Wash Trading in Crypto: Red Flags Explained

— By Tony Rabbit in Tutorials

Wash trading in crypto explained: spot the red flags on exchanges and DEXs, from wallet loops and suspicious order flow to shallow liquidity traps.

Intent check: This page focuses on exchange-wide and DEX-wide wash-trading red flags. If you want the base definition first, read What Is Wash Trading in Crypto?. If you want the memecoin-launch angle specifically, read How to Detect Fake Volume in Memecoins: Launch Red Flags (2026).

Volume is the most lied-about number in crypto. Every screener, every ranking, every "trending" tab on every exchange ultimately sorts tokens by some flavor of trading volume, and that single metric is the easiest thing in the entire industry to fake. A trader with two wallets, a few thousand dollars, and a couple of scripts can pump a brand new token from invisible to "top 100 by 24h volume" inside an afternoon. They are not buying or selling anything, in any meaningful sense. They are sending their own money back to themselves and counting it twice.

This practice is called wash trading, and in 2026 it is still everywhere. It distorts rankings on CoinMarketCap and CoinGecko, it inflates the perceived activity of memecoins on every DEX liquidity pair, it manufactures the urgency that pushes retail traders into bad entries, and it has been used to extract billions of dollars from airdrop programs, NFT royalty contracts, and exchange rebate schemes. If you do not know how to spot it, you will routinely confuse engineered noise for real demand.

In this guide you will learn what wash trading actually is, how it works at the wallet level on both centralized exchanges and DEXs, why so many actors keep doing it despite years of bans and regulation, and most importantly how to filter it out as a retail trader. By the end you should be able to look at a token on a screener and form a defensible opinion about how much of its volume is real, before you risk a single dollar of size.

What Is Wash Trading?

Wash trading is the practice of buying and selling the same asset to yourself, or coordinating with someone else to do the same, in order to create the appearance of trading activity that does not reflect real market demand. The defining feature is that the beneficial ownership of the asset does not actually change. The same person, or the same coordinated group, controls both sides of the trade. Volume is produced. Price prints are produced. But no new buyer with an independent view has entered the market.

The practice is much older than crypto. It originated in traditional equity markets in the late 19th century, where pools of investors would coordinate to trade shares back and forth at rising prices to attract outside buyers, who would then provide the real exit liquidity for the pool. The 1934 Securities Exchange Act in the United States made this explicitly illegal under what later became Section 9(a)(1), and the Commodity Futures Trading Commission applies a similar prohibition to futures markets under the Commodity Exchange Act. In short, in regulated TradFi, wash trading is a felony.

Under SEC rules, a trade is considered a wash sale when it is "a transaction in a security that involves no change in beneficial ownership," entered into for the purpose of creating "a false or misleading appearance of active trading" or "a false or misleading appearance with respect to the market for any such security." Note the two-part test: no economic change, plus an intent to mislead. Both have to be present for a regulator to bring a manipulation case. In practice, regulators infer intent from the pattern. If two accounts at the same broker trade the same illiquid stock against each other 200 times in a day in matched sizes, no one believes it is a coincidence.

Crypto adopted the term, but the mechanics are slightly different from TradFi. In crypto you do not need a broker, you do not need a clearing house, and you do not need anyone's permission to open a wallet. You can spin up ten wallets in three minutes, fund them from a centralized exchange, and start trading them against each other on any decentralized exchange you like. The cost of entry into market manipulation collapsed from "you need a Wall Street trading desk" to "you need MetaMask and a few hundred dollars in gas."

How Wash Trading Works in Crypto

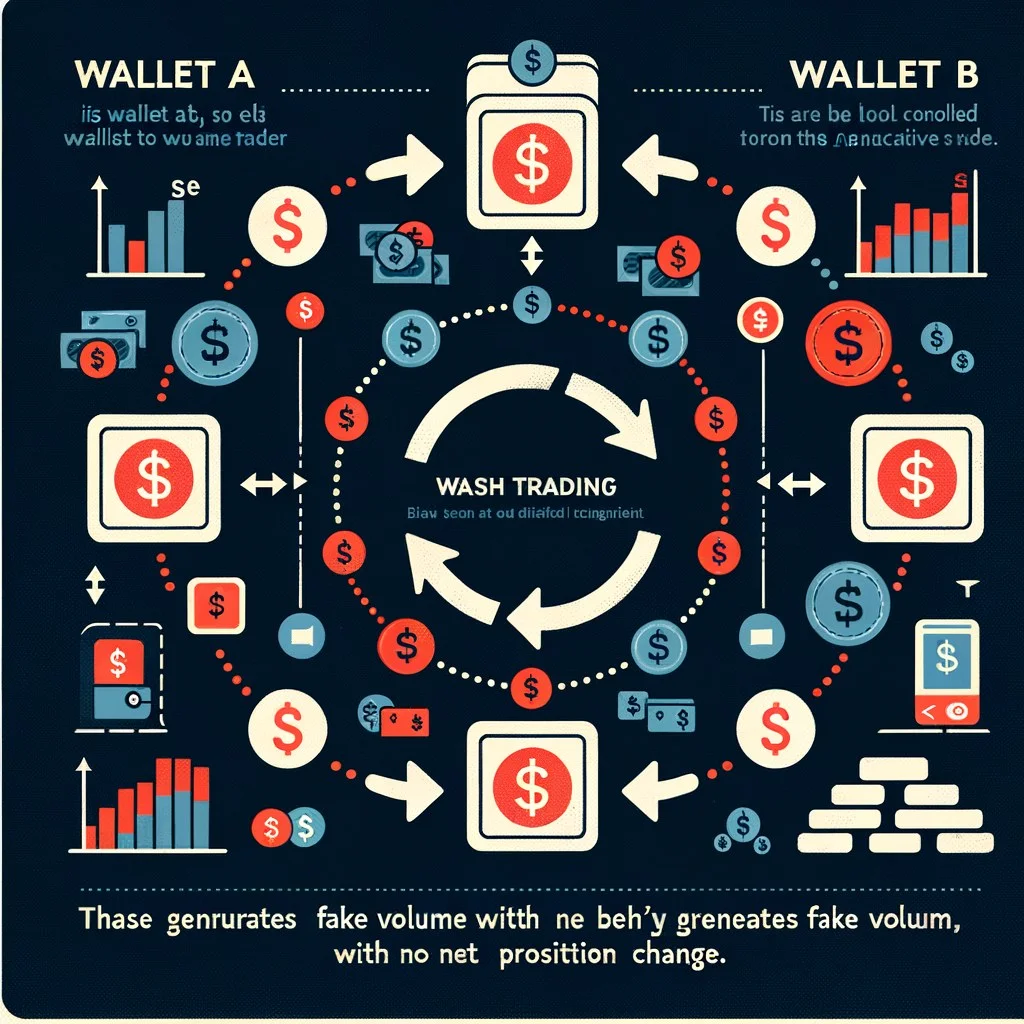

The simplest version of crypto wash trading is the round-trip trade. The operator controls two wallets, A and B. Wallet A sells 10,000 tokens to wallet B at $0.10 each. A few seconds or a few minutes later, wallet B sells the same 10,000 tokens back to wallet A at roughly the same price. From the outside, the pair just printed $2,000 of volume on the chart. From the inside, nothing happened. The operator still owns the same 10,000 tokens, minus whatever they paid in gas fees and DEX swap fees. They moved tokens out of their left pocket and back into their left pocket.

More sophisticated operators do not use only two wallets. They use rings of sybil wallets, sometimes dozens or hundreds, with funding chains that loop through mixers or multiple bridges to make the link between wallets harder to detect on chain. They vary trade sizes, they space trades out across uneven time intervals, and they sometimes route through real third-party liquidity to break the simple "wallet A sells, wallet B buys, the end" pattern. The goal is to make the volume look organic to a casual observer while still keeping the underlying tokens in the same beneficial hands.

On a centralized exchange, the mechanics are different in form but identical in substance. The operator does not need two on-chain wallets, they just need two exchange accounts, or a single account with API keys that places matched buy and sell orders against itself in the order book. Because the exchange handles off-chain matching, the trades never appear on any blockchain. They only exist inside the exchange's database. From the public's perspective, the only evidence is the printed tape and the volume number. There is no chain-level forensic trail at all.

This asymmetry is one of the most important things to understand. DEX wash trading is loud. Every transaction is on chain, every wallet address is public, and anyone with a block explorer can reconstruct the pattern after the fact. CEX wash trading is quiet. It happens inside private infrastructure, and unless the exchange itself reports it, the public has no way to prove it ever happened. Most of the famous studies showing that the majority of CEX volume is fake have had to infer it statistically from order book and tape patterns, not from direct evidence.

Why Wash Trading Exists: Six Motivations

If wash trading just moves your own money in a circle and costs you fees, why does anyone do it? Because the goal is never the trade itself. The goal is the side effect that the trade produces. Here are the six biggest reasons operators wash, ordered roughly by how much money is involved.

CoinMarketCap, CoinGecko and exchange "trending" tabs sort by 24h volume. Higher rank means more eyeballs, more clicks, more retail discovery. Wash trading is the cheapest way to climb that list.

Many CEX listing committees and DEX aggregator algos use volume as a quality signal. Fake volume can bait an exchange into listing a token or push it onto "hot" feeds that drive trader inflows.

Selling a JPEG to yourself for 50 ETH sets a new "floor" on the collection. Naive buyers anchor to that print, and the operator can then dump real inventory into the inflated bid stack.

Maker-taker fee schedules pay rebates to liquidity providers. Wash trading farms those rebates at scale. If the rebate exceeds the round-trip cost, every loop is pure profit.

A green candle on huge volume looks like real demand. Retail piles in. Insiders use the inbound real flow as exit liquidity. This is the core dynamic behind most memecoin pumps.

Many protocols allocate airdrop tokens based on trading volume. Sybil farmers wash trade through the protocol to maximize their share. Billions in airdrop value has been farmed this way since 2021.

Each of these motivations creates a slightly different fingerprint, and that is good news for anyone trying to detect wash trading. A trader farming rebates leaves a very different on-chain pattern than a trader trying to pump a memecoin's ranking, and both look different from an NFT collection manipulator. We will get into the forensics in a later section.

Wash Trading on Centralized Exchanges

Centralized exchanges have been the dominant venue for wash trading throughout the entire history of crypto. The reasons are structural. Off-chain matching means trades are invisible to outside investigators, fee rebates create direct economic incentives for self-trading, and ranking competition between exchanges creates pressure to report inflated numbers even when the exchange itself is not directly participating.

The single most influential piece of research on CEX wash trading is the 2019 Bitwise Asset Management study, which was submitted to the SEC as part of a Bitcoin ETF application. Bitwise analyzed reported volume across the 81 exchanges then listed on CoinMarketCap and concluded that roughly 95% of reported Bitcoin spot volume was fake. Their methodology compared volume against several "tells" of real trading: trade size distributions following Benford's Law, the ratio of volume to bid-ask spread, and consistency between exchange volume and verifiable on-chain settlement flows. Almost every exchange outside the top 10 failed these tests catastrophically.

The 2019 figure has improved somewhat in the years since, partly because the worst offenders died, partly because the survivors got better at hiding it, and partly because methodologies have evolved. Subsequent studies from Nomic Labs, the National Bureau of Economic Research and Forbes have put more recent estimates anywhere from 40% to 70% of all reported CEX volume being non-genuine. Even the optimistic end of that range means that nearly half the volume number you see on any given mid-tier exchange is invented.

Why does it persist? Because rankings drive listings, listings drive new user signups, signups drive real fee revenue, and the cost of producing fake volume is essentially zero for an exchange that controls its own internal accounts. The economic logic for an unregulated offshore venue is almost irresistible. The only thing holding the practice back is the risk of being publicly exposed and losing credibility with the small slice of users who actually pay attention.

Wash Trading on Decentralized Exchanges

DEX wash trading exploded after 2020 for two reasons. First, decentralized exchanges have no listing process at all. Anyone can create a pool, and any pool gets indexed on every DEX screener immediately. Second, the rise of MEV infrastructure and cheap layer-2 chains made it economically viable to run high-frequency wash bots that would have been prohibitively expensive on Ethereum mainnet in 2020.

The typical pattern on a DEX involves a small ring of sybil wallets that take turns swapping a token against its paired liquidity. Each swap consumes a small portion of the pool's liquidity, gets sandwiched by its own counterpart swap a few blocks later, and pays the DEX fee both ways. The fee is a real cost, but the operator does not care, because the goal is the volume print, not the fee. A token with $50,000 of liquidity can easily produce $5 million of reported daily volume through this kind of churn, and the resulting volume-to-mcap ratio is the smoking gun.

Airdrop farming is the other massive driver of DEX wash trading in 2026. Whenever a major protocol announces that it will allocate tokens to "active users" based on past trading volume, an army of sybil operators spins up thousands of wallets and starts wash trading through the protocol. The 2021 dYdX airdrop, the 2022 Optimism airdrops, the 2023 Arbitrum drop, and a long list of newer L2 distributions have all been hit by this. The protocols know it is happening, they just cannot fully filter it out because the wash trades are technically real trades that pay real fees and use the real product. The operator is gaming a metric, not breaking a rule.

A subtler form of DEX wash trading uses an MEV bot as a partial counterparty. The operator's primary wallet places a buy. An MEV searcher's sandwich bot front-runs and back-runs it. The operator earns the volume credit, the MEV bot earns the sandwich profit, and both walk away happy at the expense of any unrelated trader who happens to interact with that pool. This pattern is hard to call wash trading in the strict sense, because real economic activity is occurring on both sides, but it is the same family of behavior. You should treat any token with extreme MEV activity in its pool with the same skepticism you would apply to a directly washed token.

NFT Wash Trading

NFTs deserve their own section because the wash trading dynamic there is even more extreme. With fungible tokens, you at least need to maintain a real liquidity pool that the wash trading flows through. With NFTs, an asset is unique and indivisible, which means a single self-trade can set the entire "floor price" of a collection. Sell a JPEG to yourself for 50 ETH, and every screener now reports that the collection has a 50 ETH floor, even if not a single other buyer in the world would pay more than 0.1 ETH for one.

The two most documented historical cases happened on LooksRare and Blur. LooksRare launched in early 2022 with a token-emission model that rewarded users in LOOKS tokens proportional to the platform's trading volume. Within days, traders discovered that they could earn far more in LOOKS rewards than they spent in royalties and fees by trading high-value NFTs back and forth between their own wallets. At one point, more than 95% of LooksRare's reported volume was estimated to be wash trading. The platform's "real" trading was a tiny fraction of what the headline numbers suggested.

Blur in 2023 introduced its own token incentive system that rewarded both listing activity and trading activity. Once again, wash farmers descended on the platform and produced billions in headline volume that was overwhelmingly non-organic. Analysts at CryptoSlam and Chainalysis later published forensic breakdowns showing that during peak farming periods, the majority of "blue chip" NFT volume on Blur traced back to a small number of farmer-controlled wallet clusters.

The retail-trader trap is simple. A new collector sees that an NFT collection has $20 million in 30-day volume and a 5 ETH floor, both rising. They feel like they are getting in on a winner. They buy at 5 ETH. The wash trading stops. The real bid drops to 0.3 ETH. They are down 94%. This sequence has played out hundreds of times since 2021, and it continues today on smaller and lesser-known NFT venues. If you collect NFTs at all, you have to learn to read wash trading patterns.

Organic Volume vs Wash Volume

Before we get into specific forensic tools, it helps to have a clean mental picture of what organic and wash volume actually look like. The comparison below is what you should be looking for when you scan any new token.

- Diverse wallet base. Hundreds or thousands of unique addresses, with new ones constantly appearing.

- Varied trade sizes. A natural distribution from $20 retail buys up to occasional whale prints.

- Real price discovery. Trades move the price as supply and demand pressure shift.

- Irregular time pattern. Spikes around news, lulls overnight, weekend variation.

- Healthy depth chart. Order book or pool liquidity scales with the volume.

- Narrow wallet ring. The same handful of addresses appearing on both sides of trades repeatedly.

- Identical or rhythmic sizes. Suspiciously uniform trade amounts like 1,000 tokens exactly.

- No real price impact. Volume prints but the chart barely moves, or moves in mechanical sawtooth patterns.

- Bot-like time pattern. Trades every N seconds, 24/7, no human rhythm.

- Volume dwarfs liquidity. Daily volume is 50x to 500x the actual pool liquidity.

Note the asymmetry of this list. Organic volume has many independent signals lining up by accident. Wash volume has many statistical irregularities lining up because a small number of operators are producing all of it. You are not looking for one perfect tell. You are looking for a stack of suspicious facts that, taken together, point in the same direction.

How to Spot Wash Trading: On-Chain Forensics

On a DEX, almost everything you need is publicly available if you know where to look. Here is the practical forensic stack, ordered from cheapest to most thorough.

Volume-to-holder ratio. A real token with $10 million in daily volume should have thousands of holders. If a token is printing $10 million daily and has 38 holders, you are looking at engineered volume. The math just does not work for a normal market. This is the fastest and most reliable single check. You can pull it from any DEX explorer or holder analytics tool in seconds.

Recurring wallet pairs. Open the trade history for the pair. Look at the buyer and seller addresses on the last 100 trades. If the same five or ten wallet addresses are appearing on both sides repeatedly, those are almost certainly the operator's wallets, and the volume between them is fake. Real markets have hundreds of distinct counterparties in any given 100-trade window.

Identical-size trades. Sort the trade history by size. If you see clusters of trades at suspiciously round and identical amounts, especially in the same time window, that is a script speaking. Humans place trades for "$200 worth of token" or "0.5 ETH worth," which produces messy non-round token amounts. Bots place trades for "exactly 1,000 tokens" because that is what they were programmed to do.

Time pattern analysis. Plot the timestamps of trades on a 24-hour clock. Organic volume has a circadian rhythm. It rises during US and European market hours, falls in the dead of night, varies on weekends, and spikes around news. Wash volume is often perfectly flat across all hours because the bot does not sleep. A pair that prints exactly $50,000 of volume every hour for three days straight is washing.

Depth chart vs volume mismatch. Pull the depth chart or pool liquidity. Real markets cannot sustainably produce volume that is many multiples of their depth. If a pair has $20,000 of liquidity but prints $5 million in daily volume, that is mathematically suspicious. Real traders trying to push that much volume through a $20,000 pool would cause catastrophic slippage on every trade, and the chart would look like a sawtooth. If the chart is calm and the volume is huge, the volume is fake.

You can apply the same kind of logic on a CEX, but you only see the order book and the tape, not the wallets. The most useful CEX checks are trade size distribution analysis (look for unnatural clustering at specific sizes), spread-vs-volume sanity checks (a tight spread combined with low real depth and huge volume is a tell), and cross-exchange comparison. If a token trades $50 million daily on a tier-3 exchange and $300,000 daily on Binance, the tier-3 exchange is almost certainly washing.

Practical Red Flags for Retail Traders

You will not always have time to run a full forensic audit on a token before you decide whether to enter or pass. For day-to-day screening, this is the short list of red flags that should trigger a hard skepticism check.

If a "top 100" token has 95% wash volume, the real market cap is a fraction of what you see. A token with $200M in reported market cap supported by fake volume might have only a few million dollars of genuine demand sitting behind it. When the wash bots stop, the real bid will discover itself, and that real bid is usually a savage 80-95% lower than the price you bought at.

DEX volume far greater than liquidity. If a token is showing daily DEX volume that is more than 5x its total locked liquidity, something is off. The honest version of this ratio for a real, actively traded token is usually somewhere between 0.5x and 3x. A 50x or 100x ratio is a wash trading neon sign.

Tiny holder count. If the token shows multimillion-dollar volume but the holder count is under 200, you can be almost certain the volume is fake. Real demand requires real buyers, and real buyers are unique wallets.

Uniform trade sizes. Pull the recent trades feed on any DEX screener. If you see clean rounded numbers like 10,000.00 tokens repeating over and over with similar timestamps, you are looking at a bot.

Top wallets heavily concentrated. If the top 10 wallets hold 80% or more of supply, then almost by definition any large volume is being produced by those same wallets, because nobody else has enough tokens to move that volume. Check the holder distribution before you check the volume.

Bot-like time pattern. If the volume is uncannily steady across hours and days, with no overnight lull and no spikes, you are watching a machine. Real markets breathe. Wash markets metronome.

Pair these red flags with our broader rug pull avoidance checklist for any new token. Wash trading is one of the highest-correlation precursors to a rug, because both behaviors come from the same kind of operator, and tokens that are aggressively washed in their early days are very rarely projects with long-term ambitions.

Tools That Help Detect Wash Trading

You do not have to do all of this analysis by hand. Several tools surface the relevant data quickly enough to use during live trading decisions.

DEXTools. The platform's pair explorer and audit panels surface most of the metrics you need at a glance: holder count, top holder concentration, liquidity, recent trades, and unique buyer/seller counts. The "trades" tab lets you eyeball recurring wallet pairs, and the holder analytics flag any address controlling an unusually large share. You can also combine this with our meme coin screener setup to filter out the worst offenders automatically before you ever click into a token.

On-chain explorers. Etherscan, Solscan, BscScan and their equivalents on every other chain let you click any wallet and see its full transaction history. If you suspect wash trading, click the two most active wallets in the pair's recent trades. If both wallets show identical funding sources, similar gas patterns, and a trade history dominated by the same token, they are almost certainly controlled by the same operator.

Holder analysis tools. Bubblemaps, Arkham, and Nansen all specialize in clustering related wallets into single "entities" using funding flows and behavioral patterns. Drop a suspicious token into any of these and look at whether the top 20 wallets cluster into a handful of entity blobs. If five blobs control 90% of supply, the volume between them is wash regardless of how many surface-level wallets are involved.

Social signals. Real tokens with real volume usually have real communities. If a token is printing $50 million in daily volume but its Telegram has 200 members and its Twitter account has zero engagement on every post, the volume is not coming from a community. It is coming from a few scripts. This is a soft signal but it is consistently useful.

Legal Status and Regulation

The legal picture is messier in crypto than in traditional securities, but it is rapidly converging on "wash trading is illegal" across all major jurisdictions. Here is the current state of play in 2026.

United States. The SEC treats wash trading in any security as market manipulation under the 1934 Securities Exchange Act. The CFTC treats it as manipulation in any commodity, including Bitcoin and Ether spot markets in some interpretations and crypto futures unambiguously. The DOJ has brought criminal cases for wash trading in crypto, most notably against the operators of the Mango Markets exploit and against several quant traders charged for spoofing and wash trading on regulated futures venues. If you wash trade a US-domiciled token or do it from US infrastructure, you are exposed to both civil and criminal liability.

European Union. The Markets in Crypto-Assets regulation (MiCA), which fully came into force in 2024, explicitly prohibits market manipulation including wash trading, matched orders, and "creating a false or misleading impression as to the supply, demand or price" of crypto-assets. MiCA gives the European Securities and Markets Authority and national competent authorities direct enforcement powers, and the penalties include fines of up to 15% of annual turnover for legal persons and bans on trading for individuals.

Exchange terms of service. Every major centralized exchange in 2026, including Binance, Coinbase, Kraken, OKX, and Bybit, prohibits wash trading in their terms of service and reserves the right to freeze accounts and seize funds discovered to be engaged in it. Enforcement is uneven, but it is real. Many traders have had accounts permanently closed and balances confiscated for self-trading.

The practical takeaway is that wash trading sits in an enforcement gray zone for individual retail-level offenders on decentralized venues, but it is unambiguously illegal in the US, EU, and most other large jurisdictions, and it can absolutely be prosecuted. If you are tempted to "just farm a quick airdrop" by spinning up a few sybil wallets, understand that you are committing market manipulation and exchange ToS violations, and that on-chain forensics gets better every year.

Famous Wash Trading Cases

Bitwise 2019 CEX report. Already mentioned, but it deserves a second pass. The Bitwise filing was the single most important piece of public evidence that the majority of crypto exchange volume had been fake for years. It led directly to CoinMarketCap and CoinGecko reforming their volume rankings and to multiple SEC ETF denials referencing the report. It also moved the Overton window on what "trusted volume" meant industry-wide.

LooksRare and Blur NFT wash farming. The token-reward design of both platforms accidentally turned wash trading into a profitable strategy for any user who could afford the royalties and fees. At peak, more than 95% of LooksRare's volume and a clear majority of Blur's volume was wash trading. Both platforms eventually adjusted their reward structures, but the damage to retail collectors who anchored to those inflated floors was permanent.

Nomic Labs and CER reports. Multiple research groups including Nomic Labs, the Crypto Exchange Ranks team, and Forbes have published their own takedowns of CEX wash trading, each using slightly different methodologies and each independently confirming that a substantial fraction (40% to 70%) of reported volume across the industry is non-genuine.

MultiBit and Coin Flow. Smaller documented cases where specific exchanges or specific token issuers were caught running coordinated wash trading operations. These tend not to make headlines outside crypto media, but they pile up. If you sort historical exchange closures by reported "trading volume to actual user base" ratio, you can almost predict which exchanges will fail next purely from the wash signature.

Mango Markets and Avraham Eisenberg. Eisenberg was convicted in 2024 for the Mango Markets exploit, which included elements of market manipulation closely related to wash trading mechanics. The case was notable because it was one of the first US criminal convictions for crypto market manipulation that turned on the specific manipulative trade pattern rather than on any underlying theft of funds.

Airdrop sybil purges. Several major protocols, including Arbitrum, Optimism, LayerZero, and Hop, have published detailed sybil-cluster reports after their token launches identifying tens of thousands of farmer wallets and excluding them from their airdrops. These reports are public goldmines for understanding what wash trading patterns look like at scale.

How to Trade Knowing Wash Trading Exists

Once you accept that a large portion of the volume you see on every screener is fake, your trading process has to change. Here is how experienced traders actually adjust.

Discount the volume. Whenever you look at a token's volume number, mentally divide it by some skepticism multiplier. For top-10 chains and tokens, 1.5x to 2x is usually a safe haircut. For unknown small-caps on mid-tier CEXs, divide by 5 or 10. For brand new memecoins that just appeared on a DEX, assume by default that 90% of the volume is wash unless you can prove otherwise.

Look at liquidity depth, not volume. Liquidity is much harder to fake than volume, because real liquidity is real capital sitting in a pool or in resting orders. A token with $5 million of locked, on-chain liquidity is meaningfully different from a token with $50,000 of liquidity, regardless of which one prints higher volume on the day. Lean on depth charts when you are sizing positions.

Use TWAP execution. When you do decide to enter, especially in size, split your orders out over time with a time-weighted average price strategy. If the token you are buying turns out to be heavily washed and the volume collapses when the bots stop, TWAP execution gives you a chance to notice the regime change mid-entry and pull out of the rest of the order. A single market buy at the top of a wash-pumped chart has no escape hatch.

Read slippage as a tell. If you try to price out a normal-sized swap and the slippage estimate is enormous despite the token allegedly having huge volume, that is a wash trading confession in real time. Real volume requires real depth, and real depth means small swaps barely move the price.

Watch for the sandwich. Heavily washed pools are often also sandwich attack zones, because MEV bots love thin pools with high apparent activity. If you do trade in this kind of environment, use private RPC submission or MEV-protected swap routes to avoid being chopped on every entry and exit.

Avoid the first 48 hours. The vast majority of wash trading on DEXs happens in the first few days of a token's life, while the operators are trying to bait initial retail flow. If you simply refuse to enter any new token in its first 48 hours, you sidestep most of the wash trading trap by default, at the cost of giving up some upside on a few legitimate launches. For most traders, that is a profitable trade-off over a full cycle.

Cross-check tokenomics. Wash trading is almost always paired with bad tokenomics. Concentrated supply, opaque vesting, and undisclosed team allocations are the natural companion to fake volume, because the same operators who are willing to lie about volume are willing to lie about everything else. A clean tokenomics check filters out most washed tokens by accident.

Finally, get comfortable being skeptical. Wash trading exists because the industry rewards loud volume numbers, and you cannot fix the industry. You can only refuse to trust those numbers blindly. Treating every "trending" token as guilty until proven innocent is the single highest-EV mental adjustment a retail trader can make, and it costs nothing.

Frequently Asked Questions

Is wash trading illegal?

Yes, in every major jurisdiction. The US prohibits it under the Securities Exchange Act and the Commodity Exchange Act. The EU prohibits it explicitly under MiCA. Every major centralized exchange bans it in their terms of service. The enforcement gray zone is largely about whether regulators choose to prosecute small individual offenders on decentralized venues, not about whether the underlying behavior is illegal. It is illegal.

How do exchanges detect wash trading?

Exchanges use a mix of account-linking heuristics (KYC matches, shared IP addresses, shared device fingerprints, related funding sources), trade pattern analysis (self-crossing orders, suspicious matched order behavior), and statistical anomaly detection (trade size clustering, time pattern regularities). The largest exchanges have dedicated surveillance teams modeled on traditional securities market surveillance. None of these systems are perfect, and operators with deep operational discipline can evade detection, but the cost of doing so meaningfully reduces the profitability of small-scale wash trading.

What percentage of crypto volume is wash trading?

It depends heavily on which subset of the market you mean. For top-tier exchanges and top-cap tokens, the figure is probably under 20%. For mid-tier centralized exchanges and small-cap tokens, the figure ranges from 40% to 70% depending on the study. For brand new memecoins on DEXs, the figure routinely exceeds 90% in the first days of trading. The 2019 Bitwise report famously found 95% of reported Bitcoin spot volume on the long tail of exchanges was fake. The picture has improved since then but the fundamental dynamic is unchanged.

How can I tell if a specific token has wash volume?

Run through the practical red flag checklist: volume-to-liquidity ratio, holder count, top wallet concentration, uniformity of trade sizes, and time pattern of trades. If three or more of those flags are red, treat the token as washed by default. Cross-check with a holder clustering tool like Bubblemaps or Arkham to see if the active wallets resolve into a small number of entity clusters. None of this is bulletproof, but together it filters out the overwhelming majority of fake-volume tokens.

Is wash trading the same as a pump and dump?

No, but they often happen together. A pump and dump is a scheme where insiders accumulate a token quietly, then drive the price up through coordinated buying and promotion, and finally distribute their inventory into retail buyers at the top. Wash trading is one of the techniques pump and dump operators use to attract attention during the pump phase, because fake volume helps the token appear on screener "trending" lists. Wash trading can also exist without a price pump (for example, airdrop farming or rebate harvesting), and pump and dumps can theoretically happen without wash trading. But in practice, the same operators run both.

Can wash trading move a real market price long-term?

Not on its own. Wash trading manufactures volume and attention. If real buyers do not arrive, the operator eventually exhausts their capital on fees and stops, and the price reverts. The real risk is that wash trading attracts enough real buyers during its active phase that the price moves to a level genuinely supported by new demand. In that scenario, the wash trading served as marketing for what becomes a real, if often briefly, market. This is why fake volume is so dangerous for retail. It is not that wash trading itself moves the price. It is that wash trading recruits real buyers who then move the price, and those real buyers usually arrive late.

Conclusion

Wash trading is the original sin of crypto market data. It has been present since the first centralized exchanges launched, it has been documented by every major research group in the industry, and it persists in 2026 because the incentives are still aligned to reward it. Rankings sort by volume. Listings care about volume. Retail looks at volume. Airdrops measure volume. The whole stack treats volume as a proxy for legitimacy, and the entire stack can be gamed by any operator with two wallets and a script.

The defense is not technical. It is dispositional. Treat every volume number as a claim that has to be verified, not a fact you can rely on. Develop a fast mental checklist of red flags. Lean on the metrics that are harder to fake, including liquidity depth, holder count, holder distribution, and chain-level forensic clustering. Pair this with awareness of related manipulation patterns like MEV, sandwich attacks, and pump and dumps, all of which often co-occur with wash trading and reinforce each other.

Most importantly, give up on the idea that the screener is your friend. The screener is showing you what other people, many of them adversaries, want you to see. Your job as a retail trader is to look behind the screener at the underlying chain data, the wallet patterns, and the actual depth of demand. That work is unglamorous and slow, but it is the difference between being the exit liquidity for a wash trading operator and being the rare retail trader who consistently avoids the trap. The number on the volume column is the most lied-about number in crypto. Stop trusting it, and you will be a better trader by the end of the week.

Related Guides

- How to Detect Fake Volume in Crypto: Memecoin Red Flags (2026)

- Fake Volume vs Real Demand: How to Spot Artificial Momentum in DeFi Trading

- When Not to Trade: 12 Red Flags Every DeFi Trader Should Know

- How to Evaluate Yield Farms in Crypto: APY Quality, Risks and Red Flags (2026)

- What Is an Admin Wallet in Crypto? Red Flags

- What Is On