TWAP Order Crypto: Complete Execution Guide 2026

— By Whatsertrade in Tutorials

TWAP order crypto guide. Slice large trades, minimize slippage and dodge MEV with Hyperliquid, Binance Algo, CoW Swap and Uniswap V4 TWAMM.

A TWAP (Time-Weighted Average Price) order splits a large trade into smaller slices executed at regular intervals over a specified time period. It targets the average market price across the window, which reduces slippage on big orders, hides trading intent from copy traders and MEV bots, and produces more predictable execution than firing a single market order into a thin book.

TWAP Order Crypto: Why Power Traders Refuse to Buy in One Click

If you have ever clicked market buy on a low cap token and watched the price spike, fill at a worse number, then immediately retrace, you have already paid the tax that TWAP orders exist to fix. The bigger the order, the thinner the book, the worse the surprise. Whales know this. Market makers know this. Bots know this. Retail usually finds out the hard way.

A TWAP order is one of the oldest execution algorithms in traditional finance, and over the last three years it has become a native primitive on the platforms power users actually trade on. Hyperliquid built it directly into the order panel. Binance ships it under Algo Orders. dYdX, Vertex, Drift and Aevo expose it in their advanced order menus. CoW Swap turned it into an on chain intent. Uniswap V4 made it a hook called TWAMM. If you are still pasting trades in one shot you are working harder than you need to.

This guide is the long version. We will cover the math, the difference between TWAP and VWAP, how TWAP compares to VWAP, iceberg, sniper and DCA, where to actually place a TWAP order today, how to choose duration and slice count, how TWAP interacts with MEV and sandwich attacks, and step by step walkthroughs for Hyperliquid, Binance Algo and CoW Swap.

What Is a TWAP Order in Crypto?

TWAP stands for Time Weighted Average Price. As an execution algorithm, a TWAP order takes one parent order, breaks it into N child orders of roughly equal size, and releases them into the market at fixed intervals across a chosen time window. The target is simple: match the average market price over that window. The formula is the unweighted arithmetic mean of prices sampled at equal time intervals.

That is the entire mathematical content. The interesting part is everything around the formula, which child order size to use, what interval is safe, when to randomize timing, whether to allow limit prices, and how to defend against actors who can see your slices land.

A TWAP differs from a normal market order in one crucial way: instead of taking liquidity all at once and accepting whatever price the book gives you, it spreads the impact over time so the market has room to refresh between fills. The lender of that time is you. You give up immediacy. You buy back execution quality.

A Short History: From Equities Desks to Hyperliquid

TWAP and VWAP were both born on traditional equities trading desks in the late 1980s and 1990s. Institutional brokers needed a way to fill multi million share orders without telegraphing their flow to the rest of the floor. Goldman Sachs, Morgan Stanley and Instinet popularized TWAP as the default "neutral" execution algorithm because it required no volume profile, only a clock.

Crypto inherited the concept slowly. Early Bitcoin OTC desks used manual TWAP, an analyst clicking buy every five minutes. By 2018, exchanges like Coinbase Prime, Kraken OTC and FalconX offered TWAP execution as a service for institutional clients. Around 2020, BitMEX and FTX exposed basic algo orders to retail.

The real shift came with Hyperliquid in 2023. They put TWAP directly in the spot and perps order panel, no API code required. By 2025, Binance had launched Algo Orders under the spot interface with TWAP as a first class option, and DEX side, Uniswap V4 introduced the TWAMM hook that lets long duration TWAPs run trustlessly as a smart contract. CoW Swap layered TWAP on top of its intent based aggregator model in late 2023, making TWAP a native feature of MEV resistant DEX trading.

How a TWAP Order Actually Works Under the Hood

The naive description is "split a trade into pieces over time", but real implementations are smarter than that. Here is the typical flow when you submit a TWAP through a modern crypto venue.

Inside the venue, the algo engine usually does three things smarter than a manual user could. First, it adds jitter, randomizing the exact second a slice releases inside a window around the expected interval so MEV searchers cannot predict when liquidity is about to be hit. Second, it ranges the child size, releasing 0.8x to 1.2x of the average slice instead of an obvious round number. Third, on perpetual venues it watches the funding rate and order book mid drift, optionally pausing if a sudden spread blowout makes filling expensive.

On DEX TWAPs like CoW Swap, the same logic lives in a settlement contract. Each child order is auctioned to solvers who compete to give the best execution. Uniswap V4 TWAMM goes further, using a continuous virtual order book where the TWAP fills proportionally with every block rather than in discrete chunks.

TWAP vs VWAP: The Two Cousins That Aren't the Same

Beginners often treat TWAP and VWAP as interchangeable. They are not. The difference is what the average is weighted by.

Each time interval gets equal weight regardless of how much volume traded in that window. A quiet 3am bar counts the same as a high volume noon bar.

Use when: the trade is not benchmarked against market volume, you want simple predictable scheduling, or you are operating in 24/7 crypto markets where volume profile is unstable.

Each interval is weighted by the volume that traded during it. Heavy volume periods dominate the average. Filling in line with volume minimizes implementation shortfall.

Use when: you are benchmarked against a volume curve, executing during a defined session, or trading equities and equity style instruments with clear intraday rhythm.

In equities the choice matters a lot because regulated sessions have well known volume curves with predictable opens and closes. In crypto, volume is noisier, weekend liquidity collapses, and listings can dump 80% of daily volume in a 15 minute window after a tweet. That noise is exactly why most crypto desks default to TWAP. You do not need to forecast volume to schedule a TWAP. You only need a clock.

VWAP still matters as a benchmark. Traders compare their fill price against the period's VWAP to score execution quality. But for live order routing, TWAP is the cleaner crypto native primitive.

TWAP vs Iceberg vs Sniper vs DCA

TWAP is one of several execution patterns, each solving a different problem. Mixing them up leads to using the wrong tool for the job.

Practical translation. If your concern is "I do not want my $200k buy to be obvious in the order book", iceberg is your tool. If your concern is "I am willing to wait for $1,950 ETH and nothing else", you want a sniper or a hard limit. If your concern is "I want average daily exposure as a long term saver", that is DCA, the slowest of the family.

TWAP sits in the middle. It is for traders who already decided they want exposure now (today, this hour, this session) but who care about not paying tourist prices on the way in. The classic combo is TWAP for the bulk of a position with a sniper limit as a backstop in case price unexpectedly hits a great level mid window.

Why Traders Reach for TWAP: The Five Real Reasons

A 200 BTC market sell on a venue with 60 BTC top of book obliterates 4 to 6 levels of bids. The same 200 BTC TWAPed over 60 minutes hits at the mid most of the way.

Hyperliquid leaderboards expose every whale's trades in real time. Drip filling via TWAP makes it harder for followers to ride your wave and exit on top of you.

If you have no edge on direction in the next hour, the lowest variance entry is the time average. TWAP gives you exactly that, by construction.

A single $500k AMM swap is sandwich bait. A CoW Swap TWAP or TWAMM filling per block makes the same trade un sandwichable in practice.

Once you commit to a 30 minute TWAP you stop second guessing every candle. The algorithm becomes a commitment device against fear and FOMO.

Where TWAP Lives Today: Five Venues That Matter

Here is where you actually find a usable TWAP in 2026, ordered from "easiest UX" to "most powerful for big size".

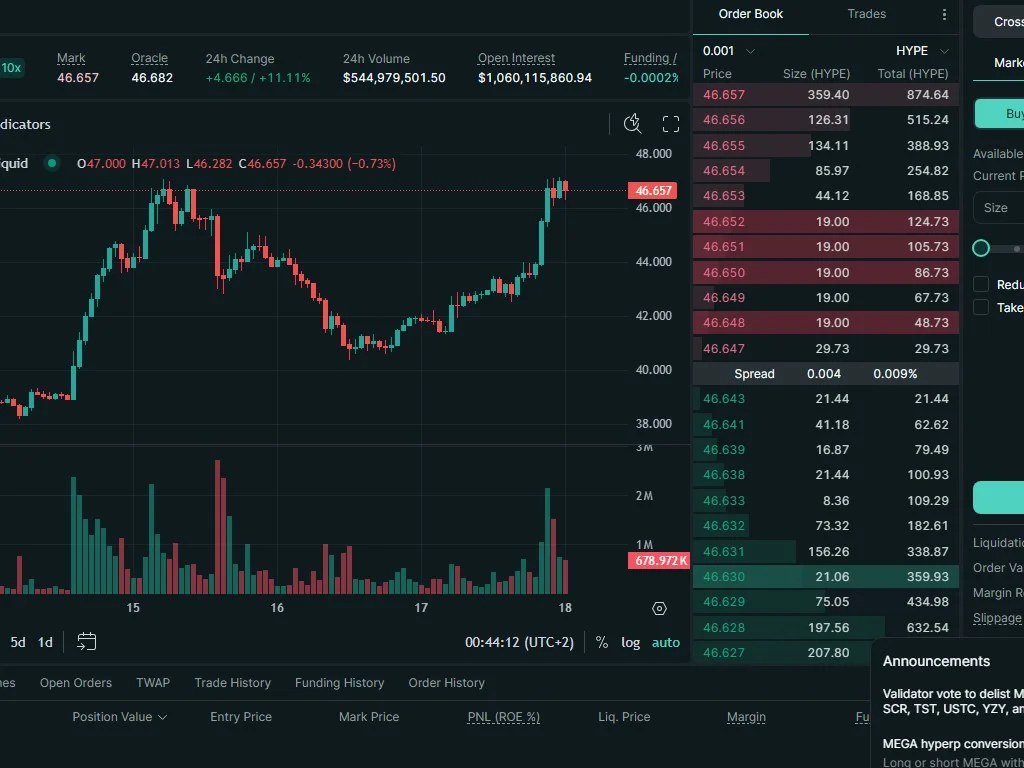

1. Hyperliquid Native TWAP

Hyperliquid put TWAP right next to Market, Limit and Stop in the order panel. You toggle TWAP, type a size and a duration in minutes (default 30), and the venue handles slicing. Each slice releases roughly every 30 seconds with jitter, sized to spread the total order evenly across the window. There is no per slice fee surcharge, you just pay maker or taker on each child fill. For perps traders running $100k to $5M positions this is the fastest path to clean execution. The only gotcha is that funding can drift during longer TWAPs, so on 4h or 24h windows traders sometimes pair it with funding hedges.

2. Binance Algo Orders TWAP

Binance exposes TWAP under Spot and Futures via the Algo Orders tab. You pick total quantity, duration (5 minutes up to 24 hours), and the engine handles the rest. Binance's implementation is conservative, it tries to stay close to the spread and will pause briefly if it detects unusually wide books. Liquidity here is unbeatable for BTC, ETH, SOL and any top 30 pair. For mid cap altcoins, the engine sometimes leaves residual quantity that you have to clean up manually at the end of the window.

3. CoW Swap TWAP Orders (DEX)

CoW Swap turned TWAP into an on chain intent. You sign an order that says "buy X amount of token Y, split into N parts, every T seconds". Solvers compete to fill each tranche through whatever route gives the best price, and CoW's batch auction model means each slice gets MEV protected execution by default. This is the cleanest way to TWAP large DEX positions in stables or majors without leaving on chain. Cost is a per slice settlement fee plus the solver spread.

4. Uniswap V4 TWAMM Hook

The TWAMM (Time Weighted Average Market Maker) hook in Uniswap V4 hooks takes TWAP to its logical extreme. Instead of discrete child orders, your TWAP is a continuous stream of virtual orders that fills proportionally every block. There is no fixed slice count, no exposed transaction per slice, and the order is effectively invisible to MEV searchers because it lives inside the pool's state, not the mempool. Best for long duration (24h+) accumulations in highly liquid pools.

5. dYdX, Vertex, Aevo, Drift

The other major perps venues all ship TWAP in their advanced order types. The implementations are similar to Hyperliquid, child orders every 15 to 60 seconds with jitter, configurable duration, native to the order panel. The choice between them is usually a function of which chain you are on (Solana for Drift, Arbitrum for Vertex) and where the liquidity for your specific pair lives.

Choosing TWAP Duration: 15 Minutes, 1 Hour, 4 Hours or 24 Hours?

The single biggest mistake in TWAP usage is picking a duration that does not match the trade thesis. Too short and you lose the slippage benefit. Too long and the market drifts away from your idea before you finish filling.

Quick heuristic. Take your intended size and divide by the venue's average 1 minute volume on the pair. If your size is 10% or less of one minute volume, 15 minutes is plenty. If it is 100% of one minute volume, target 1 to 2 hours. If it is several multiples of one minute volume you probably want 4+ hours, or you should not be putting that size through that venue at all.

Slice Count: More Is Not Always Better

Slice count interacts with duration. Most engines default to a slice every 15 to 60 seconds. Going finer (a slice every 5 seconds) increases gas costs on chain, increases per slice fees on CEX, and rarely improves the average fill price. Going coarser (one slice every 5 minutes) starts to look like a limit ladder and loses the smoothness benefit. Default ranges work for almost everyone. Tune only if you can measure execution quality and prove the change helps.

MEV Considerations: Can a TWAP Be Sandwich Attacked?

Short answer: yes, a naive TWAP on a public AMM is sandwich bait, and that is precisely why dedicated DEX TWAP venues exist.

The attack vector is straightforward. Each slice of your TWAP is a separate transaction in the mempool. An MEV searcher sees slice N, front runs it with a buy to push the price up, lets your slice fill at the worse price, then back runs with a sell to capture your slippage. Repeat for every slice. A 10 slice TWAP becomes 10 small sandwiches instead of one big one. Worse, the predictable cadence of slices on naive implementations makes it easier, not harder, to target.

Defenses that work in practice:

- Use a CoW Swap TWAP order, every slice goes through a batch auction and is solver settled, so the typical mempool sandwich path does not apply.

- Use Uniswap V4 TWAMM, fills happen inside the pool's state per block, with no mempool transactions to front run.

- Submit through a private RPC (Flashbots Protect, MEV Blocker), which hides your transactions from the public mempool entirely.

- Use a CEX TWAP on Hyperliquid, Binance, dYdX, where the venue is the only one that sees your child orders, removing public mempool MEV from the equation.

- Randomize slice cadence, quality algo engines already do this. If you are scripting TWAP yourself, never use a perfectly regular interval.

The classic mistake is running a TWAP by manually sending 10 swaps through MetaMask on a Uniswap V3 pool with low slippage tolerance. That just hands the MEV bots a clock to time their sandwiches to. If you cannot use a TWAP aware venue, do not TWAP, just send one larger swap through a private RPC.

Step by Step: TWAP Order on Hyperliquid

Hyperliquid has the cleanest TWAP UX in the industry. Here is the end to end flow for buying $80,000 of perpetual SOL over 30 minutes.

- Open the SOL perp. In the right side order panel, click the order type selector and choose TWAP.

- Pick direction. Toggle Buy / Long.

- Enter size. Type the USD or SOL amount you want to fill. The engine will convert.

- Set the duration. Default is 30 minutes. For 80k on SOL that is fine, the venue does several million per minute.

- Set leverage. Adjust your leverage slider before submitting if you are using anything other than the default.

- Submit. A confirmation modal shows the parent order, estimated slice count and slice interval. Confirm.

- Monitor. The order appears in the Open Orders tab as a parent TWAP with a fill progress bar. Each child fill is logged in Trade History.

- Cancel if needed. Cancelling the parent stops future slices but keeps everything already filled. You can mid window flip from TWAP to limit if conditions change.

If you are sizing across multiple Hyperliquid pairs in a coordinated rotation, you can launch parallel TWAPs and let them all run, the venue handles them independently.

Step by Step: Binance Algo Orders TWAP

- Open the spot or futures pair. Click the order type tab and switch from Limit / Market to Algo Orders, then choose TWAP.

- Enter total quantity. In base asset units (BTC, ETH, etc) or USDT.

- Pick duration. Dropdown ranges from 5 minutes to 24 hours.

- Optional limit price. Binance lets you cap how aggressively the engine reaches across the spread. Leaving it blank means it will accept whatever the market gives within reason.

- Review the slice plan. Binance shows an estimated number of orders, average size per order, and fee schedule.

- Submit. The parent appears in your Algo Orders tab.

- Inspect post fill. Once complete, Binance reports the average fill price, total fees, and the implementation difference vs the period's VWAP. This is the report you want to read to improve.

For pairs outside the top 30, watch the residual. If the TWAP cannot complete because the asset is too thin, Binance leaves a remainder for you to handle manually. This is a feature, not a bug, it stops the engine from chasing.

Step by Step: CoW Swap TWAP (On Chain, MEV Protected)

CoW Swap TWAPs are the cleanest way to fill large DEX trades without getting sandwich attacked. The setup lives under Advanced order types.

- Connect a Safe or EOA wallet. CoW Swap TWAPs work best from a Safe multisig because the settlement is non custodial and the order persists across slices.

- Pick sell and buy tokens. For example sell 1,500,000 USDT and buy WETH.

- Toggle TWAP under Order Type. Set number of parts (slices), interval between parts, and start time.

- Optional limit price. You can set a per slice minimum fill price so a sudden adverse move pauses the strategy.

- Sign the order. One signature authorizes the entire TWAP. Solvers will fill each slice in sequence.

- Watch fills. The CoW Swap dashboard shows each slice as it settles, with effective price and solver name.

- Cancel any time. A single transaction cancels the remaining schedule. Already filled slices are final.

Because CoW Swap settles in batch auctions, you get MEV protection by default and often beat the AMM mid price thanks to coincidence of wants matches with other users in the same batch. This is the closest thing to an institutional TWAP desk available to anyone with a wallet.

TWAP for Institutions and Whales

Institutional desks have been TWAPing since before crypto existed. The pattern translates almost unchanged: a trader at a fund receives a parent order from the portfolio manager, splits it into a TWAP scheduled across the session, and reports back on the implementation shortfall vs the period VWAP at the close.

In crypto specifically, three additional concerns come into play. First, 24/7 markets mean there is no closing bell to benchmark against, so desks pick reference windows (UTC midnight to UTC midnight is common). Second, fragmented liquidity across CEX, DEX and dark pools means a real institutional TWAP often splits across several venues, with a smart router scheduling slices to wherever liquidity is best at that second. Third, on chain transparency makes hiding intent harder, leading many funds to prefer CoW Swap, TWAMM or RFQ flow for their largest DEX trades.

For whales (defined here as anyone whose single trade size is meaningfully large relative to top of book), the calculation is similar but more aggressive on MEV defense. The dominant pattern in 2026 is to run a perp TWAP on Hyperliquid for the directional bet while simultaneously running a stablecoin TWAP on CoW Swap for the spot accumulation, with a quant hedging the basis between them.

TWAP for Retail Power Users

You do not need to be a fund to benefit from TWAP. The retail patterns that work:

- Memecoin and low cap entries. A 30 minute TWAP on Hyperliquid spot or via CoW Swap dramatically beats a single market buy on a low cap with thin order books. See our guide on detecting fake volume first to make sure the book is real.

- Profit taking on perp wins. Closing a big winning long with a single market sell announces your exit to every leaderboard follower. A 15 minute TWAP exit gets you out at a better average and quieter.

- Rebalancing into stables before bad news windows. Moving 50% of a portfolio to USDC ahead of a CPI print is much smoother as a 1 hour TWAP than as a panic flush.

- Entering a contrarian position. If you are buying the dip on ETH and not sure exactly where the bottom is, a 4 hour TWAP commits you to a position while removing the "did I catch the exact low" anxiety.

Risks and Honest Tradeoffs

- Reduced slippage on large orders

- Hidden intent vs copy traders and front runners

- Predictable average price by construction

- Discipline against FOMO and panic

- MEV protection on DEX TWAP venues

- Works equally well for entries and exits

- Adverse selection if market trends against you

- Per slice fees on some venues add up

- Slow exposure means missing fast moves

- Funding can drift on long perp TWAPs

- Naive TWAP on AMM is still sandwich bait

- Residual quantity if liquidity is too thin

The adverse selection point deserves its own paragraph. TWAP gives you the average price of the window. If the market rips up 8% during your 1 hour TWAP buy, you will fill at a much worse average than if you had taken the whole thing at the start. Conversely, if it dumps 8% you will get a much better average. By definition, TWAP trades best execution for average execution. If you have a strong directional view in the next hour, TWAP is the wrong tool, use a market order or a limit at your target.

TWAP vs Limit Ladders: When to Pick Which

Some traders argue limit ladders (a stack of resting limit orders at descending price levels) replace TWAPs entirely. They do not, and the distinction is worth understanding.

A limit ladder fills only at your specified prices. If the market never reaches them, you do not fill. If it spikes past one of them, you fill instantly at exactly that level. Limit ladders express a view about where price is going. They are great for "I want to buy if and only if ETH dips to $2,000, $1,950 or $1,900."

A TWAP fills regardless of price (within whatever protective limit you set). It expresses a view about wanting exposure, not about specific entry levels. The two combine well: a TWAP for the base position with a limit ladder underneath to catch unexpected dumps for free bonus fills.

Best Practices for TWAP Execution

- Always size the TWAP relative to venue liquidity. Pull up market maker top of book and 1 minute trade volume before deciding duration.

- Use a protective limit if your venue supports it. A limit price that pauses execution if the market moves 3 to 5% against you saves a lot of bad fills during sudden moves.

- Pair TWAP with on chain monitoring. If you are TWAPing into a token, set up an alert for unusual whale flows or liquidation zones that might dump price mid execution.

- Pick the right venue for the asset. Hyperliquid for perps, Binance for top 30 spot, CoW Swap for large DEX flows, TWAMM for very long durations.

- Review every TWAP after it completes. Compare your average fill to the period VWAP. If you consistently underperform VWAP, your duration or venue choice is wrong.

- Do not panic cancel mid window. The entire benefit of TWAP is structure. If you cancel because price moved a little, you remove the discipline benefit and pay slippage on the residual.

- Combine with hedges on long durations. For 4h+ TWAPs in volatile markets, a tactical perp hedge offsets directional risk during the fill window.

- Never TWAP through public mempool transactions. Either use a venue with built in MEV protection or route through a private RPC.

A Quick Word on TWAP Bots and Scripted TWAPs

Plenty of trading firms run their own TWAP scripts. The basic logic is a loop that fires market orders every N seconds for M minutes. Writing one yourself is a useful exercise in understanding the mechanics, but production use almost always loses to native venue TWAP because:

- Your script is one client among many, the venue's algo engine has co located infrastructure and lower latency.

- Your slice cadence is exposed in API logs and can be reverse engineered.

- You do not get the benefit of randomization, smart order routing, or pause on spread blowout that native engines apply automatically.

- You pay full taker fees on every slice, native algo orders sometimes get fee discounts or maker rebates on a portion of fills.

Use scripted TWAP for prototyping or for venues without native support. For everything else, the native button is faster, cheaper and safer.

Frequently Asked Questions

Q Q Q What is a TWAP order in crypto?

A TWAP (Time-Weighted Average Price) order splits a large trade into smaller slices that execute at regular intervals across a defined time window. The fill price approximates the simple time average of the asset's price during that window, which minimizes the slippage and price impact of putting a big order through the book all at once.

Q Q Q TWAP vs VWAP: what is the actual difference?

TWAP weights every time interval equally, regardless of volume. VWAP weights each interval by the volume that traded in it. In crypto's 24/7 markets, volume is noisy and unpredictable, so TWAP is the simpler default for live execution. VWAP is still widely used as a benchmark to score how well a fill performed relative to the period's volume weighted average.

Q Q Q Which exchanges offer TWAP orders natively?

Hyperliquid puts TWAP in the main order panel. Binance offers it under Algo Orders on spot and futures. dYdX, Vertex, Aevo and Drift all expose TWAP in their advanced order types. On the DEX side, CoW Swap supports TWAP orders as on chain intents and Uniswap V4 has a TWAMM hook for continuous block by block fills.

Q Q Q Can a TWAP order be sandwich attacked?

Yes, naive TWAPs executed as public mempool transactions on AMMs can be sandwich attacked at every slice. Defenses include using CoW Swap TWAP (batch auction settled), Uniswap V4 TWAMM (fills inside pool state), routing through private RPCs like Flashbots Protect, or using CEX TWAP where the venue is the only one that sees your child orders.

Q Q Q Is TWAP the same as DCA?

No. DCA (Dollar Cost Averaging) is a long term investing strategy that buys a fixed amount over days, weeks or months. TWAP is a short term execution algorithm typically running for minutes or hours. TWAP optimizes a single trade's fill price. DCA optimizes a long term accumulation path.

Q Q Q How long should a TWAP order last?

It depends on your size relative to venue liquidity. For most retail orders on liquid pairs, 15 to 60 minutes is the sweet spot. For larger positions or thin altcoins, 2 to 4 hours. For institutional accumulation, 24 hours or longer via TWAMM. Shorter durations give less slippage protection but less direction risk. Longer durations are smoother but expose you to market drift.

Q Q Q Can I use TWAP for exits, not just entries?

Yes, TWAP works equally well for selling. Many traders use exit TWAPs to liquidate large winning positions without telegraphing to copy traders or moving the market against themselves. The same duration and venue choice logic applies.

Q Q Q What is Uniswap V4 TWAMM?

TWAMM (Time Weighted Average Market Maker) is a Uniswap V4 hook that lets users post long duration TWAP orders directly into a liquidity pool. Instead of discrete slice transactions, the order fills continuously, proportionally with every block, using the pool's state. This makes the order invisible to MEV searchers because there are no per slice mempool transactions to front run.

Q Q Q What is a CoW Swap TWAP order?

A CoW Swap TWAP is an on chain intent that splits a swap into N parts executed at regular intervals. Solvers compete to fill each tranche through whatever route gives the best price, and CoW's batch auction model provides MEV protection by default. It is the cleanest way to TWAP large DEX positions without leaving on chain or exposing yourself to mempool front running.

Q Q Q What is the difference between TWAP and an iceberg order?

An iceberg order is one large limit order that displays only a small visible tip in the order book and reveals more as the visible portion fills. It hides size but is fully passive. A TWAP is an active execution algorithm that slices and releases child orders over time to average the price. Iceberg targets stealth at a single price. TWAP targets average price over a window.

Q Q Q Do TWAP orders cost more in fees?

Most CEX venues do not charge a TWAP surcharge, you pay normal maker or taker fees on each child fill. On DEX, you pay gas or settlement fees for every slice, which can add up over many small slices. CoW Swap charges a per slice fee plus the solver spread. The net cost is usually still well under the slippage savings on large orders.

Q Q Q Can I cancel a TWAP order mid execution?

Yes. Cancelling the parent TWAP stops any future child orders from being released. Slices that already filled are final. On CoW Swap and TWAMM, cancellation is a single transaction. On CEX, it is a single click. That said, the entire benefit of TWAP comes from sticking to the plan, so panic cancellation usually defeats the purpose.

Final Take: TWAP Is a Default, Not a Trick

The mental shift that takes a trader from intermediate to advanced is realizing that execution quality is a measurable, controllable edge. Every basis point you give up to slippage, MEV or telegraphed flow is a basis point you do not need to earn back with directional accuracy. TWAP is the single easiest tool to start capturing that edge today, on the venues you already use.

The playbook is not complicated. For perps, use Hyperliquid's native TWAP. For top tier spot, use Binance Algo Orders. For DEX accumulation, use CoW Swap TWAP or, for very long durations, Uniswap V4 TWAMM. Pick durations that match your size relative to venue liquidity. Use protective limits when offered. Defend against MEV by routing through venues built to handle it. Review your fills against VWAP after every TWAP and tune what does not work.

Crypto trading is moving toward a world where execution is increasingly automated, intent based, and MEV aware. TWAP is the entry point to that world. Once it becomes muscle memory, the question stops being "should I use a TWAP here" and starts being "is there any reason not to". For most non urgent trades of any meaningful size, there is not.

If you want to deepen the toolkit around TWAP, the related execution and trading guides on DexTools are worth a read in order: VWAP explained, backtesting strategies, long vs short positioning, transaction simulation for sanity checking DEX trades, Permit2 token approvals when interacting with newer DEXs, and Pyth oracles for the price feeds that power most modern execution venues. Stack them together, and you stop trading like a tourist.

Related Guides

- Stop-Limit vs Stop-Market Orders: Crypto Guide 2026

- Not.Trade Limit Orders: TON Memecoin MCAP Triggers Guide 2026

- How to Use 1inch for Swaps: Classic, Fusion and Limit Orders (2026)

- What Is Order Flow in Crypto Trading? How to Read Buying and Selling Pressure (2026)

- What Is an Order Book in Crypto? Complete 2026 Guide