What Is Liquidity Mining? DeFi Rewards Guide

— By Tony Rabbit in Tutorials

Liquidity mining explained: a step by step DeFi rewards workflow, how it differs from staking and yield farming, top protocols, and the key risks in 2026.

Decentralized finance bootstrapped trillions of dollars in cumulative trading volume by solving one fundamental problem: how do you convince total strangers to lock their money into a smart contract that has no marketing department, no sales team, and no central authority promising returns? The answer that reshaped the industry was liquidity mining, an incentive mechanism that rewards users for providing the capital that decentralized exchanges and lending markets need to function. Without liquidity mining, the entire DeFi ecosystem we know today would not exist.

Liquidity mining turned passive token holders into active participants and turned protocols into bootstrapped economies. By distributing governance tokens to users who deposited assets into liquidity pools, projects could grow from zero to billions in total value locked within weeks. This guide unpacks how liquidity mining works in 2026, where it sits between simple staking and high-risk yield farming, what the modern vote-escrow models like veCRV and ve(3,3) actually do, and how to evaluate whether providing liquidity makes sense for your portfolio.

By the end of this article you will understand the four-step workflow of becoming a liquidity miner, the differences between stable-pair and volatile-pair strategies, how to calculate net profitability after accounting for impermanent loss, gas, and reward token slippage, and which protocols dominate the landscape today. This is written for intermediate DeFi users who already understand swapping tokens on a decentralized exchange and want to take the next step into earning yield by becoming a liquidity provider.

What Is Liquidity Mining?

Liquidity mining is the practice of depositing two tokens into a liquidity pool on a decentralized exchange or lending protocol, receiving an LP token that represents your share of the pool, and then staking that LP token into a rewards contract to earn an additional stream of the protocol's native governance token. You earn two simultaneous yields: the trading fees generated by the pool, and the freshly minted reward tokens the protocol distributes to incentivize liquidity. This dual reward structure is what separates liquidity mining from any other form of crypto yield.

Classic staking is fundamentally different. When you stake ETH or any proof-of-stake asset, you are locking a single asset to help secure a blockchain and earning inflation rewards plus transaction fees. You do not take on price risk from a second asset, you do not face impermanent loss, and your reward is denominated in the same token you staked. Liquidity mining, by contrast, exposes you to two assets, requires you to deposit them in a specific ratio, and pays you in a third token that often has its own volatility profile. It is closer to running a small market-making business than to earning interest on a savings account.

The mechanism only works because decentralized exchanges need deep order books to function. A pool with $10,000 of liquidity will produce massive slippage on a $1,000 trade. A pool with $100 million can absorb the same trade with minimal price impact. Protocols pay liquidity miners because deeper pools attract more traders, more traders generate more fees, and more fees attract more liquidity. Liquidity mining is the flywheel that kicks the cycle into motion.

The 4-Step Liquidity Mining Workflow

Every liquidity mining program, regardless of protocol or chain, follows the same four-step sequence. Understanding these steps is the foundation of everything else in this guide.

Step one requires depositing two tokens of equal dollar value into the pool. If you want to provide liquidity to the ETH/USDC pool when ETH is at $3,000, you deposit 1 ETH and 3,000 USDC. The protocol will not accept unbalanced deposits, and trying to game the ratio results in failed transactions or unfavorable single-sided fills. Step two issues you an LP token, which is itself an ERC-20 asset transferable like any other token. The LP token represents your fractional ownership of the pool, and burning it returns the underlying assets plus accumulated trading fees.

Step three is what distinguishes a passive liquidity provider from a liquidity miner. You take the LP token and stake it into the protocol's rewards contract, often called a gauge on Curve and Balancer, or a MasterChef on SushiSwap and many forks. The staking contract tracks how many LP tokens you have deposited and for how long, and emits the protocol's governance token to you continuously, block by block. Step four is harvesting. You claim accumulated rewards on whatever schedule fits your gas budget and tax strategy, then either compound them back into the pool or sell them for stablecoins.

Liquidity Mining vs Staking vs Yield Farming

These three terms get used interchangeably across crypto media, but they refer to genuinely different activities with different risk profiles. Clarifying the distinction is essential before you commit capital.

Asset: One token

Risk: Slashing, validator downtime

Yield source: Protocol inflation + tx fees

Typical APR: 3% to 8%

Asset: Two tokens in pair

Risk: IL, contract bug, reward dump

Yield source: Fees + reward token emissions

Typical APR: 5% to 40%

Asset: Multi-protocol stacking

Risk: Compound contract risk, leverage

Yield source: Loops, leverage, restaking

Typical APR: 10% to 200%+

Staking is the simplest of the three. You lock one asset, secure a network or service, and receive yield denominated in that same asset. There is no second token, no LP receipt, no farm to stake into. Examples include native ETH staking, locking SOL with a validator, or staking AAVE in the safety module. The risk is bounded by the protocol's slashing rules, which for most major chains in 2026 are well understood and capped.

Liquidity mining sits in the middle. You provide two assets, accept exposure to impermanent loss, and receive both trading fees and a governance reward token. It is more complex than staking and carries more risk, but the yields are higher and the activity directly supports the functioning of decentralized markets. Yield farming is the most aggressive of the three. Farmers chain liquidity mining positions across multiple protocols, often borrowing against their LP tokens, restaking on top of restaking, and chasing the highest possible APR regardless of token quality. Yield farming uses liquidity mining as one of its building blocks, but adds layers of leverage and protocol stacking that multiply both upside and risk.

How Reward Tokens Work

The reward token you earn from liquidity mining is not pulled out of thin air, and it is not free money. It is freshly minted supply released by the protocol according to an emissions schedule defined in the smart contract. Understanding how these tokens are designed determines whether the yield you see on screen is real or an illusion that will evaporate as soon as you try to sell.

Reward tokens almost always serve three functions: governance, revenue capture, and emissions direction. Governance rights let token holders vote on protocol parameters, fee changes, treasury spending, and new feature launches. Revenue capture, where it exists, distributes a portion of protocol fees back to token holders who lock or stake the token. Emissions direction is the most interesting design, popularized by Curve, where token holders vote on which liquidity pools receive the next round of token emissions, creating a competitive market for governance influence.

The emissions schedule is the most important number to check before mining a new pool. Some protocols emit on a fixed linear schedule, releasing the same amount of tokens every block until the supply runs out. Others use halving schedules similar to Bitcoin, where emissions drop by 50% every six months or year. The most modern designs use ve-locked emissions, where the rate of token release is determined by how much of the existing supply has been locked into the vote-escrow contract. In all cases, the question to ask is whether the APR you see today will still exist in three months, or whether emissions will have dropped 70% by then.

The Compound Summer of 2020: Birth of Liquidity Mining

The modern era of liquidity mining started on June 15, 2020, when Compound Finance launched its COMP governance token and began distributing it to users who borrowed and lent assets on the platform. Within a single week, Compound's total value locked exploded from roughly $90 million to over $600 million. Users discovered that by simultaneously borrowing and supplying the same asset they could earn more in COMP rewards than they paid in interest, a trick that became known as recursive lending or yield looping. The COMP token itself rocketed from around $60 at launch to over $370 within two weeks.

What Compound demonstrated was profound. A protocol could bootstrap its user base, its liquidity, and its governance distribution all at once by issuing a token to active participants. Within months, every major DeFi project copied the playbook. Balancer launched BAL distribution to liquidity providers. Curve launched CRV with its now-famous vote-escrow model. SushiSwap launched a vampire attack on Uniswap by offering SUSHI rewards to anyone who migrated their LP tokens, briefly draining over $1 billion in liquidity from Uniswap in a single weekend.

The summer of 2020 also revealed the dark side of liquidity mining. Hundreds of forks emerged with names like YAM, KIMCHI, SUSHI, and dozens of food-themed tokens promising 1,000%+ APRs. Most of these collapsed within days as reward token prices crashed under the weight of constant farmer-driven sell pressure. The lessons from that period still apply in 2026: high APR is not the same as high return, and reward token quality matters more than reward token quantity.

Top Liquidity Mining Protocols in 2026

The landscape has consolidated meaningfully since the 2020 to 2022 explosion. Most of the dozens of food-named clones from that era are gone. What remains are protocols that built real moats: deep liquidity, audited contracts, sustainable token economics, and active developer teams. These are the names that dominate liquidity mining flows today.

Uniswap V3 and V4 remain the dominant decentralized exchange by volume. Uniswap itself does not run a continuous liquidity mining program on its core pools, but the new V4 hook architecture allows third parties to deploy custom incentive contracts on top of any pool. Protocols like Arrakis, Gamma, and Steer manage concentrated liquidity positions on Uniswap V3 and V4 and distribute rewards to their depositors, effectively wrapping a liquidity mining layer around Uniswap's native fee system.

Curve Finance is the king of stable-pair liquidity mining. Curve's gauge system, combined with the veCRV vote-escrow model, created the most sophisticated emissions market in DeFi. Users lock CRV for up to four years to receive veCRV, which gives them voting power over which pools receive CRV emissions plus a boost on their own LP rewards of up to 2.5x. The Curve Wars, in which Convex, Yearn, and other protocols competed to accumulate veCRV, defined the meta-game of DeFi for years and still drives significant capital flows.

Balancer offers weighted pools where the two assets do not have to be in 50/50 ratio, and runs the veBAL system modeled on Curve's design. Balancer LPs can hold pools like 80/20 BAL/ETH, which reduces impermanent loss for the heavier asset compared to a standard 50/50 pair. Convex Finance is a meta-protocol built on top of Curve that lets users earn boosted Curve rewards without locking their own CRV. It captured roughly half of all circulating CRV at its peak and remains a major force in 2026.

Pendle took yield trading mainstream by tokenizing the yield component of yield-bearing assets and letting traders speculate on future APY levels separately from principal. Pendle pools have become a destination for yield-farming sophistication. Aerodrome on Base inherited the ve(3,3) design from Solidly and Velodrome and has become the largest liquidity venue on Base, hosting deep pools across stablecoins, ETH derivatives, and a wide selection of Base-native tokens.

Vote-Escrow (ve) Models Explained

The vote-escrow model is the most influential innovation in DeFi token design since the AMM itself. Pioneered by Curve in August 2020 and copied by dozens of protocols since, it solves the fundamental problem with first-generation liquidity mining: governance tokens were too easy to dump. The ve model forces alignment by requiring users to lock their tokens for a long period to access the most valuable features.

The basic mechanic is straightforward. You take your governance token, say CRV, and lock it in a veToken contract for a period between one week and four years. The longer you lock, the more boost you receive on three things: your share of protocol fees, your voting power in governance, and the multiplier applied to your LP mining rewards. veCRV is non-transferable, but it grants the holder real economic and political power inside the Curve ecosystem.

The ve(3,3) design popularized by Solidly, Velodrome, and Aerodrome adds a critical twist. The ve token is an NFT rather than a fungible balance, which makes positions tradeable as discrete assets. Emissions are directed by ve-token holders to specific pools through a continuous vote, and the protocol's fees from those same pools flow back to the ve-token holders who voted for them. This creates a clean alignment where ve-token holders are incentivized to vote emissions toward pools that generate real volume and real fees, not toward vanity pools with no organic activity.

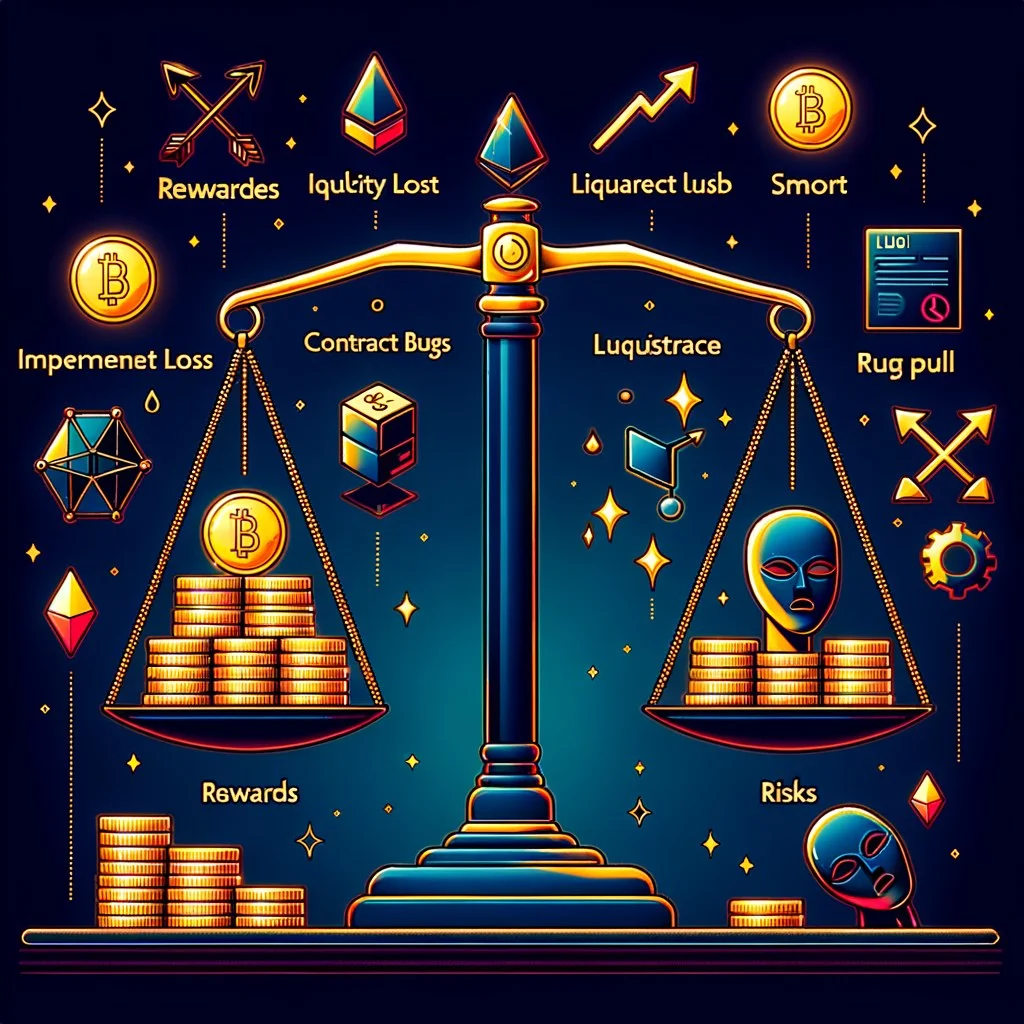

Liquidity Mining Risks

The yields look attractive, but liquidity mining is not a savings account. Four distinct risk categories can erase your gains or destroy your principal entirely. Anyone planning to deploy meaningful capital should be able to articulate each one before depositing the first dollar.

- High blended yield from fees plus rewards

- Governance token exposure on top of base yield

- No KYC, permissionless entry

- Compounding via auto-vault wrappers

- Liquidity is unlocked at any moment

- Stable-pair pools minimize price risk

- Impermanent loss in volatile pairs

- Smart contract bugs can drain pools

- Reward token dump destroys APR

- Gas costs eat small positions on L1

- Regulatory uncertainty in many jurisdictions

- Reward emissions decay over time

The most discussed risk is impermanent loss, often abbreviated as IL. When the price ratio of the two pooled assets changes, the constant-product math of the AMM rebalances your position automatically. You end up with more of the asset that fell and less of the asset that rose. If you had simply held the two tokens in your wallet, you would have come out ahead. The loss is called impermanent because if prices return to the deposit ratio it disappears, but in practice prices rarely come back exactly and the loss becomes permanent on withdrawal.

The second category is smart contract risk. Every liquidity mining position depends on at least two contracts: the AMM pool itself and the staking gauge. Each is a potential point of failure. The DeFi history book is littered with examples of bugs draining hundreds of millions in a single transaction. Auditing helps but does not eliminate risk. Even well-audited protocols like Cream Finance, Yearn, and Curve have suffered exploits.

Third is reward token dump risk. When emissions vastly exceed organic demand for the token, the price collapses. A 100% APR paid in a token that loses 90% of its value over the same period is a 90% loss, not a 100% gain. Always check whether the protocol has revenue, has fee distributions to token holders, has vote-escrow lock-ups that reduce circulating supply, and has any real reason for the token to hold value beyond farmer rotation. Finally, regulatory risk varies by jurisdiction. Some countries treat liquidity mining as a taxable event at every harvest. Others treat it as a non-taxable share class issuance. The classification can flip with new legislation.

APR vs APY in Liquidity Mining

Reading liquidity mining dashboards requires understanding the difference between APY vs APR. APR is the simple annualized rate of return, assuming you claim rewards once a year and do not reinvest them. APY includes the effect of compounding, assuming you harvest and redeposit rewards continuously. The same underlying yield can show as a 20% APR or a 22% APY depending on the compounding frequency.

For liquidity mining, the distinction matters because most rewards come as a separate token that you must manually claim, sell, swap to the underlying pair tokens, and redeposit into the pool. Each of these operations costs gas, costs slippage on the swap, and creates a taxable event in most jurisdictions. Auto-compounding vaults like Yearn, Beefy, and Convex automate this loop and let you achieve the displayed APY in practice, but they take a performance fee, typically 10% to 20% of the harvested rewards, in exchange.

The other critical APR dynamic in liquidity mining is decay as TVL grows. Reward emissions are typically fixed per block, so the per-dollar share of those emissions shrinks as more capital enters the pool. A pool launched with 100% APR and $1 million TVL will pay 10% APR once TVL hits $10 million. This is why early movers into a new mining program often capture the bulk of the returns, and why the displayed APR on a hot new pool today may be unrecognizable in a month.

Stable-Pair vs Volatile-Pair Liquidity Mining

The single most important strategic choice in liquidity mining is whether to provide liquidity to a stable pair or a volatile pair. The two categories are different products with different return profiles and different risks.

Stable pairs combine two assets that are designed to trade close to the same price. Examples include USDC/USDT, DAI/USDC, FRAX/USDC, and triple-stable pools like Curve's 3pool. Because the price ratio of the underlying assets barely moves, impermanent loss is essentially zero. The trade-off is that trading volume is also lower because arbitrageurs only have a few basis points of price differential to capture. Fees on stable pools are typically 0.04% to 0.1%, much lower than the 0.3% standard on volatile pools. Stable-pair liquidity mining is the equivalent of a conservative bond fund: 2% to 8% APR, very low risk, very predictable.

Volatile pairs combine two assets whose prices move independently. Examples include ETH/USDC, BTC/ETH, and any token paired against a stablecoin or ETH. These pools generate the bulk of decentralized exchange trading volume and pay the highest fees, typically 0.3% to 1% per trade. The catch is that impermanent loss can be severe. A pool where one asset doubles while the other stays flat will impose roughly 5.7% impermanent loss on the LP. If you are providing liquidity to a small-cap token that pumps 10x and then dumps, the math is brutal.

How to Calculate Profitability: A Worked Example

Numbers matter more than narrative. Let us walk through a concrete liquidity mining calculation using a realistic ETH/USDC position in 2026.

The headline yield in this example is 34% (22% from fees plus 12% from emissions). After realistic deductions for impermanent loss, gas, and the cost of converting reward tokens back to capital, the net falls to roughly 25%. That is still a strong return, but it shows why looking only at the displayed APR is misleading. A pool advertising 50% APR with 30% expected IL plus 5% reward token decay over the harvest period is a worse position than a stable pool offering 12% with no IL.

Different pools require different deduction estimates. Stable-pair pools deduct almost no IL but tend to have lower fee yields. Concentrated liquidity positions on Uniswap V3 and V4 can amplify both fee yields and IL by 5x to 50x depending on the range width. LP economics requires running these numbers honestly before each deposit, not just trusting the dashboard headline.

Liquidity Mining Best Practices

The patterns separating consistent earners from drained accounts in liquidity mining have been refined over six years of practice. The following rules sound simple but are violated constantly by users chasing the highest APR.

Start small. The first time you deposit into a new pool, use an amount you can afford to lose entirely. Verify that staking, harvesting, and withdrawing all work as expected. Confirm that the rewards you accumulate match the displayed APR. Then scale up. Many users make the mistake of trusting a screenshot from Twitter and depositing six figures into a contract they have never used.

Prefer audited and battle-tested protocols. The difference in risk between a Curve or Uniswap pool and an unaudited fork is enormous. Many forks copy the contract code but skip the audit, and copy-pasted vulnerabilities have drained hundreds of millions in aggregate. A pool offering 40% APR on a protocol with 90 days of history and no audit is offering compensation for a risk you cannot model.

Monitor reward decay actively. The APR you joined at is rarely the APR you exit at. Check your positions weekly. If emissions are halving or new TVL has flooded in and cut your share of rewards, recompute whether the position still beats your alternatives. Auto-compound vaults often hide this decay because they keep restaking, but the underlying math is the same.

Exit on red flags. Real red flags include the protocol's team going silent, governance proposals to drastically increase emissions, security disclosures of any kind, large unlock events for the team or investors that have not been transparent, and oracle issues. The cost of an early exit is one round of gas. The cost of staying through an exploit is everything.

Taxation of Liquidity Mining

Tax treatment of liquidity mining varies dramatically by jurisdiction, and even within jurisdictions the rules are evolving. This section is informational, not legal advice. Anyone with material liquidity mining income should consult a tax professional familiar with crypto in their country.

In the United States, the IRS has historically treated newly minted reward tokens as ordinary income at the moment they are claimable, valued at the fair market price at that moment. Subsequent appreciation or depreciation creates capital gains or losses when the tokens are sold. Depositing into and withdrawing from a liquidity pool may or may not be a taxable event depending on whether the LP token is treated as a separate property. The IRS has not issued definitive guidance on the LP token question as of 2026, and conservative practitioners treat the deposit as a disposal of both underlying assets for tax purposes.

Other jurisdictions differ. Germany has historically treated liquidity mining held for more than 10 years as tax-free under certain conditions. The United Kingdom treats LP token issuance as a disposal for capital gains purposes, similar to the conservative US approach. Portugal, long considered crypto-friendly, has tightened rules in recent years. Australia treats every claim as ordinary income. Regardless of jurisdiction, keep detailed records of every deposit, every harvest, and every withdrawal, including USD value at the time of each event. The audit trail matters far more than the tax category.

Frequently Asked Questions

Is liquidity mining the same as yield farming?

No, but they are closely related. Liquidity mining is a specific activity: deposit two tokens, receive an LP token, stake it for rewards. Yield farming is a broader strategy that can include liquidity mining as one component, but typically adds layers of leverage, borrowing, multi-protocol stacking, and recursive looping on top of base liquidity mining positions. All yield farming uses liquidity mining as a building block, but not all liquidity mining qualifies as yield farming. Liquidity mining is usually lower risk and lower yield than full yield farming.

What is impermanent loss in liquidity mining?

Impermanent loss is the difference between holding two tokens in your wallet versus depositing them into a liquidity pool. When prices diverge, the AMM rebalances your position, leaving you with more of the underperforming asset and less of the outperforming one. The loss only materializes if you withdraw at the divergent prices. If prices return to the deposit ratio, it disappears. For volatile pairs, IL can range from 1% to 25%+ depending on price movement. For stable pairs, it is typically under 0.1%.

Which is the best liquidity mining protocol in 2026?

There is no single best, only best-fit for a strategy. For deep stable liquidity, Curve and its meta-layer Convex remain the standard. For concentrated liquidity in volatile pairs with active management, Uniswap V3 and V4 wrappers like Arrakis and Gamma lead. For Base chain native liquidity, Aerodrome dominates. For yield trading and APY speculation, Pendle is the venue. For weighted pools and 80/20 designs that minimize IL, Balancer remains differentiated. Most experienced LPs spread positions across two or three of these depending on their target asset exposure.

Can I lose money in liquidity mining?

Yes, in several ways. Impermanent loss on volatile pairs can outweigh fee and reward income. Smart contract bugs can drain entire pools. Reward token prices can collapse, turning a headline 50% APR into a real-world negative return. Regulatory action can lock or invalidate positions. Gas costs on Ethereum mainnet can exceed rewards on small positions. Liquidity mining is not equivalent to a bank deposit, and treating it as such has cost many users their principal.

What is ve(3,3)?

The ve(3,3) model combines vote-escrow tokenomics from Curve with the (3,3) game theory popularized by OlympusDAO. The "ve" part means users lock the protocol token in exchange for non-transferable governance and reward power. The "(3,3)" part refers to a Nash equilibrium where every participant benefits most when everyone cooperates by locking rather than selling. In practice, ve(3,3) protocols like Aerodrome and Velodrome let ve-token holders direct emissions to specific pools and capture the fees those pools generate, creating tight alignment between liquidity allocation and protocol revenue.

How much money do I need to start liquidity mining?

On a low-gas chain like Base, Arbitrum, or Polygon, you can meaningfully participate with $500 to $1,000 in capital. On Ethereum mainnet, the math only starts working at $5,000 to $10,000 minimum because gas costs for deposit, stake, claim, and withdraw can total $50 to $200 per round trip depending on network congestion. Stable-pair pools on L2s have become accessible to mid-four-figure positions, while volatile-pair concentrated liquidity on mainnet still favors larger capital that can absorb gas and active range management.

Conclusion

Liquidity mining built modern DeFi. The mechanism that lets a protocol bootstrap deep order books, distribute governance to engaged users, and turn passive token holders into active market makers is the foundation that every on-chain trading venue depends on. Understanding how it works puts you in a position to participate in that ecosystem rather than just consume it.

The honest summary is that liquidity mining sits in the middle of the DeFi risk spectrum. It is more complex and more dangerous than staking, less aggressive and less leveraged than full yield farming. The yields on offer in 2026 are lower than the absurd numbers of 2020 to 2021 but they are also more sustainable, supported by real fee income from real trading volume rather than pure token inflation. A well-chosen stable-pair position on Curve or a thoughtfully managed concentrated position on Uniswap V4 can generate 8% to 30% net APR in conditions where bank deposits pay 4% and treasuries pay 4.5%.

The best advice for any new participant is to start small, choose audited protocols with sustainable token economics, understand impermanent loss before deploying volatile-pair capital, and recompute net profitability rather than trusting headline APR. Liquidity mining rewards patience and discipline. It punishes chasing the highest number on the leaderboard. The miners who are still here after six years did not pick the highest APR, they picked the most sustainable risk-adjusted yield and let compounding do the work.

Frequently Asked Questions

What is liquidity mining?

Liquidity mining is a process where users provide cryptocurrency assets to decentralized finance (DeFi) protocols and are rewarded with additional tokens, often the protocol's native governance token.

How does liquidity mining work?

Participants deposit their crypto into liquidity pools, facilitating trading or lending within the DeFi platform. In return for providing this liquidity, they earn a share of transaction fees and newly minted tokens.

What are the rewards in liquidity mining?

Rewards typically include a portion of the trading fees generated by the liquidity pool and newly issued governance tokens from the DeFi protocol. These tokens can often be traded or used for voting on protocol changes.

What is the role of DeFi in liquidity mining?

DeFi protocols are the platforms where liquidity mining occurs, enabling peer-to-peer financial services without traditional intermediaries. Users interact with smart contracts on these decentralized applications to provide liquidity and earn rewards.

What are the potential future trends for liquidity mining by 2026?

By 2026, liquidity mining may see increased institutional adoption, enhanced regulatory clarity, and a focus on more sustainable tokenomics models. Innovations in yield optimization and risk management tools are also anticipated.

Related Guides

- Liquidity Incentive Traps: When Rewards Attract Farmers, Not Real Buyers

- How to Farm on PancakeSwap: Liquidity, CAKE Rewards and LP Risks (2026)

- Impermanent Loss in DeFi Liquidity Pools: Worked LP Math, Break-Even and Trade-Offs (2026)

- Liquidity Turnover vs TVL: How to Know If a DeFi Pool Is Active or Idle

- LP Behavior: Insights from Liquidity Providers