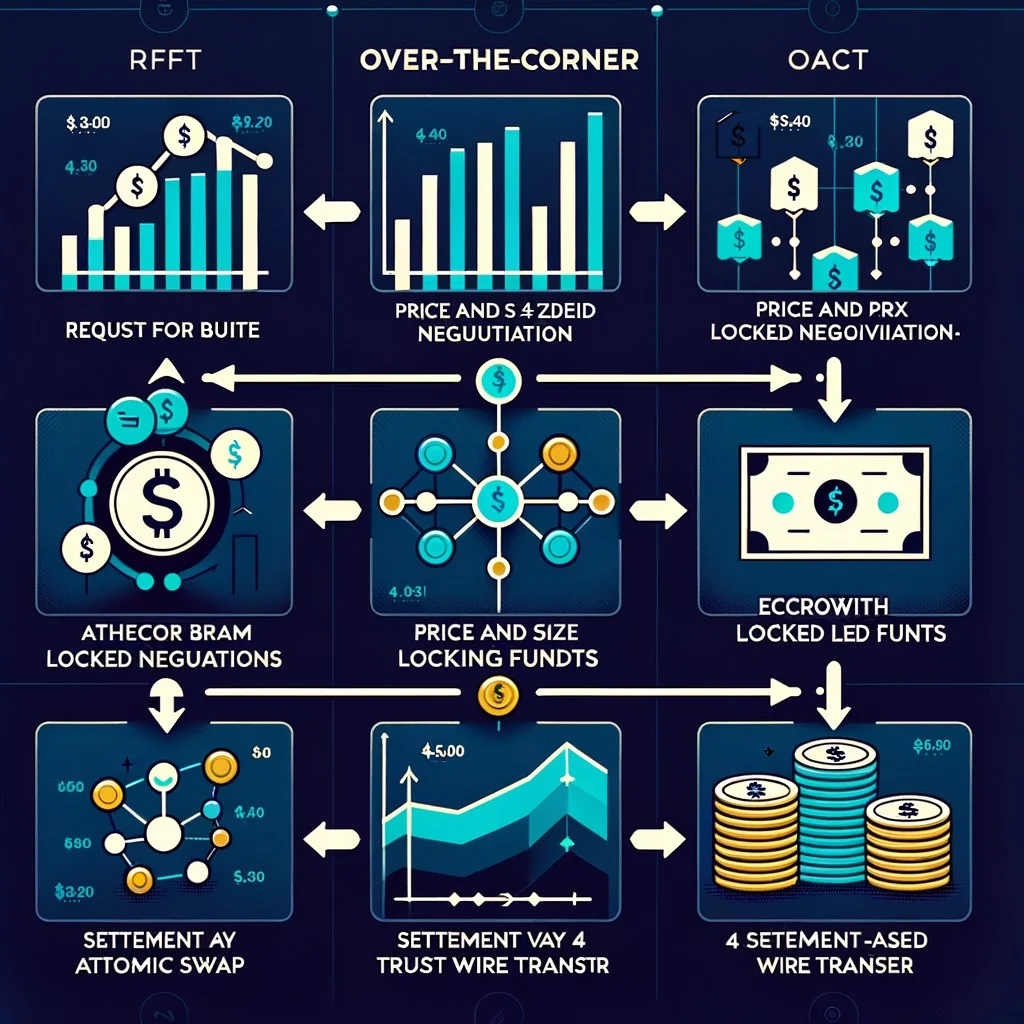

The 4-Step OTC Trade Lifecycle

Every OTC trade follows roughly the same flow, whether the counterparty is Cumberland, Wintermute, or Coinbase Prime. The terminology and tooling differ, but the four conceptual stages are universal. Understanding this lifecycle is the difference between sounding like a retail trader and sounding like someone who has actually executed institutional size.

Step 1: Request for Quote (RFQ)

Everything starts with an RFQ. The client sends a structured request to one or more desks specifying the asset, direction (buy or sell), and size. A typical RFQ looks like: "I am a taker, want to buy 150 BTC for USDT, settled today." The desk does not know the client's exact strategy but does know the trade ticker, which is enough to price it. Some desks accept RFQs via Telegram or Signal, others through proprietary chat tools, and the largest support FIX or REST APIs for automated workflows. Multi-desk RFQs are common: a fund pings five desks at once, holds the quotes side by side, and lifts the best one.

Step 2: Negotiation and Firm Quote

The desk responds within seconds with a firm two-way price or a one-way quote, depending on what was requested. A two-way quote shows both bid and ask, so the client can see the spread. A one-way quote is just the side relevant to the trade. The quote is firm for a defined window, usually 5 to 30 seconds, after which the desk reserves the right to refresh. The client either lifts the offer ("done"), counters, or walks away. There is no haggling on a $10M ticket the way some retail tutorials describe. The market moves too fast for round-trip negotiation, so the client either takes the price or walks.

Step 3: Escrow and Pre-Funding

This is where new traders trip up. The desk does not just trust the client to send funds. Before any settlement, both sides must demonstrate they have the assets. With a qualified custodian like BitGo, Fireblocks, Anchorage, or Komainu sitting in between, both sides pre-position funds. The buyer's USDT (or USD wire) sits at the custodian. The seller's BTC sits at the custodian. Once both legs are confirmed, the desk releases the trade for settlement. For repeat counterparties with credit lines, the escrow step can be relaxed or replaced by a settlement window, but the principle is identical.

Step 4: Settlement

Settlement happens via one of three models: atomic on-chain swap, custodian-mediated delivery versus payment (DVP), or trust-based wire and transfer. We will cover these in detail in the settlement section. For most BTC and ETH OTC trades in 2026, settlement is custodian-mediated and completes within minutes, marked as T+0. Wire-based fiat legs may extend to T+1 if the wire is sent outside US banking hours. Once both legs clear, both sides receive confirmation, the trade is done, and the desk updates its book.

Principal vs Agency OTC Desks

One of the most important and most confusing distinctions in the OTC world is whether the desk is acting as a principal or an agent. The label affects pricing, settlement risk, and who carries the inventory exposure. Many retail-oriented guides skip this entirely, but if you do not understand it you cannot evaluate desk quality.

A principal vs agency distinction works like this. A principal desk takes the other side of the trade with its own balance sheet. If you buy 100 BTC from Cumberland, Cumberland sells you 100 BTC out of its own inventory or short position. The desk now owns the opposite exposure and must manage that risk on its own books, typically by hedging on futures or sweeping liquidity from exchanges. The price you get is the desk's view of where it can unwind the position, plus a spread for its trouble.

An agency desk does not take inventory. It acts as a broker, matching the client to a counterparty (another desk, an exchange, or a different client) and earning a commission or markup for the service. Agency desks are common for esoteric altcoin trades, structured products, and situations where no single principal desk wants to warehouse the risk. Settlement still flows through the agency, but the actual price comes from the underlying counterparty.

The big crypto desks (Cumberland, Wintermute, B2C2, Galaxy) are primarily principal market makers. They quote tight spreads on liquid pairs because they can warehouse and hedge efficiently. Smaller boutique desks and many bank-affiliated OTC arms operate on an agency model, especially for illiquid tokens and one-off block trades. Always ask which model you are dealing with, because it changes everything about who bears the price risk between RFQ and settlement.

OTC Spread: The Hidden Cost

The single most common mistake new institutional traders make is to focus on commissions. OTC desks do not charge commissions, at least not in the traditional sense. They make money on the spread, the difference between the price they buy at and the price they sell at. This spread is built into every quote and is the single biggest cost of using OTC.

Typical spreads in 2026 look roughly like this. For BTC and ETH spot trades in the $100k to $5M range, expect 5 to 25 basis points over a reference mid price. For $5M to $50M, spreads tighten to 3 to 15 bps because the desk knows it can hedge cleanly. For tickets over $50M, top-tier desks compete down to 1 to 5 bps on majors during normal market conditions. Move into altcoins and spreads widen dramatically: 25 to 100 bps for top-20 alts, and 200 to 1000+ bps for thin altcoins or memecoins (assuming the desk will even quote them, which most refuse to do).

Spreads also widen during volatility. If BTC is making a 3 percent move in an hour, every desk widens its quotes to protect itself from getting picked off. A trade that costs 5 bps during quiet markets might cost 30 bps during a volatile session. Smart traders time their OTC executions to low-vol windows whenever the trade is not urgent. Conversely, market makers run wider spreads at illiquid hours (Asian morning for USD pairs, weekend nights) because hedging is harder.

Settlement Models in OTC Trading

Settlement is the unglamorous part of OTC that determines whether a desk is actually safe to use. The promise of a quote is meaningless if the trade fails to settle, and the history of crypto is full of OTC counterparties that went bust between the trade and the wire. Understanding which model your desk uses is mandatory.

Atomic Swap Settlement

The ideal settlement model is atomic, meaning both legs of the trade happen in the same transaction or not at all. On-chain atomic swaps using hash time-locked contracts (HTLCs) or modern protocols allow two parties to exchange assets across different blockchains without any trust assumption. The buyer's payment and the seller's delivery are mathematically bound together. If either side fails, both legs revert. This is the cleanest possible settlement and removes counterparty risk entirely. The catch is that atomic on-chain settlement is slow and gas-expensive, so it is mostly used for very large institutional trades where the cost is worth the safety.

Custodian-Mediated DVP

Most modern crypto OTC trades settle via a qualified custodian acting as the neutral settlement agent. Both sides deposit their assets to the custodian's escrow, the custodian verifies both legs are present, and then releases them simultaneously in a delivery-versus-payment swap. BitGo, Fireblocks, Copper, Komainu, and Anchorage all offer this service. The custodian carries the operational risk, the trade settles within minutes, and neither side ever has to extend credit to the other. This has become the dominant model for institutional crypto OTC because it combines speed with strong settlement guarantees.

Trust-Based Wire and Transfer

The oldest and riskiest model is simple bilateral settlement. One side wires fiat, the other side transfers crypto. There is no escrow, no custodian, no atomic guarantee. Each side just has to trust the other to perform. This works only between counterparties with deep relationships, established credit lines, and ideally legal master agreements (ISDAs adapted for crypto). When it fails (and it does fail, sometimes catastrophically) the loser has to chase the winner through the courts. Trust-based settlement is still common in altcoin OTC and in regions with limited custodian access, but most major desks have moved away from it.

T+0 vs T+1 Settlement

Crypto OTC almost universally promises T+0, meaning same-day settlement. In practice, T+0 for crypto-to-crypto trades through a custodian usually means under an hour. T+0 for crypto-to-fiat is technically possible if the wire originates during US banking hours, but international wires often slip to T+1 (next business day). This is faster than traditional finance, where equities settle T+1 and many bond markets still run T+2. The speed advantage is one reason institutions accept the spread cost: they get capital back working faster than they would in traditional markets.

Top Crypto OTC Desks in 2026

The OTC landscape is dominated by a small number of firms that handle the vast majority of institutional volume. These desks compete on spread, speed, breadth of assets, and the quality of their settlement infrastructure. Below are the six that matter most as of 2026.

DRW subsidiary, one of the deepest BTC and ETH liquidity providers, known for tight quotes and 24/7 coverage across all major pairs.

London-based algorithmic market maker, dominant in altcoin OTC and DeFi liquidity, supports hundreds of token pairs on principal basis.

SBI-owned principal desk with strong fiat rails in EUR, GBP, and JPY, popular with European funds and family offices.

Reorganized after the 2023 bankruptcy, now focused on spot OTC and structured products with a leaner institutional book.

Mike Novogratz's full-service institutional crypto firm, offers OTC alongside lending, derivatives, and asset management.

Coinbase's institutional arm, integrates OTC execution with prime brokerage, custody, and staking. Largest US-regulated OTC venue.

Beyond these six, there is a tier of strong specialist desks. FalconX has carved out a niche in the US institutional and ETF flow market. Kraken's institutional OTC arm focuses on US and European clients with strong USD and EUR rails. Flow Traders and DV Trading offer market-making OTC for crypto ETFs specifically. OSL serves Asia-Pacific institutions. Each desk has slightly different specialties, fiat coverage, and minimum size requirements, so most sophisticated funds maintain three to five relationships in parallel.

Block Trades vs OTC Sweeps

Inside the OTC world there is an important distinction between a block trade and what desks call an OTC sweep. A block trade is a single large transaction executed at one negotiated price for the full size. The desk takes on the entire position immediately and unwinds it on its own schedule. The client gets a clean, instant fill and walks away. This is the classic OTC trade and is what most people picture when they think of over-the-counter execution.

An OTC sweep, by contrast, is when the desk agrees to work an order over a period of hours or days, executing across multiple venues to minimize impact. The client might say: "I want to buy 5,000 BTC over the next 8 hours, target VWAP plus 10 bps." The desk takes on the execution risk and uses a mix of exchange order books, internal liquidity, and dark pools to fill the order. The client pays for the desk's algorithmic execution skill and gets a benchmarked fill instead of an instant price.

Block trades suit clients who need certainty of execution at a known price right now. Sweeps suit clients who can wait, want to minimize impact, and trust the desk to deliver a benchmark-quality fill. Pricing reflects the difference: block trades carry wider spreads because the desk absorbs all the inventory risk instantly, while sweeps carry tighter effective costs but introduce timing risk. Knowing which product fits your situation is one of the first lessons institutional traders learn when they start using OTC seriously.

Retail OTC: Coinbase Prime, Kraken OTC, and Binance VIP

For most of crypto's history, OTC was strictly an institutional product. Today, the line has blurred. Several major exchanges offer OTC-style execution for high-net-worth retail clients with minimums starting around $100,000. This is not full institutional OTC, but it captures most of the benefits for traders who clear the minimum.

Coinbase Prime is the most accessible institutional-grade OTC platform in the US. Minimums start around $100,000 per trade, and clients get access to a dedicated coverage team, full prime brokerage features, and the same execution engine that powers BlackRock's IBIT and other spot Bitcoin ETFs. The OTC desk supports all major pairs plus a long list of altcoins, with same-day settlement through Coinbase Custody.

Kraken OTC serves a similar segment, with strong US and European fiat rails and a focus on personal service. Minimums hover around $100,000, and the desk is known for handling longer-tail altcoins that other US-regulated desks avoid. Settlement runs through Kraken's regulated custody arm, and trades are typically completed within an hour of confirmation.

Binance VIP is the global heavyweight for non-US clients. The VIP program offers tiered OTC access with minimums depending on volume tier, but in practice clients executing $250,000+ tickets get OTC-style block execution. Binance VIP also extends to a wider universe of altcoins than any US-regulated desk thanks to its global liquidity book. Settlement is internal to Binance, which means counterparty exposure to Binance itself, a tradeoff that experienced institutional traders weigh carefully.

Beyond these three, Gemini, Bitstamp, and OKX also offer OTC services with varying minimums and asset coverage. For retail traders nudging into institutional territory, these exchange-affiliated desks are usually the first stop. They combine familiar onboarding (most are extensions of the standard exchange account) with real OTC pricing for trades large enough to qualify.

KYC and Compliance in OTC Trading

The KYC bar for OTC is dramatically higher than for retail exchange accounts. Where a normal Binance or Coinbase account might require a passport scan and a selfie, opening an OTC relationship requires entity documents, beneficial ownership disclosure, source-of-funds attestation, and ongoing transaction monitoring. The process can take a week for a fast-tracked individual and a month or more for a fund or trading entity with complex ownership.

Most reputable desks require clients to qualify as institutional, professional, or accredited investors depending on jurisdiction. In the US that means meeting the SEC's qualified institutional buyer or accredited investor standards. In Europe it means MiFID II professional client status. In Asia the rules vary by country, but most desks demand demonstrated trading experience, a minimum net worth threshold, and sometimes proof of regulated entity status. Retail-grade KYC simply does not unlock OTC access at the major desks.

Beyond onboarding, ongoing compliance includes screening every trade against sanctions lists, monitoring for unusual patterns, and reporting large transactions to relevant authorities under FinCEN, FATF, and EU AML directives. Desks that fail this often end up in the same place as failed counterparties: out of business or under prosecution. When evaluating a desk, the strength of its compliance program is at least as important as its spreads.

OTC for Memecoins and Altcoins: The Red Flag Zone

One of the dirtiest secrets in crypto is that OTC trading is often used as a vehicle for scams in the memecoin and low-cap altcoin world. Here is how the typical pattern works. A token team holds a large supply of an illiquid token. They cannot dump it on the public market without crashing the price and tipping off chart-watchers. So they reach out privately to a buyer, often a retail "investor" who thinks they are getting a sweet deal, and offer a "discounted" OTC block.

The buyer wires funds or sends stablecoins and receives the tokens. The team takes the cash and disappears. Sometimes the tokens were never going to have any liquidity and the entire chart was wash-traded. Sometimes the team rugs the contract a week later. Sometimes there is enough on-chain liquidity to let the buyer exit, but only at a massive loss. Either way, the OTC structure is what enabled the dump without alerting the market.

If a memecoin team or anonymous Telegram contact offers you an OTC deal at a "discount," treat it as a near-certain scam. Real OTC desks do not quote memecoins because there is no hedge venue, no liquidity, and no reason for a market maker to take the position. The only entities offering memecoin "OTC" are the people trying to exit the bag. Use tools to inspect token concentration before you ever consider a trade like this, and remember that anyone bypassing the public market is usually doing so for reasons that do not benefit you.

Risks of OTC Trading

OTC is not a free upgrade over exchange trading. It comes with its own distinct risk profile that institutional traders manage carefully and that newcomers often underestimate. The four big risks are counterparty risk, settlement failure, market move during negotiation, and bad pricing for the taker.

Counterparty risk is the most obvious. When you trade OTC, the desk is your direct counterparty (or at least your direct intermediary). If the desk fails between trade and settlement, you can lose the entire trade value. This is not theoretical. Several major OTC desks have collapsed since 2018, including Genesis (rescued via Chapter 11), Alameda (caused by the FTX implosion), and various smaller boutiques. Using a custodian-mediated DVP model dramatically reduces this risk but does not eliminate it entirely.

Settlement failure can occur even when the desk is healthy. Wires can be delayed, on-chain confirmations can stall during congestion, custody platforms can have outages. A trade that should settle T+0 sometimes slips to T+1 or worse. During that window, the market can move significantly and either party may attempt to walk away. Strong master agreements and reputable counterparties mitigate this, but you should plan for the possibility before it happens to you.

Market move during negotiation is a subtle one. Even though firm quotes are valid for 5 to 30 seconds, that window is enough for prices to move materially during volatile conditions. If the market rips against the desk while you are deciding, your favorable quote may expire before you can hit it. If the market rips for the desk, the desk will hold the quote and you will execute at a price that is already stale. This is why fast decision-making matters in OTC, and why some traders run automated execution from RFQ to confirmation.

Finally, the simplest risk: bad price. Without the transparency of a public order book, you cannot independently verify that the desk's quote is competitive. The fix is to RFQ multiple desks simultaneously and only lift the tightest quote. Funds that route through a single desk relationship often get worse prices than they would by running a multi-desk RFQ for every trade. This is why an experienced trading desk always maintains at least three to five active OTC relationships.

Who Uses OTC: Funds, Miners, ETFs, and Treasuries

The OTC client base in 2026 is dominated by a handful of well-defined user groups, each with their own reasons for picking up the phone instead of hitting an order book. Understanding who uses OTC and why helps you see where the flow actually comes from.

Crypto-native funds (Multicoin, Pantera, Paradigm, Galaxy, Polychain, and dozens of smaller ones) use OTC for both portfolio entry and exit. Every fund rebalance, every LP distribution, every realized profit flows through OTC because the size exceeds what public books can absorb. These funds usually maintain relationships with five or more desks and RFQ aggressively.

Miners are constant OTC sellers. Every BTC, ETH, or alt-mined operation needs to convert production to fiat or stablecoins on a regular schedule to pay electricity and operating costs. Public selling would suppress the very asset they hold, so miners route through OTC desks. Some larger mining operations (Marathon, Riot, Hut 8) have dedicated relationships and forward sell production months in advance through structured OTC products.

ETF authorized participants are the newest and most important OTC users since US spot Bitcoin ETFs launched. When IBIT, FBTC, or other spot ETFs see net inflows, the AP needs to acquire BTC to create new ETF shares. The size of these flows (sometimes hundreds of millions of dollars in a single day) is far beyond what public books can absorb without massive impact. APs route nearly all of this through OTC desks, primarily Cumberland, Coinbase Prime, and Galaxy.

Corporate treasuries (MicroStrategy being the most famous, but dozens of public and private companies hold BTC on their balance sheet) use OTC for both accumulation and any rare divestment. Treasury-grade execution requires audit trails, KYC integration, and accounting-friendly settlement, all of which OTC desks provide and exchange retail accounts do not.

Beyond these four groups, OTC sees flow from family offices accumulating crypto, sovereign wealth funds taking initial positions, payment processors hedging USDT inflows, and high-net-worth individuals managing concentrated positions. Each segment has different priorities, but they share the common thread of size large enough to make public execution prohibitively expensive.

How OTC Connects to the Broader Crypto Trading Stack

OTC is one execution venue inside a larger ecosystem of trading tools that sophisticated traders combine. Understanding how it fits next to spot trading on public exchanges, perpetual futures, and margin trading products helps you build a complete picture of how institutional crypto actually works.

A typical institutional workflow looks like this. The fund decides to add $20M of BTC exposure. They RFQ four OTC desks, lift the tightest quote, and settle T+0 through a custodian. To hedge the position before settlement, they short an equivalent amount of perpetual futures on a regulated venue. As the OTC trade settles, they unwind the perp short and now hold the clean spot exposure. The OTC desk got their spread, the perp venue got their fees, and the fund got their position with minimum market impact. Each tool played its part.

OTC also connects to stablecoin flows. Most institutional crypto-to-crypto OTC trades settle in USDT or USDC because moving USD via SWIFT is slow and expensive. The growth of regulated stablecoins has been one of the biggest enablers of modern OTC infrastructure, making T+0 settlement viable at institutional scale. And for desks that want extra security around their treasury, multisig wallet setups have become standard alongside custodian relationships.

Frequently Asked Questions

Is OTC trading safe in crypto?

OTC trading with reputable, regulated desks using a qualified custodian for DVP settlement is generally safer than self-custody trading and competitive with exchange trading. The risk profile concentrates around counterparty risk (the desk failing) and settlement risk (the trade not closing cleanly). Using a top-tier desk like Cumberland, Coinbase Prime, or B2C2 with custodian-mediated settlement reduces these risks substantially. Avoid any OTC offered through anonymous Telegram channels, unaudited counterparties, or memecoin teams.

What is the minimum OTC trade size?

Most major desks set minimums between $100,000 and $250,000 per trade. Coinbase Prime starts at around $100,000. Kraken OTC sits near the same level. Binance VIP scales with volume tier but typically targets $250,000 minimums for genuine OTC block execution. Below these levels, traders are usually better served by smart order routing on public exchanges, which can fill smaller trades efficiently without the OTC onboarding burden.

How does an OTC desk make money?

OTC desks make money on the bid/ask spread embedded in their quotes. They do not charge commissions. If a desk quotes you a buy price of $100,500 and a sell price of $100,400 on BTC, the $100 difference per BTC is their gross spread revenue (assuming they capture both sides). On top of pure spread, principal desks also generate revenue from their hedging activities and inventory positioning. Agency desks instead charge an explicit markup or commission on each trade.

Can retail traders use OTC?

Yes, but only retail traders who clear the institutional minimums. If you can execute a single trade of $100,000 or more, you can access Coinbase Prime, Kraken OTC, or similar exchange-affiliated OTC platforms. Below that threshold, you are essentially better off using deep public order books with smart execution tools. For most retail traders, true institutional OTC remains out of reach not because it is forbidden but because the per-trade minimums make it impractical.

Is OTC trading regulated?

OTC desks are regulated to the extent that their jurisdiction regulates crypto firms generally. In the US, major desks operate under FinCEN money services business registration, state-level money transmitter licenses, and SEC oversight when relevant. In the EU, MiCA applies. In the UK, FCA registration is required. The trades themselves are not exchange-listed and thus do not have the same disclosure requirements, but the desks operating them are heavily regulated entities subject to AML, sanctions, and capital requirements. Compared to retail exchange trading, OTC is arguably more regulated, not less.

What is the difference between a block trade and OTC?

A block trade is a specific type of OTC trade: a single, large, off-book transaction executed at one negotiated price for the full size, with the desk taking on the entire position instantly. OTC is the broader category that includes block trades plus other off-exchange execution styles such as sweeps (working an order over time across venues), structured products (forward sales, options, lending), and bilateral swaps. All block trades are OTC, but not all OTC trades are block trades.

Do I need a special wallet for OTC?

Not strictly. The desk and its custodian handle the actual settlement infrastructure. What you need is a deposit address (or wallet) under your control to receive the assets after settlement, and a funding source (wire or stablecoin transfer) to send funds. Many institutional users settle directly to a qualified custody account rather than a personal wallet to maintain audit trails and security. If you are using leverage trading on top of an OTC spot position, the leverage venue may also require its own deposit setup.

Conclusion

Crypto OTC trading is the institutional layer that powers most of the real volume in the market. While retail traders chase candles on a public chart, funds, miners, ETFs, and corporate treasuries quietly execute the trades that actually move the needle through OTC desks. The product solves a real problem: large trades cannot survive public order books without massive slippage. The solution is privately negotiated execution with firm quotes, fast settlement, and minimum size requirements that filter out most retail flow.

If you ever cross the threshold from retail to institutional, OTC becomes mandatory rather than optional. The economics simply do not work otherwise. Even at the high end of retail, a $250,000 trade executed through Coinbase Prime or Kraken OTC will materially outperform the same trade smashed into a public order book at market. The savings from a single well-executed OTC trade can dwarf years of subscription costs and data feeds combined.

What you should take away from this guide: the OTC product is fundamentally about size and privacy, the cost is the spread (not commissions), the safe settlement model is custodian-mediated DVP, the dominant desks are Cumberland, Wintermute, B2C2, Genesis, Galaxy, and Coinbase Prime, and the red flag is anyone offering OTC on illiquid memecoins. Memorize that list and you will already understand the market better than 90 percent of the retail audience. Use the desks, respect the risks, and remember that the price you see on the chart is only the tip of the volume iceberg.

Frequently Asked Questions

What is OTC trading in crypto?

OTC trading in crypto involves direct, peer-to-peer transactions of digital assets outside of traditional exchanges. It often facilitates larger trades that might impact market prices on public exchanges.

Why would someone use OTC trading for crypto?

Individuals and institutions use OTC desks for large volume trades to minimize price slippage and impact on public exchange order books. It also offers more privacy and personalized service.

How does an OTC crypto trade work?

A buyer or seller contacts an OTC desk with their desired trade. The desk then sources the cryptocurrency or fiat, agrees on a price, and facilitates the direct transfer between parties.

What are the benefits of OTC trading in crypto?

Benefits include price stability for large orders, enhanced privacy, access to deeper liquidity pools, and personalized support from the OTC desk. It avoids the volatility of public exchanges for significant transactions.

Will OTC crypto trading change by 2026?

By 2026, OTC crypto trading is expected to become more regulated, with increased institutional participation and sophisticated technological integration. Enhanced compliance and security measures will likely be standard.