What Is an Order Book in Crypto? Complete Guide (2026)

— By Tony Rabbit in Tutorials

Master crypto order books in 2026: bids, asks, spread, depth, and spoofing, plus CLOB vs AMM and how Binance, Coinbase, and Hyperliquid compare.

If you have ever opened the trading screen on Binance, Coinbase Advanced, Bybit, or Hyperliquid and seen two stacks of red and green numbers moving like a heartbeat, you were looking at an order book. It is the single most important visualization in trading, and the one most beginners learn to read last. This guide changes that, because in 2026 the order book is no longer a centralized exchange artifact, it is the structural backbone of the fastest growing corner of crypto: perpetual decentralized exchanges.

An order book is a real-time list of all buy and sell orders for an asset, organized by price level. That definition fits in a single sentence, but the implications stretch across every trade you place. The order book is where liquidity lives, where slippage is born, where whales hide behind iceberg orders, and where market makers and takers exchange risk thousands of times per second. Reading it well is the difference between a trader who understands execution and one who keeps wondering why their fills look bad.

By the end of this guide you will be able to decode bids, asks, depth, spread, imbalance, walls, and manipulation patterns like spoofing and layering. We will compare central limit order books (CLOBs) with automated market makers (AMMs), tour the dominant CEX and DEX venues including Binance, Coinbase, Bybit, OKX, Hyperliquid, dYdX v4, Vertex, and Injective, and explain why perp DEX volume hit fresh records in 2026 with Hyperliquid alone clearing over $3.5 billion in daily perpetual volume.

Quick answer: what is an order book in crypto?

An order book is a real-time list of all buy and sell orders for a crypto asset, organized by price level. Buy orders (bids) sit on one side, sell orders (asks) sit on the other, and the gap between the highest bid and lowest ask is called the bid-ask spread. The book shows traders where liquidity is resting, how much size is waiting at each price, and how a market order will travel through the available depth.

- Anatomy of a crypto order book

- A short history of order books in crypto

- How order books actually work

- Order types: market, limit, stop, iceberg, OCO

- Reading the depth chart visualization

- Order book imbalance as a signal

- Market makers vs takers

- Spoofing, layering, and whale walls

- CEX order books: Binance, Coinbase, Bybit, OKX

- DEX order books: Hyperliquid, dYdX v4, Vertex, Injective

- CLOB vs AMM: which model wins what

- How to read an order book step by step

- Common mistakes and best practices

- Frequently asked questions

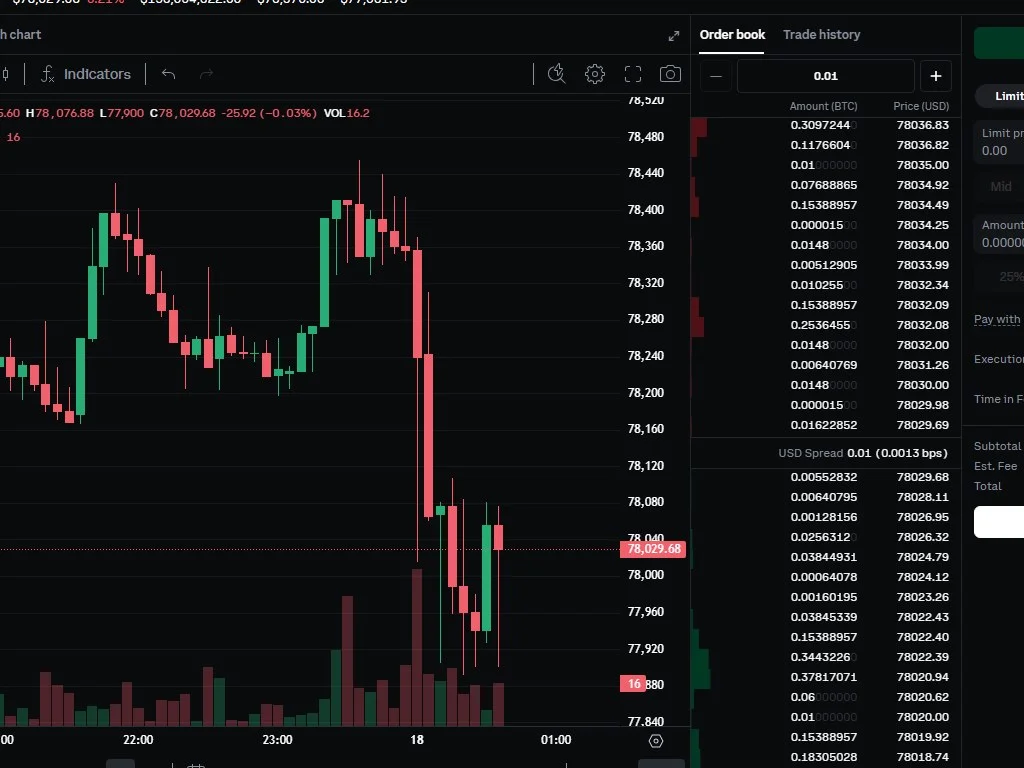

Anatomy of a crypto order book

Every order book has the same five components, regardless of whether you are looking at Binance spot, Coinbase Advanced, or Hyperliquid perpetuals. The bid side lists buy orders sorted from highest to lowest price. The ask side lists sell orders sorted from lowest to highest price. The last price sits between them, representing the most recent executed trade. The bid-ask spread is the numerical gap between the best bid and best ask. And depth is the cumulative size resting on each side at various distances from the mid price.

That sounds simple, but each piece carries information. The bid side tells you where buyers are willing to commit capital. The ask side tells you where sellers want to unload supply. The last price tells you who won the most recent battle between the two. The spread tells you how competitive market making is on that venue. And depth tells you how much real liquidity exists, which directly governs how much your trade will move the price.

Sorted highest to lowest. The top bid is the best buy price available. Stack size at each level shows how much demand is queued.

Sorted lowest to highest. The top ask is the best sell price. Size at each level shows how much supply sellers are offering.

Numerical gap between the top bid and top ask. Tight spreads mean efficient markets, wide spreads mean fragility.

Total volume resting within a percentage band of mid. Deeper books absorb large orders without major slippage.

The last price is sometimes overlooked, but it is the one number that anchors the rest. A book where the last print is closer to the best ask suggests aggressive buying, while a last print near the best bid suggests aggressive selling. Watching where the last price sits relative to bid and ask, trade by trade, is one of the oldest tape reading techniques in financial markets, and it still works in 2026 on every venue from Binance to Hyperliquid.

A short history of order books in crypto

The earliest crypto exchanges in 2010 and 2011, including Mt. Gox and later Bitstamp, were straight imports of the order book model from traditional finance. They ran central limit order books because nobody had invented anything else yet. Coinbase launched its first matching engine in 2012, Bitfinex followed in 2013, and by 2014 the order book was the universal interface for trading any cryptocurrency.

Then 2018 introduced a different model. Uniswap V1 went live with an automated market maker that replaced the order book entirely with a constant product formula. For the first time, traders could swap tokens without any counterparty resting an order on a book. Liquidity providers deposited pairs of assets into pools, and a deterministic curve set the price. This was the dawn of DeFi as we know it, and for a few years it looked like AMMs might make order books obsolete on chain.

By 2022 it was clear that AMMs were not a perfect replacement. Slippage on large orders was punishing, impermanent loss drained passive liquidity providers, and capital efficiency was poor compared to professional market makers quoting on a CLOB. dYdX migrated to its own Cosmos app chain to build a true order book DEX. Hyperliquid launched in 2023 on its custom L1 with an on chain matching engine running at CEX speeds. Vertex launched a hybrid orderbook plus AMM model. Injective built a fully decentralized CLOB from day one. By 2025 perpetual DEX volumes were rivaling spot CEX flows, and by 2026 Hyperliquid alone routinely clears over $3.5 billion in daily perpetual volume, proving that the order book never went away, it just had to wait for the right infrastructure.

The broader timeline is worth remembering because it explains why the design space is so diverse today. Spot CEX order books inherited their structure directly from equities and futures venues. Early DEX experiments rejected order books because Ethereum block times made matching too slow. The arrival of high throughput L1s, app chains, and rollups specifically tuned for order book throughput closed that gap. By the time Hyperliquid hit production it was clear that order books and AMMs would coexist permanently, each occupying the venues and asset classes where their tradeoffs make most sense, rather than one displacing the other.

How order books actually work

An order book is maintained by a matching engine, the piece of software that receives orders, ranks them, and pairs buyers with sellers. The matching engine follows a strict priority rule called price-time priority, which means the order with the best price executes first, and if two orders sit at the same price, the one that arrived first gets matched first. This priority is why latency matters so much for professional traders, and why every CEX runs co-located market making infrastructure.

When you submit a limit order at a price that does not cross the spread, the matching engine adds it to the book at the correct level. When you submit a limit order at a price that does cross the spread, or any market order at all, the matching engine starts consuming resting liquidity on the opposite side. Your order eats through the best ask (if buying) or best bid (if selling), walking up or down the book until it has filled its full size.

Every fill produces a print on the tape and updates the last price. The matching engine then broadcasts the new state of the book to every connected client via websocket, which is why your order book interface updates in real time. On a fast CEX like Binance, the book state is broadcast hundreds of times per second. On Hyperliquid, the L1 itself processes order book state at sub-second finality, and on dYdX v4 the chain produces blocks every few hundred milliseconds specifically tuned for CLOB throughput.

Order types: market, limit, stop, iceberg, OCO

The order book understands many different instructions. Knowing each one and when to use it is foundational to any execution strategy.

Executes immediately against the best available liquidity. Prioritizes speed over price. Pays the spread plus any depth-walking slippage. Useful when speed matters more than precision.

Rests at your chosen price (or better) until matched or cancelled. Provides liquidity if non-crossing. Earns the maker rebate on most venues. Prioritizes price over speed.

Becomes active only when price triggers a threshold. Stop-market fires a market order at trigger, stop-limit places a limit order. Used for risk management and breakout entries.

Shows only a fraction of the full order size to the book. As each slice fills, the next slice surfaces. Used by whales to hide intent and reduce information leakage.

One-Cancels-Other pairs a take-profit and a stop-loss. When one fills, the other is cancelled automatically. Standard for managed risk exits.

Sits in the book without showing in public depth feeds. Available on some CEX venues like Binance and OKX. Used by institutional desks to absorb size without telegraphing.

Iceberg and hidden orders are the most misunderstood. On Binance for example, a trader can place a 5,000 BTC iceberg order that shows only 50 BTC at a time. The book looks calm, but each time someone takes 50 BTC of the offer, a new 50 BTC slice replenishes. This is one of the reasons why depth alone can be misleading: what you see is not always what is actually waiting. Reading the tape against the displayed book is how experienced traders detect hidden liquidity, and pairing this with our guide on crypto market makers gives a complete picture of how professional liquidity sits.

Reading the depth chart visualization

Most order book interfaces include a depth chart, a side-by-side visualization that plots cumulative bid size on the left in green and cumulative ask size on the right in red. The X axis is price, and the Y axis is total resting size. The shape of these two curves tells you a lot at a glance.

A symmetrical, gradually sloping depth chart suggests a balanced two-sided market with healthy liquidity. An asymmetrical chart with a steep green wall and a flat red side suggests heavy buy support relative to sell pressure. A flat green side with a steep red wall suggests the opposite. Vertical jumps in the curve indicate large resting orders at specific price levels, often called walls, and these can act as temporary support or resistance.

The flaw in interpreting depth charts naively is that they only show what is visible. Iceberg orders, hidden orders, and conditional orders not yet triggered are absent from the curve. Algorithmic traders also pull orders rapidly as price approaches, so a beautiful wall sitting just under the bid can vanish in a single block. Treat the depth chart as a snapshot, not a contract.

Order book imbalance as a signal

Order book imbalance measures the ratio between bid size and ask size within a chosen price band, usually the top 5, 10, or 20 levels. Many short-term trading systems use imbalance as a leading indicator, on the assumption that heavily skewed books are more likely to move in the direction of the skew.

The math is simple. If the top 10 bid levels hold 800 BTC of size and the top 10 ask levels hold 200 BTC of size, the imbalance ratio is 4 to 1 favoring buyers. A persistent imbalance over several seconds tends to precede directional moves, while transient imbalance can simply reflect normal noise. Quantitative desks build sophisticated models on top of this raw signal, layering in trade flow, queue dynamics, and adverse selection metrics.

Important caveat on imbalance

Imbalance is a probabilistic edge, not a guarantee. Skilled market makers and HFT firms deliberately create misleading imbalance to bait retail flow, then pull the supporting orders before the move. Use imbalance as one input among many, never as a standalone signal. Pair it with trade flow, volume profile, and broader market context.

Market makers vs takers

Every trade has two sides, and every venue distinguishes between the maker and the taker. The maker is the trader whose limit order was already resting in the book and got filled. The taker is the trader who submitted the aggressive order that crossed the spread to hit that resting liquidity. The distinction matters because most exchanges charge different fees to each side.

Binance, for example, charges a default 0.10% taker fee and a 0.10% maker fee on spot, but the maker fee can drop to 0.02% or lower at higher VIP tiers, and can even be negative on perpetual contracts (meaning the maker gets paid a rebate). Coinbase Advanced charges 0.60% taker and 0.40% maker at the lowest tier, scaling down to 0.05% maker and 0.40% taker at the highest. Hyperliquid charges 0.025% taker and 0.0% maker on perpetuals, which is part of why professional market makers love quoting there.

The economic implication is straightforward. If you trade with limit orders that rest on the book, you pay lower fees and sometimes get paid to provide liquidity. If you trade with market orders that consume liquidity, you pay higher fees plus the bid-ask spread. Over thousands of trades, the difference between maker and taker fees can dwarf any edge in your strategy.

Spoofing, layering, and whale walls

The order book is also a battlefield for manipulation. Two specific techniques, spoofing and layering, are illegal in regulated traditional markets but remain widespread in crypto where enforcement is patchy. Knowing what they look like is essential for any trader who relies on book reading.

Spoofing is the placement of large limit orders with no intention of execution. The spoofer posts a 500 BTC bid wall just below the current price, retail traders see the wall as support and start buying, the price ticks up, and the spoofer immediately cancels the wall and sells into the demand they manufactured. Layering is the same idea but distributed across multiple price levels to create a more convincing illusion of depth. Both are designed to manipulate the perceived supply and demand balance to extract value from less sophisticated participants.

How to spot spoofing and layering

- Large walls that appear and disappear repeatedly without ever being executed

- Walls that always stay just out of reach as price approaches and retreats

- Sudden cancellation of huge resting size milliseconds before a directional move

- Asymmetric book that flips orientation within seconds without corresponding tape activity

- Persistent depth on one side that vanishes the moment price crosses into it

The defense is to weigh resting orders less heavily than executed trades. If a wall keeps showing up but the tape shows no fills at that level, treat it as informational only. If you see real prints absorbing supply at a specific price, that is a far stronger signal than a wall sitting there untouched. Combine this with our guide to detecting fake volume and you have a framework for filtering out most manipulation.

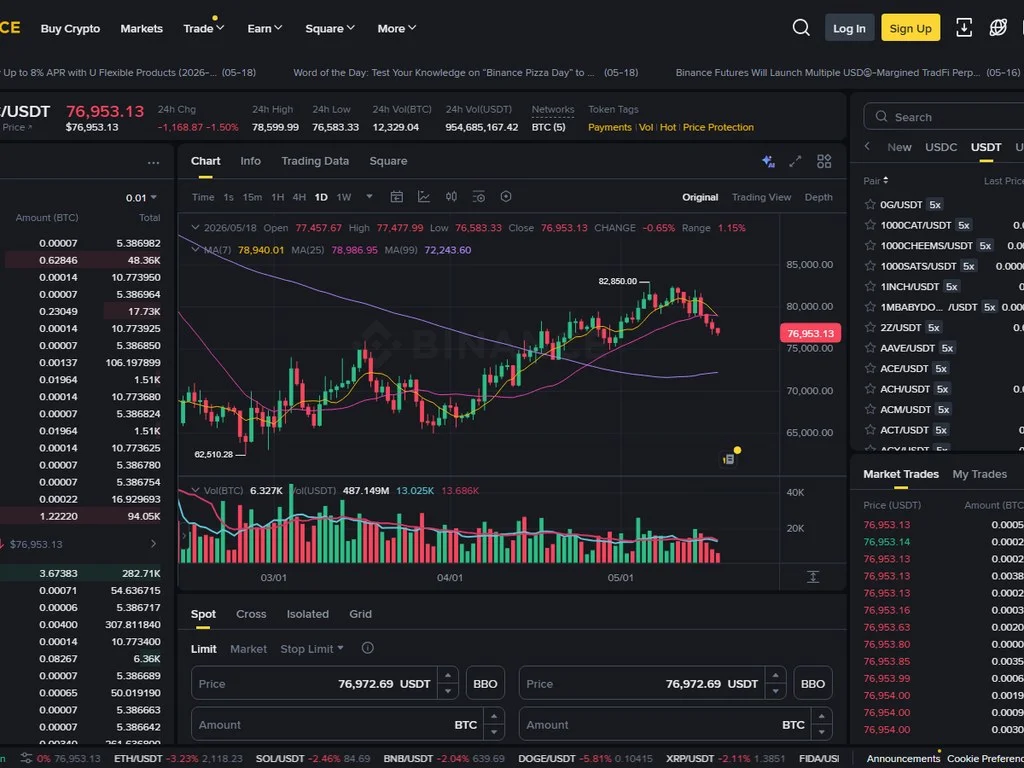

CEX order books: Binance, Coinbase, Bybit, OKX

Centralized exchanges still dominate spot crypto trading in 2026, and each of the major venues runs slightly different order book mechanics worth understanding.

Binance operates the deepest order books in crypto across spot, margin, and perpetual futures. The BTC/USDT order book typically shows over $50 million of bid size within 1% of mid, and the spread on majors is often a single tick. Binance offers full iceberg and hidden order support on the institutional API, and the matching engine processes hundreds of thousands of orders per second.

Coinbase Advanced (formerly Coinbase Pro) runs a slightly less deep book than Binance but with very tight regulation-grade compliance. Spreads on BTC-USD are typically a few basis points wider, and the venue is favored by US institutional desks for its regulatory clarity.

Bybit rose to prominence in derivatives and now offers a powerful spot book as well. The exchange supports advanced order types including conditional orders, take-profit and stop-loss attached to entry orders, and a unified trading account that consolidates margin across products.

OKX built a reputation for deep derivatives books and a sophisticated order matching engine. The platform supports trailing stops, time-weighted average price algorithms, and a robust API used heavily by quantitative trading firms.

For new traders comparing these venues, our DEX vs CEX comparison guide covers the broader tradeoffs, while our guide on selling ETH effectively walks through actual execution on these books.

DEX order books: Hyperliquid, dYdX v4, Vertex, Injective

The most explosive growth story in 2026 is on chain order books for perpetual trading. Four venues lead the category, each with a different architecture.

Hyperliquid runs a custom L1 with the entire order book matching engine on chain. Block times are sub-second, the venue charges 0.025% taker and zero maker fees, and daily perpetual volume routinely clears $3.5 billion. Hyperliquid has captured roughly 70% of all on chain perpetual volume in 2026, displacing dYdX as the dominant perp DEX. Our Hyperliquid tutorial walks through how to actually trade there.

dYdX v4 migrated from a StarkWare rollup on Ethereum to a sovereign Cosmos chain in late 2023. The matching engine runs across validator nodes, and the entire order book state is reconstructed from the chain. Volume in 2026 sits around $400 million per day on perpetuals, well behind Hyperliquid but still the second largest on chain CLOB.

Vertex runs a hybrid model that combines a CLOB with an AMM backstop. Limit orders match through the order book engine, but when the book is too thin, trades route to an integrated AMM pool to guarantee execution. This eliminates the cold-start liquidity problem that plagues new markets on pure CLOB venues.

Injective built a fully decentralized order book at the protocol layer of its Cosmos chain. Frontends like Helix and Mito tap directly into the chain-native CLOB, with shared liquidity across every UI. Injective also pioneered cross chain margin, letting users post collateral from any Cosmos chain to trade on the Injective order book.

CLOB vs AMM: which model wins what

Central limit order books and automated market makers are fundamentally different architectures, and each has clear strengths.

The verdict in 2026 is that both models will coexist permanently. CLOBs dominate where deep, liquid, professional markets exist (BTC, ETH, SOL perpetuals on Hyperliquid; spot majors on Binance). AMMs dominate where long-tail asset bootstrapping matters (new memecoins on Uniswap, niche tokens on Raydium). Hybrid models like Vertex and Injective bridge the gap. Our Uniswap V4 hooks guide explores how AMMs are evolving to compete on the dimensions where they were historically weakest.

How to read an order book step by step

Reading an order book well is a learned skill. Here is a structured approach that works on any venue.

If the bid-ask spread is wider than usual for that pair, the market is either thin, volatile, or both. Adjust position sizing and choose limit orders over market orders.

The size sitting closest to the mid price is what determines real slippage for typical trades. Far away levels matter much less. Note any unusually large clusters.

Sum total bid size versus total ask size within 1% of mid. A persistent skew can hint at directional pressure, but verify against tape activity.

When market orders eat into liquidity, does the book refill quickly or stay depleted? Fast refills indicate active market makers. Slow refills indicate fragile liquidity.

If a wall keeps appearing and vanishing without executions, it is probably spoofed. Treat walls as suspicious by default unless you see real prints absorbing into them.

The order book is only half the picture. The tape (recent trades) tells you what actually executed. A heavy buy book with a tape full of sells is a warning sign.

This six-step pattern is repeatable in seconds once you internalize it. Pair it with our VWAP guide for benchmark-aware execution, and with our liquidation zones guide to understand where forced flow may hit the book.

Common mistakes and best practices

Beginners consistently fall into the same handful of traps when learning to read order books. Avoiding these is half the battle.

- Use limit orders for size, market orders only when speed matters

- Always check spread before committing to an entry

- Weigh executed trades higher than resting orders

- Use the depth chart for the big picture, not entry timing

- Split large orders into smaller chunks to reduce slippage

- Pair book reading with volume profile and tape analysis

- Trusting every visible wall as guaranteed support or resistance

- Submitting market orders into thin books and getting destroyed by slippage

- Ignoring iceberg and hidden liquidity that does not appear in depth

- Treating order book imbalance as a guaranteed directional signal

- Not adjusting interpretation based on volatility regime

- Mistaking spoofing patterns for genuine accumulation

The single most important habit is to remain humble. The order book is a probabilistic information source, not a deterministic map. Treat it as one of several inputs into your decision making, combined with broader market structure analysis. Our long vs short guide and backtesting guide show how to integrate book insights into a complete trading workflow.

Why order book literacy matters more in 2026

Five years ago, retail traders could survive without understanding order books. Spot trading on Coinbase or Binance was simple enough that hitting the buy button worked. Today, the landscape is fundamentally different. Perpetual DEXs like Hyperliquid have brought CLOB-style trading to a new generation of on chain users, and the leverage available means execution quality matters more than ever. A 0.1% slippage on a 10x leveraged perpetual position equals a 1% hit to your collateral.

Meanwhile, the data infrastructure around order books has exploded. Tools like Velo Data, Tardis, and CoinGlass now stream historical order book snapshots that anyone can analyze. Open source projects let retail traders build custom imbalance dashboards, depth heatmaps, and spoofing detectors. The information asymmetry that used to favor only institutional desks is shrinking, but only for traders who actually learn how to use the data.

Regulatory attention is also rising. The SEC has flagged spoofing and layering as enforcement priorities for crypto venues, and several CEX operators have settled cases involving manipulative practices on their own books. As compliance tightens, the structural integrity of order book data should improve, which makes book reading skills even more valuable going forward.

Frequently asked questions

Q Q Q What is an order book in crypto trading?

An order book is a real-time list of all buy and sell orders for a crypto asset, organized by price level. Bids sit on one side, asks on the other, and the gap between them is the bid-ask spread. The book shows where liquidity is resting, how much size waits at each price, and how a market order will travel through the available depth.

Q Q Q What is the difference between bids and asks?

Bids are buy orders submitted by traders willing to purchase at a specific price or lower. Asks are sell orders submitted by traders willing to sell at a specific price or higher. The highest bid and the lowest ask together form the best market available, and the difference between them is the bid-ask spread.

Q Q Q What is order book depth in crypto?

Order book depth refers to the total volume of buy and sell orders resting at various prices around the current market. Deeper books contain more cumulative size within a narrow band of the mid price, which means large orders can execute with less slippage. Thin books cause larger price movements when sizable orders hit them.

Q Q Q How do market orders interact with the order book?

A market order is matched immediately against the best available resting liquidity on the opposite side of the book. If you submit a market buy, your order consumes the best ask first, then the next ask, and so on until your size is filled. This walking behavior is what produces slippage on large market orders, especially in thin books.

Q Q Q What is spoofing in crypto markets?

Spoofing is the practice of placing large limit orders with no intention of execution, designed to mislead other traders about real supply and demand. The spoofer creates a false wall to bait reactions and then cancels the order before it fills. It is illegal in regulated traditional markets and is increasingly targeted by enforcement in crypto.

Q Q Q Do DEXs use order books?

Some do, some do not. AMM-based DEXs like Uniswap, PancakeSwap, and Raydium replace the order book with liquidity pools and a pricing formula. Order book DEXs like Hyperliquid, dYdX v4, Vertex, and Injective run true central limit order books on chain, with matching engines that look and behave like centralized exchanges. The order book model dominates perpetual trading on chain in 2026.

Q Q Q What is the bid-ask spread and why does it matter?

The bid-ask spread is the numerical gap between the best bid price and the best ask price. A tight spread suggests efficient market making with competitive quoting, while a wide spread suggests low liquidity or high volatility. Spread is a direct cost for any trader using market orders, since they cross the spread to execute immediately.

Q Q Q What is an iceberg order?

An iceberg order is a large limit order broken into smaller visible slices. Only the current slice shows in the public depth feed, and as it fills, the next slice automatically surfaces. Whales use iceberg orders to absorb or distribute large positions without revealing their full intent, which would otherwise move the market against them.

Q Q Q What is order book imbalance?

Order book imbalance is the ratio between cumulative bid size and cumulative ask size within a chosen depth band. A persistent imbalance favoring one side can hint at directional pressure, but skilled market makers also create misleading imbalance to bait flow. Imbalance is a probabilistic input, not a guaranteed signal.

Q Q Q Which crypto exchange has the deepest order book?

Binance consistently runs the deepest spot and perpetual order books in crypto for major pairs like BTC/USDT and ETH/USDT. On the DEX side, Hyperliquid leads on chain perpetual depth in 2026 with daily volume clearing over $3.5 billion. Coinbase Advanced and OKX also offer substantial depth, while Bybit and Bitget have grown quickly in the derivatives category.

Q Q Q What is the difference between a CLOB and an AMM?

A central limit order book (CLOB) matches buyers and sellers through resting limit orders ranked by price-time priority. An automated market maker (AMM) replaces the order book with liquidity pools and a deterministic pricing formula like x*y=k. CLOBs deliver better price discovery and capital efficiency for liquid markets, while AMMs make long-tail asset bootstrapping trivial.

Q Q Q How can the order book mislead beginners?

Visible size can vanish in milliseconds through cancellation. Iceberg and hidden orders are invisible in public depth. Spoofers manufacture fake walls to bait retail flow. Imbalance can be deliberately engineered. The fix is to weigh executed trades higher than resting orders and treat the book as one input among several rather than a guaranteed map.

Conclusion: the order book is your trading microscope

The order book is the most informative single view in any trading interface, and learning to read it well separates serious traders from button mashers. Every concept in this guide, bids and asks, spread, depth, imbalance, makers and takers, iceberg orders, spoofing patterns, CLOB versus AMM tradeoffs, applies across every major venue from Binance and Coinbase to Hyperliquid and dYdX v4.

What changed in 2026 is the breadth of where these skills matter. Perpetual DEXs running on chain CLOBs now process billions in daily volume, and the next generation of crypto traders will spend as much time in Hyperliquid books as in Binance books. The fundamentals are the same, but the surface area for applying them has expanded dramatically.

Start by paper trading on a single venue, watching a single pair for a week, and forcing yourself to predict the next price move based on book and tape before checking what actually happens. That deliberate practice loop is how every professional trader internalized order book reading, and it is still the most reliable path in 2026. Combine it with our broader tutorial library, including the Hyperliquid trading guide and the slippage guide, and you will have a complete framework for executing trades with intention rather than guesswork.

Related DEXTools tutorials

Related Guides

- Hyperliquid L1 Explained: HyperBFT, On-Chain Order Book and Market Design (2026)

- AMM vs Order Book DEXs: Crypto Trade Dynamics

- What Is BOME (Book of Meme)? Solana Darkfarms Memecoin Guide 2026

- What Is Order Flow in Crypto Trading? How to Read Buying and Selling Pressure (2026)

- What Is an Iceberg Order in Crypto Trading? (2026)