What Is Frax Finance: Complete FXS & FRAX Stablecoin Guide (2026)

— By Whatsertrade in Tutorials

Frax Finance is a multi-product DeFi ecosystem: FRAX stablecoin, frxETH liquid staking, Fraxlend, FraxSwap and Fraxtal L2. Full 2026 guide with FXS and veFXS.

Frax Finance is not a single product. It is a sprawling, vertically integrated DeFi ecosystem that bundles a stablecoin, a liquid staking token, an isolated lending market, a time-weighted AMM, a cross-chain bridge, and its own Layer 2 rollup. If you have heard of FRAX the dollar-pegged stablecoin without realizing it is the centerpiece of an entire onchain economy, you are not alone. Most articles about Frax stop at the stablecoin and miss the bigger picture.

Founded in 2020 by Sam Kazemian, Stephen Moore, and Travis Moore, Frax pioneered the fractional-algorithmic stablecoin model, then publicly reversed course in 2023 to become fully collateralized through governance vote FXIP-188 (commonly called the FXG vote). It launched its own OP Stack rollup called Fraxtal in February 2024, introduced an FXTL points program that runs through 2026, and continues to ship new primitives like frxBTC, frxUSD, and AMO controllers that manage protocol liquidity at scale.

This guide is a complete walkthrough of the Frax stack as it stands in May 2026. You will learn how each product works, how the FXS governance token captures value, how to mint FRAX, stake frxETH, lend on Fraxlend, and bridge to Fraxtal. You will also see how Frax compares to MakerDAO/Sky, Curve, and Base, the risks that come with each subsystem, and the eight to ten questions that beginners ask most often.

What Is Frax Finance?

Frax Finance is a multi-product DeFi protocol that issues the FRAX stablecoin, the frxETH liquid staking token, runs the Fraxlend isolated lending platform, operates the FraxSwap AMM with built-in TWAP order execution, bridges assets via FraxFerry, and powers the Fraxtal Layer 2 rollup. The FXS token governs the entire ecosystem and captures fees from every subprotocol.

That single paragraph is dense for a reason. Frax is intentionally designed as a stack rather than a single dApp. The protocol calls itself a "decentralized central bank" because it issues currency (FRAX), manages monetary policy through AMO controllers, operates payment rails (Fraxtal, FraxFerry), and earns seigniorage on the assets it controls. Every product feeds back into the same flywheel: FRAX liquidity grows, AMOs deploy that liquidity into yield strategies, fees flow to veFXS lockers, FXS becomes more valuable, governance can mint more collateral-backed FRAX. The loop is the point.

Founders and the Path from Fractional to Fully Collateralized

Frax Finance was founded by Sam Kazemian (co-founder of Everipedia), Stephen Moore, and Travis Moore. Sam is the public face of the protocol. Travis handles much of the technical engineering and operations. The protocol launched on December 20, 2020 with a then-novel pitch: a stablecoin only partially backed by collateral, with the rest supported by algorithmic mechanisms and arbitrage. At launch, FRAX was 100% collateralized by USDC, and the system was designed to gradually reduce the collateral ratio (CR) as the market demonstrated confidence. By 2022, the CR had fallen as low as 82%, with the uncollateralized portion supported by FXS that the protocol could mint and sell if needed.

This fractional-algorithmic model survived the brutal stress test of May 2022 when Terra/UST collapsed. FRAX held its peg partly because it had real collateral behind most of every coin, and partly because Frax controlled enough Curve liquidity through its AMOs to absorb sell pressure. In February 2023, Sam Kazemian put forward proposal FXIP-188, commonly nicknamed the "FXG vote" because it set FRAX on a path toward becoming fully collateralized at 100% CR. The proposal passed with overwhelming support from veFXS lockers, and over the following months the protocol steadily raised the collateral ratio until FRAX reached full backing. The era of partially-backed algorithmic FRAX officially ended.

The shift was not just defensive. Fully collateralized FRAX is more credible to institutional users and integrators, and it removes a major narrative risk after regulators turned hostile toward algorithmic stablecoins. The cost is that Frax must hold more stablecoin reserves. The protocol earns this back through AMO yields on those reserves.

FRAX: The Stablecoin Centerpiece

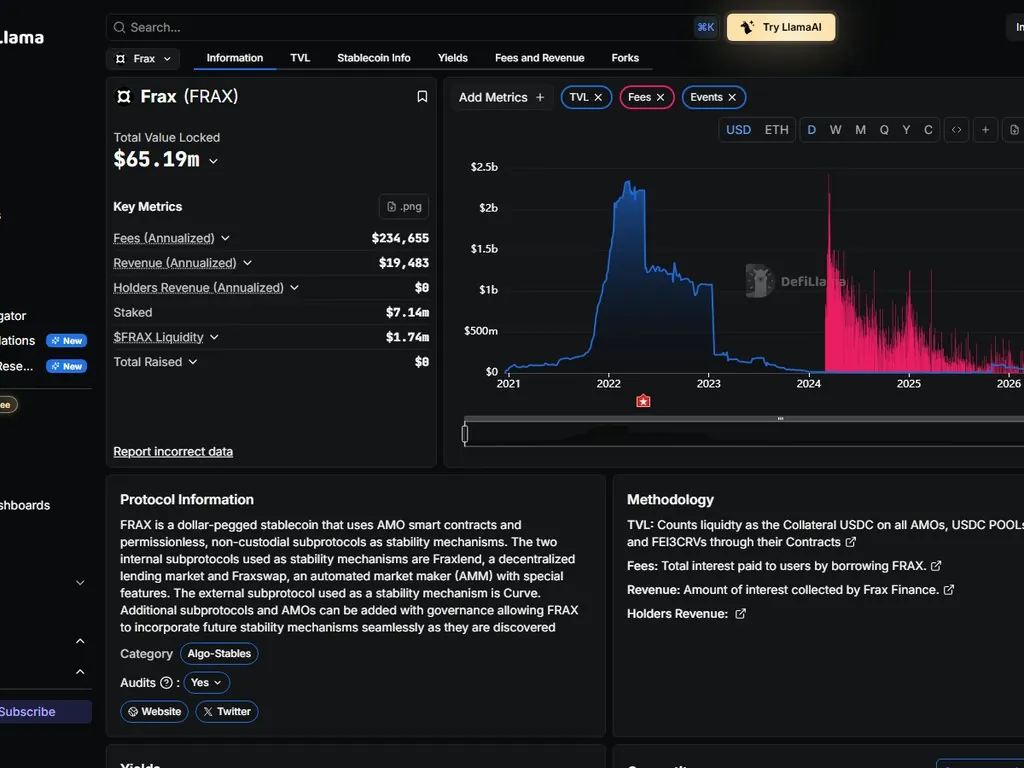

FRAX is the dollar-pegged stablecoin at the center of the protocol. After the FXG vote completed, every FRAX in circulation became backed by an equivalent or greater amount of stable assets held by the protocol, including USDC, USDT, tokenized treasuries, and DAI, all managed through smart contracts called AMOs.

Minting FRAX is permissionless. Anyone can deposit accepted collateral into the Frax minting contract and receive FRAX one-to-one. Redemption works the same way in reverse. This open mint-and-burn mechanism enforces the peg. When FRAX trades meaningfully above $1, arbitrageurs mint new FRAX and sell it for profit, increasing supply and pushing the price down. When it trades below $1, arbitrageurs buy FRAX cheap and redeem it for $1 of collateral, reducing supply and pushing the price up. FRAX is deployed natively on Ethereum, Fraxtal, and several other chains, with FraxFerry providing canonical cross-chain liquidity. While Circle pockets the Treasury bill yield on USDC reserves, Frax uses AMO controllers to deploy FRAX collateral into yield-bearing strategies and distributes the proceeds to veFXS lockers.

frxETH and sfrxETH: Liquid Staking Without Slashing

frxETH is Frax's liquid staking token. You deposit ETH into the frxETH minter, the protocol stakes that ETH through its own validator set on the Ethereum beacon chain, and you receive frxETH in return at a one-to-one ratio. frxETH itself does not accrue staking yield directly. It just represents a claim on staked ETH, similar to Rocket Pool's rETH but with a different yield distribution model.

To earn yield, you stake frxETH into the sfrxETH vault. sfrxETH is the yield-bearing version. As validators earn staking rewards, the exchange rate between sfrxETH and frxETH gradually increases, similar to how aTokens or cTokens accrue interest. The reason for splitting the token into two pieces is that it lets frxETH function as a clean, fungible representation of staked ETH for use in liquidity pools, while sfrxETH captures the yield for stakers who want it.

One of the most distinctive design choices in frxETH is its slashing resistance. Frax operates its own validator infrastructure with rigorous monitoring, geographic distribution, and conservative client diversity. Since launch, the frxETH validator set has experienced zero slashing events. This is partly engineering and partly statistical luck, but the operational practices behind it are deliberate. Compare this to early Lido validator slashings or Rocket Pool's penalty events, and you can see why frxETH has carved out a niche among yield-focused stakers.

FXS: Governance and Value Capture Token

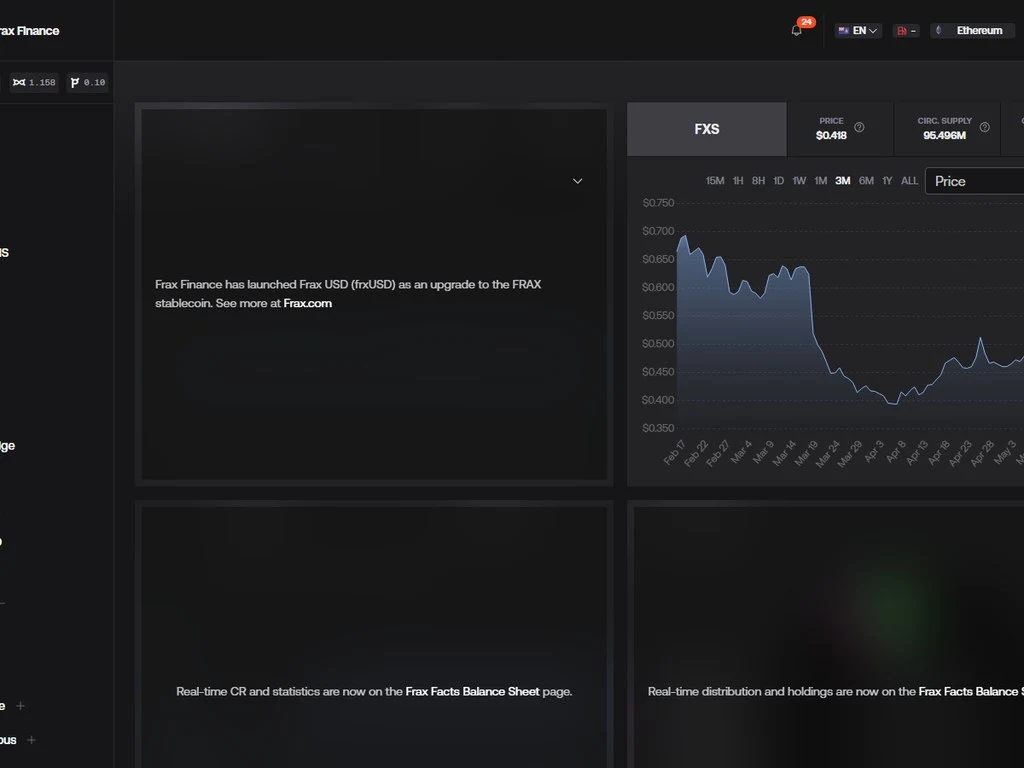

FXS (Frax Shares) is the governance token of the protocol, with a fixed maximum supply of 100 million tokens and emissions that decrease over time. Approximately 60% of the supply is allocated to community incentives, liquidity rewards, and gauge emissions. The remaining 40% covers team allocation, treasury, and early investors, with multi-year vesting schedules.

To participate in governance and earn protocol fees, holders must lock FXS into veFXS (vote-escrowed FXS) for a duration ranging from one week to four years. The longer you lock, the more veFXS you receive per FXS: a four-year lock gives four veFXS per FXS, a one-year lock gives only one. veFXS decays linearly, so to maintain voting power you must re-lock periodically. veFXS holders receive a share of all fees generated across the Frax ecosystem, including minting and redemption fees on FRAX, lending interest from Fraxlend, swap fees from FraxSwap, AMO yields, and sequencer revenue from Fraxtal. The model is inspired by Curve's veCRV system: long-term lockers receive a larger share of value capture, aligning governance with protocol health.

Fraxlend: Isolated Pair-Based Lending

Fraxlend is Frax's lending platform, and it takes a different approach from monolithic markets like Aave or Compound. Rather than pooling all assets into a single risk-shared market, Fraxlend creates isolated lending pairs. Each pair consists of one asset that can be borrowed and one asset that serves as collateral. A pool might allow borrowing FRAX against ETH, for example, while a separate pool allows borrowing FRAX against wstETH.

The advantage of isolation is risk containment. In a pooled market like Aave, a serious bad debt event in one asset can theoretically threaten the entire protocol. In Fraxlend, each pair is its own siloed market with its own oracle, its own liquidation parameters, and its own utilization curve. If one pair experiences bad debt, only the lenders in that specific pair are exposed. The rest of the protocol is unaffected.

Interest rates on Fraxlend are dynamic and adjust based on utilization. The protocol uses a variable rate algorithm that increases borrow rates when utilization is high and decreases them when utilization is low. The goal is to keep utilization within a target band, typically between 70% and 85%, where capital is being used efficiently without preventing lenders from withdrawing. Liquidations occur when the loan-to-value ratio exceeds the maximum LTV defined for that pair, and liquidators receive a discount on the collateral they claim as compensation for the work.

FraxSwap: TWAMM and Native TWAP Execution

FraxSwap is the AMM built directly into the Frax protocol. From the outside it looks similar to Uniswap V2 with constant-product pools and 0.3% swap fees. The killer feature, however, is the TWAMM mechanism (Time-Weighted Average Market Maker), which lets users execute very large orders gradually over time without the slippage that would come from dumping the entire order at once.

Here is how TWAMM works in practice. Say you want to sell 1,000 ETH for FRAX over the course of a week. Instead of dumping it all at once and absorbing massive slippage, you submit a TWAMM order that instructs the pool to sell your ETH at a steady rate every block over the next seven days. Other traders and arbitrageurs interact normally with the pool, and your sells are folded into the pool's price-discovery process continuously rather than as a single shock. The result is that you achieve something close to the time-weighted average price (TWAP) over that period.

This makes FraxSwap particularly attractive for DAOs and large holders who need to enter or exit positions without moving the market. It is also useful for protocol treasury operations and for DAOs that need to diversify their holdings over time. The contrast with traditional limit orders or aggregator routing is meaningful: TWAMM is a native AMM primitive, not a layer built on top of taker-maker matching.

FraxFerry: The Frax-Native Bridge

FraxFerry is the protocol's cross-chain bridge for moving Frax assets between supported chains. It was built in-house rather than relying on third-party bridges after several high-profile bridge hacks in 2022 and 2023 demonstrated that external bridges introduce significant trust assumptions. By controlling its own bridge, Frax can guarantee that the canonical version of FRAX, frxETH, and other Frax assets remain consistent across chains.

FraxFerry uses a system of trusted captains who batch-process bridge transactions periodically rather than executing them instantly. The delay (typically a few hours) is a deliberate security tradeoff. It allows the protocol to monitor for suspicious activity and intervene if necessary, at the cost of slower bridging compared to instant solutions. For most users this is a non-issue. For traders who need instant cross-chain movement, third-party bridges or aggregators are still an option.

The bridge supports all major Frax assets including FRAX, FXS, frxETH, sfrxETH, and (more recently) frxBTC and frxUSD. Supported destinations include Ethereum, Fraxtal, Arbitrum, Optimism, Polygon, BNB Chain, and Avalanche, with new chains added periodically based on community demand and integration partnerships.

Fraxtal: The OP Stack Rollup Launched February 2024

Fraxtal is Frax's own Layer 2 rollup, launched on February 7, 2024. It is built on the OP Stack, the same modular framework used by Optimism, Base, and Mode. Fraxtal is technically an Ethereum L2, meaning transactions are settled to Ethereum mainnet for security, but execution and state are managed on the Fraxtal chain itself. Gas fees on Fraxtal are paid in frxETH rather than ETH, which creates direct demand for the Frax liquid staking token.

What makes Fraxtal distinctive among OP Stack chains is the FXTL points program. From launch through 2026, users earn FXTL points for activity on Fraxtal: providing liquidity, lending and borrowing, holding Frax assets, deploying protocols, and using Fraxtal-native applications. FXTL points were initially positioned as a precursor to future token distributions, with rewards expected to materialize as airdrops or as conversions into protocol tokens once specific Fraxtal-native projects launch.

The economic logic behind FXTL is to bootstrap the ecosystem. Rather than paying upfront with hard token emissions (which dilutes supply and creates immediate sell pressure), Frax issues programmable points that convert into rewards later, when the ecosystem can absorb them more gracefully. The model is similar to what we have seen with Blur points, Friend.tech points, EigenLayer points, and other point-based incentive programs that became dominant in 2023 and 2024.

Fully-collateralized USD stablecoin issued by Frax. Mintable and redeemable 1:1 with permissionless arbitrage.

Liquid staking pair. frxETH is the LST, sfrxETH is the yield-bearing vault with zero slashing events to date.

Governance token with 100M max supply. Lock FXS up to 4 years for veFXS, voting power, and fee distribution.

OP Stack rollup launched Feb 2024. Gas paid in frxETH, FXTL points incentivize early ecosystem activity.

frxBTC and frxUSD: The Latest Evolution

In 2025 Frax expanded its asset suite with frxBTC and frxUSD, both designed to extend the protocol's reach into new collateral types and use cases. frxBTC is a wrapped representation of Bitcoin held in a verifiable custody arrangement and minted as an ERC-20 on Ethereum and Fraxtal. It is conceptually similar to WBTC or tBTC but with Frax-native custody and integration into Fraxlend and FraxSwap from day one.

frxUSD is the next-generation evolution of FRAX itself. While FRAX remains the legacy stablecoin and is still widely used, frxUSD introduces a fully-on-chain treasury-backed model where the underlying collateral is composed primarily of tokenized US Treasury bills via partnerships with tokenized treasury issuers like Ondo, Maple, and Mountain Protocol. The yield from those treasuries flows back through AMO controllers, partly to veFXS lockers and partly to frxUSD holders themselves via a savings vault similar to sFRAX. This pushes Frax further into the real-world asset narrative that has dominated DeFi conversations through 2024-2026.

The relationship between FRAX, frxUSD, and the broader stablecoin landscape is evolving. Frax governance has signaled that frxUSD will gradually become the flagship issuance, with FRAX persisting as a legacy product for users and integrations that prefer stability of name. The migration is voluntary, gradual, and governance-controlled.

AMO Controllers: The Hidden Engine

AMOs (Algorithmic Market Operations) are the secret sauce of Frax's economic model. An AMO is a smart contract that has the authority to mint, burn, or move FRAX (and other protocol assets) within constraints set by governance. The purpose of AMOs is to deploy idle protocol capital into yield-bearing strategies, manage liquidity across DEXs, and protect the FRAX peg through automated market operations.

The Curve AMO, for example, deploys FRAX and USDC into the FRAX/USDC Curve pool, which is one of the deepest stablecoin pools in DeFi. This earns trading fees and CRV emissions, which are then converted into protocol revenue. The Convex AMO deposits the Curve LP tokens into Convex Finance to capture additional CVX rewards. The Fraxlend AMO mints FRAX directly into Fraxlend pools to provide liquidity for borrowers, effectively creating a free supply of FRAX that can be borrowed against productive collateral. Every borrowed FRAX must be repaid, so the AMO behaves like a leveraged central-bank balance sheet that always closes.

The brilliance of the AMO design is that protocol revenue scales with the size of the FRAX supply rather than being capped by initial treasury size. As more FRAX is minted, more capital flows through the AMOs, more yield is generated, and more value accrues to veFXS holders. It is genuinely one of the most sophisticated treasury-management designs in DeFi, and it is a major reason why Frax has consistently been profitable while most other protocols subsidize emissions with their token.

How to Mint FRAX Step by Step

Minting FRAX is straightforward. The following steps assume you have a self-custody wallet like MetaMask or Rabby, with ETH for gas and an accepted collateral asset like USDC.

Step 1: Navigate to frax.finance and connect your wallet. Always verify the URL carefully to avoid phishing sites, and consider using a burner wallet if you are testing the protocol for the first time. Frax governance addresses are publicly verifiable through the protocol's documentation.

Step 2: Open the FRAX mint module. Select USDC as your input asset and FRAX as your output. The interface displays the current minting fee (typically zero or near-zero under normal market conditions) and the redemption fee. The system uses a price oracle from decentralized oracle networks to validate the FRAX peg before allowing mints.

Step 3: Approve USDC. Your wallet will request a token approval transaction so that the Frax mint contract can pull USDC from your wallet. Set the approval to the exact amount you plan to mint rather than unlimited, following safe permission practices. Confirm the approval and wait for it to mine.

Step 4: Execute the mint. Click the mint button, confirm the transaction in your wallet, and wait for the block to be included. You will receive FRAX one-to-one with the USDC you deposited. You can verify the transaction on Etherscan or your preferred block explorer.

Step 5: Use your FRAX however you want. You can hold it as a stable asset, deposit it into sFRAX or sfrxUSD for yield, supply it to Fraxlend as a lender, provide liquidity on FraxSwap or Curve, or bridge it to Fraxtal via FraxFerry. The redemption process reverses these steps: deposit FRAX, receive USDC.

How to Stake frxETH for Yield

Staking frxETH into sfrxETH is the cleanest way to capture Ethereum staking yield through the Frax ecosystem. The process takes two transactions and about a minute.

Step 1: Acquire frxETH. You can buy frxETH directly on Curve, Uniswap, or FraxSwap, or mint it 1:1 by depositing ETH into the frxETH minter on the Frax app. Minting is gas-efficient and gives you exact one-to-one conversion. Buying on the open market is faster but may incur small slippage if the pool is shallow at that moment.

Step 2: Stake frxETH into sfrxETH. Navigate to the sfrxETH vault, approve frxETH for the vault contract, and deposit. You will receive sfrxETH at the current exchange rate (which starts at 1:1 and gradually rises over time as staking rewards accrue). Your sfrxETH does not change in balance, but the underlying frxETH it represents grows.

Step 3: Monitor yield. sfrxETH typically earns between 3% and 5% APR on staked ETH, with the exact figure depending on Ethereum network conditions, validator efficiency, and the share of MEV captured. You can track the exchange rate trend on the Frax dashboard or by querying the sfrxETH contract directly.

Step 4: Unstake when ready. To unstake, redeem sfrxETH for frxETH through the vault. You can then either hold frxETH, sell it on a DEX, or wait for ETH redemption windows to swap frxETH back to ETH at one-to-one ratio. The exact unstaking timing depends on Ethereum validator queue conditions, which can occasionally lengthen during periods of high withdrawal demand.

How to Lend on Fraxlend

Fraxlend operates on isolated pair markets, so the first step is selecting which pair you want to lend into. Each pair has its own risk profile, interest rate curve, and liquidity. Higher-volatility collateral pairs typically offer higher lending APYs because the borrow demand and risk premium are larger.

Step 1: Choose a pair. Browse the Fraxlend interface and review the available pairs. Common pairs include FRAX/wstETH, FRAX/WBTC, FRAX/CRV, and FRAX/sfrxETH. Each pair displays its current utilization, supply APY, borrow APY, and total assets. Higher utilization means higher rates but slightly higher withdrawal risk.

Step 2: Approve and deposit. Approve the asset you want to lend (typically FRAX) and deposit it into the chosen pair. You receive a deposit receipt token representing your share of the pool, similar to aTokens on Aave or fTokens on Compound forks.

Step 3: Track your position. Your deposit accrues interest continuously as borrowers pay variable-rate fees into the pool. You can withdraw at any time as long as utilization permits (the pool needs enough non-utilized capital to fulfill your withdrawal). If utilization is at 100%, you must wait for borrowers to repay or for new lenders to enter before withdrawing.

Step 4: Understand the risks. Each isolated pair carries its own risk. If the collateral asset depegs or crashes faster than liquidators can act, the pair can develop bad debt. Because pairs are isolated, this bad debt does not threaten other pairs or the broader Frax protocol, but it does affect lenders in that specific pair. Diversify across multiple pairs if you want to spread this risk.

Frax vs MakerDAO/Sky: A Direct Comparison

Frax and MakerDAO (now rebranded as Sky) are the two most prominent stablecoin protocols not run by a centralized issuer. They take genuinely different approaches that reflect different design philosophies.

The simplest way to summarize the difference is that Sky behaves more like a traditional debt-issuance protocol where users open vaults and pay stability fees, while Frax behaves more like a treasury-and-AMO model where the protocol mints stablecoin against 1:1 collateral and earns yield on that collateral through automated strategies. Both models work. They produce different risk profiles, fee structures, and integrations.

Frax vs Curve: Allies, Not Competitors

Frax and Curve are sometimes confused as competitors because both deal with stablecoins, but they are functionally complementary. Curve is the dominant DEX for stablecoin swaps and provides the deepest liquidity pools for FRAX, USDC, USDT, DAI, and others. Frax issues FRAX and uses Curve as one of its primary venues for liquidity. The FRAX/USDC Curve pool is one of the largest stablecoin pools by TVL and serves as a critical peg-stability mechanism.

Frax also famously played a starring role in the so-called "Curve Wars" of 2022 by acquiring large amounts of CRV and CVX to direct emissions toward FRAX-paired pools. Frax's veFXS model is itself directly inspired by Curve's veCRV mechanism. The two protocols have historically been deeply intertwined and continue to be in 2026.

Fraxtal vs Base: L2 Strategy Comparison

Base is Coinbase's OP Stack rollup, launched in August 2023 and now one of the largest L2s by TVL and daily active addresses. Fraxtal launched six months later with a different positioning. Where Base aimed for mass-market accessibility and integration with Coinbase's onramp, Fraxtal positioned itself as a DeFi-native chain where the underlying asset for gas is itself a yield-bearing token (frxETH).

The FXTL points program differentiates Fraxtal economically. Base does not run a native points program. Coinbase's incentive structure focuses on consumer adoption via Coinbase Wallet integrations. Fraxtal's incentives are aimed at DeFi protocols, liquidity providers, and power users who care about composable rewards. Neither approach is strictly better. They serve different audiences and different growth strategies.

Total TVL on Fraxtal sat at roughly $400 to $600 million through early 2026, smaller than Base ($5B+) but meaningful for a more specialized chain. Fraxtal also benefits from native frxETH liquidity and from being the canonical home for protocol upgrades like frxUSD.

FXS Tokenomics in Detail

FXS has a maximum supply of 100 million tokens. The emission schedule reduces issuance over time. Initial allocations were divided roughly as follows: 60% to community programs (liquidity mining, gauge emissions, treasury), 20% to team and advisors with multi-year vesting, 12% to early investors with vesting, 5% to the foundation, and 3% to strategic allocations. These exact percentages have been adjusted over time through governance.

The vesting schedule for team and investor tokens is staggered over multiple years specifically to avoid unlock cliffs that could destabilize the market. Most early team and investor unlocks completed by 2024-2025, meaning the current FXS supply is largely "liquid" in a market-structure sense. New emissions come almost entirely from gauge rewards distributed to liquidity pools selected by veFXS voters.

veFXS distribution is concentrated among a relatively small number of large holders, many of whom are protocol-aligned entities like Convex, Yearn, and various DAO treasuries. This concentration is similar to veCRV and reflects the long-time-horizon incentives baked into the model. Smaller holders can still participate by either locking directly or by delegating to liquid wrappers like cvxFXS through Convex.

Risks and Tradeoffs

No DeFi protocol is risk-free, and Frax is no exception. The following risks are worth understanding before committing significant capital.

Smart contract risk. Frax has dozens of interrelated contracts spanning FRAX, frxETH, Fraxlend, FraxSwap, FraxFerry, AMOs, and Fraxtal. The protocol has been audited multiple times by reputable firms and has a strong security track record, but the sheer complexity of the system means that bugs are always possible. Composability also means that a bug in one product (e.g., FraxSwap) could potentially affect connected products (e.g., AMO operations).

Depeg history. FRAX has held its peg through major market stress, including the Terra/UST collapse, the FTX bankruptcy, and the USDC depeg of March 2023. During the USDC depeg, FRAX briefly traded as low as $0.88 because so much of its collateral was USDC. This recovered within days as USDC itself recovered. Anyone using FRAX should understand that its peg is structurally dependent on the integrity of its underlying collateral, particularly USDC.

Validator concentration. frxETH validators are operated by a relatively small set of operators compared to Lido or Rocket Pool. This concentration is a deliberate design choice to ensure operational excellence and avoid slashing, but it does mean frxETH has more centralized validation than its largest competitors. The tradeoff is fewer slashing events but higher operator-level trust assumptions.

AMO complexity. AMOs are powerful but opaque to outside observers. Most users cannot easily audit which strategies are running, how much capital is deployed where, and what counterparty risks exist. Governance has visibility, but day-to-day operations require trust in the protocol's risk management.

Bridge risk on FraxFerry. While FraxFerry is operated by trusted captains and has not experienced security incidents, all bridges concentrate risk in their bridge contracts. Bridge hacks have collectively cost the industry billions of dollars. FraxFerry's deliberate delay mechanism reduces but does not eliminate this category of risk.

Regulatory uncertainty. Stablecoins remain a regulatory focus globally. While fully-collateralized stablecoins are generally treated more favorably than algorithmic ones, the rules in the US, EU (under MiCA), and other jurisdictions continue to evolve. Future regulation could affect how Frax mints, distributes, or integrates with traditional finance.

Pros and Cons

- Vertically integrated DeFi stack under one ecosystem

- Fully collateralized FRAX with permissionless mint and redeem

- frxETH has zero slashing events since launch

- veFXS captures fees from all subprotocols

- AMO model generates sustainable yield without dilution

- Fraxtal L2 plus FXTL points create native ecosystem incentives

- Complex architecture across many interacting contracts

- Heavy USDC reliance creates correlated peg risk

- Validator set for frxETH is more concentrated than competitors

- FraxFerry delay can be frustrating for time-sensitive moves

- veFXS distribution skews toward large protocol-aligned holders

- FXTL points value depends on future governance decisions

Best Practices and FXTL Points

If you decide to use Frax products, a few practical guidelines will help you avoid common pitfalls. Always interact with the official frax.finance domain or apps explicitly linked from it. Phishing sites are common, and a single approved transaction to a malicious contract can drain your wallet. Bookmark the real URL and use a hardware wallet for any meaningful balance. Manage approvals carefully: set approvals to the exact amount needed and periodically revoke unused approvals to avoid address poisoning scams. Use a burner wallet when first interacting with any new Frax product or chain.

The FXTL points program is one of the most distinctive elements of Fraxtal's growth strategy. Users earn points for bridging assets to Fraxtal, holding qualifying Frax assets, providing liquidity in approved pools, deploying smart contracts, and using partner protocols. Points are non-transferrable and accumulate per address on the Fraxtal dashboard. Governance has signaled that FXTL will eventually convert into something redeemable (Fraxtal-native token, FXS rewards, or frxETH distributions), with conversion expected during 2025-2026. Treat FXTL points as potential upside, not a guaranteed reward.

Frax also integrates with most major DeFi protocols. FRAX is accepted on Aave, Compound, and Morpho. frxETH and sfrxETH are integrated into Curve, Convex, Yearn, and Pendle. This composability is a strength because users can plug Frax assets into existing strategies, and a risk because complex interconnections widen the surface area for cascading failures. Treat Frax as one component in a stack rather than as a self-contained product, and understand which contracts you are interacting with at every step.

FAQ

Q Is FRAX still an algorithmic stablecoin?

No. FRAX was originally a fractional-algorithmic stablecoin, but after the FXG vote (FXIP-188) passed in early 2023, the collateral ratio was raised to 100%. FRAX is now fully collateralized by stable assets like USDC, USDT, and tokenized treasuries held by the protocol. The algorithmic portion of the design has been retired.

Q Who founded Frax Finance?

Frax Finance was founded in 2020 by Sam Kazemian (co-founder of Everipedia), Stephen Moore, and Travis Moore. Sam is the public face of the protocol and remains the most active spokesperson. Travis handles much of the engineering and operations.

Q What is the difference between FXS and veFXS?

FXS is the freely tradable governance token. veFXS is what you receive when you lock FXS for a period of one week up to four years. Longer locks give you more veFXS per FXS. veFXS provides voting power on governance proposals and earns a share of fees generated across the Frax ecosystem. veFXS itself is non-transferrable and decays over time.

Q How does frxETH avoid slashing?

Frax operates its own validator infrastructure with rigorous monitoring, client diversity, geographic distribution, and conservative operational practices. Since launch, the frxETH validator set has experienced zero slashing events. The tradeoff is that the validator set is more concentrated than open systems like Rocket Pool, which intentionally distributes staking to anyone who meets the bond requirements.

Q What is Fraxtal and why does it use frxETH for gas?

Fraxtal is Frax's Layer 2 rollup, built on the OP Stack and launched in February 2024. It uses frxETH as its gas token rather than ETH. This creates direct demand for frxETH and makes the asset slightly more attractive to hold for users who transact on Fraxtal. Gas paid on Fraxtal also contributes to ecosystem revenue.

Q Are FXTL points worth anything?

FXTL points are non-transferrable balances that accumulate based on activity on Fraxtal. Governance has signaled they will eventually be redeemable for tokens, rewards, or other value, with conversion expected during 2025-2026. The exact ratio has not been finalized, so points should be treated as speculative future value rather than guaranteed rewards.

Q What is the difference between FRAX and frxUSD?

FRAX is the legacy stablecoin issued by Frax since 2020. frxUSD is the newer evolution introduced in 2025, designed primarily around tokenized US Treasury bill backing and with yield distribution flowing through AMO controllers to both veFXS lockers and frxUSD holders via a savings vault. Both remain in circulation. frxUSD is positioned as the long-term flagship stablecoin.

Q What are AMO controllers?

AMOs (Algorithmic Market Operations) are smart contracts authorized by governance to mint, burn, or deploy protocol assets within defined constraints. They manage liquidity, generate yield on idle treasury capital, and help defend the FRAX peg. Examples include the Curve AMO (deploys liquidity into the FRAX/USDC pool), the Convex AMO (stacks Curve LP into Convex for additional yield), and the Fraxlend AMO (mints FRAX directly into Fraxlend pools).

Q Is Frax safe to use?

Frax has a strong security record and has been audited multiple times by reputable firms. It survived major stress events including the Terra/UST collapse, the FTX bankruptcy, and the March 2023 USDC depeg. That said, no DeFi protocol is risk-free. Smart contract risk, collateral risk (especially USDC dependence), and bridge risk through FraxFerry all exist. Use a hardware wallet, manage approvals carefully, and size positions according to your own risk tolerance.

Q How does Frax compare to MakerDAO/Sky?

Frax mints stablecoin against 1:1 collateral via permissionless mint and redeem, then earns yield on that collateral through AMO controllers. Sky (formerly MakerDAO) issues stablecoin through collateralized debt positions where borrowers post collateral and pay stability fees. Frax is more vertically integrated (its own L2, LST, AMM, lending market) while Sky has spawned subDAOs (Sky Stars) and historically focused on large real-world asset exposure. Both are major stablecoin issuers with different design philosophies.

Conclusion: Why Frax Matters in 2026

Frax Finance is one of the most ambitious DeFi protocols ever built. It is not a single dApp pretending to be a platform. It is genuinely a stack of interconnected products that together form an onchain monetary system. FRAX and frxUSD provide the unit of account. frxETH and sfrxETH provide the productive base asset. Fraxlend, FraxSwap, and FraxFerry provide the payment rails. Fraxtal provides the execution venue. AMOs provide the central-bank-style treasury management. FXS provides the governance and value-capture layer that ties it all together.

The 2023 FXG vote to fully collateralize FRAX was a watershed moment. It removed the algorithmic narrative risk that had been hanging over the protocol since the Terra collapse, and it set Frax on a path toward credibility with institutional users and regulators. The 2024 launch of Fraxtal added a sovereign execution layer where Frax controls the gas economy, the points program, and the long-term ecosystem direction. The 2025-2026 evolution toward frxUSD and tokenized treasury backing extends Frax into the real-world asset narrative.

For users, Frax offers something genuinely different from a single-purpose stablecoin or LST. You can hold FRAX, stake frxETH, lend on Fraxlend, swap on FraxSwap, bridge via FraxFerry, and accumulate FXTL points on Fraxtal, all within a single coherent ecosystem governed by the same token. Whether that consolidation is a feature or a risk is partly a matter of taste and partly a matter of how the protocol continues to manage its growing complexity.

If you are new to Frax, start small. Mint a modest amount of FRAX from USDC to learn the flow. Stake a small amount of frxETH into sfrxETH to see how yield accrues. Lend a small amount on Fraxlend to experience isolated pair markets. Bridge a small amount to Fraxtal to start earning FXTL points. Once you understand each product in isolation, you can begin to combine them into strategies that fit your goals. As always, never invest more than you can afford to lose, verify every URL and contract address, and use a hardware wallet for any meaningful balance. The Frax ecosystem rewards patience and curiosity more than speed and recklessness.

Related Guides

- What Is Lybra Finance (LBR)? eUSD Stablecoin + LSDfi Guide 2026

- What Is Curve Finance? Stablecoin AMM, veCRV and CRV Token Explained (2026)

- How to Use Curve Finance: Stablecoin Swaps, Pools and Slippage Guide (2026)

- How to Use DefiLlama: Track TVL, Stablecoins and Protocol Revenue (2026)

- Pendle Finance Explained: Yield Tokenization, PT, YT and Fixed-Rate DeFi (2026)