Loan Origination vs Outstanding Debt: Which Shows Real Lending Growth?

— By Whatsertrade in Tutorials

DeFi lending protocols are often analyzed through TVL, utilization and borrow rates. These metrics are useful, but they do not always show how lending demand is

DeFi lending protocols are often analyzed through TVL, utilization and borrow rates. These metrics are useful, but they do not always show how lending demand is evolving.

Two other important metrics are loan origination and outstanding debt.

Loan origination shows how much new borrowing is being created. Outstanding debt shows how much borrowing remains active.

They may sound similar, but they tell different stories.

Understanding loan origination vs outstanding debt can help traders analyze real lending growth more clearly.

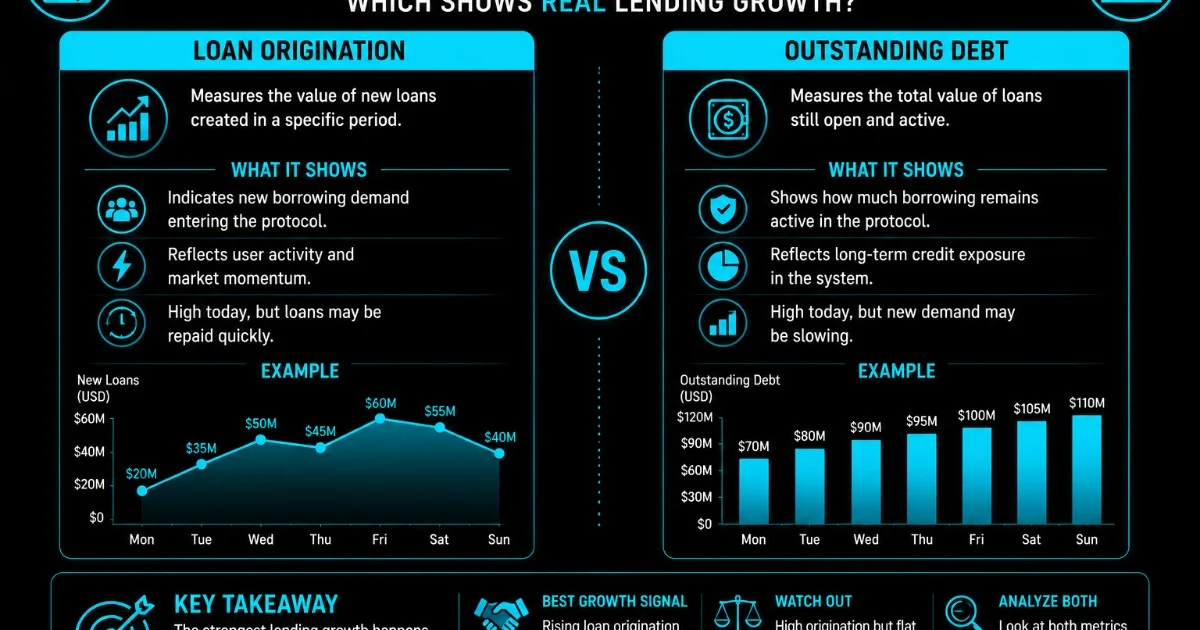

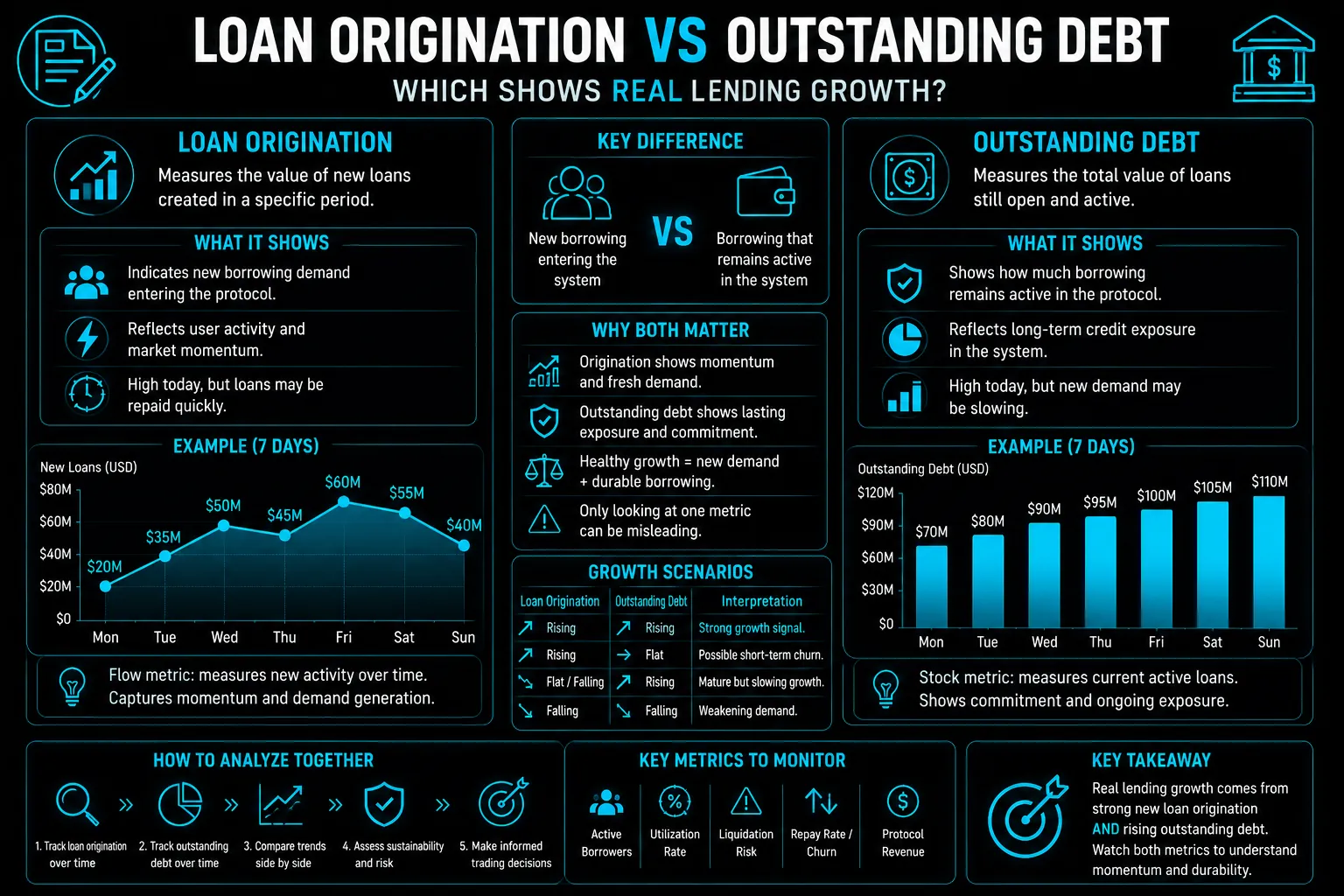

What Is Loan Origination?

Loan origination measures the value of new loans opened during a specific period.

In DeFi, this can mean new borrow positions created by users who deposit collateral and borrow assets.

High loan origination can show fresh borrowing demand. It may indicate that users are actively seeking capital for trading, leverage, liquidity, hedging or DeFi strategies.

Loan origination is a flow metric because it tracks new activity over time.

What Is Outstanding Debt?

Outstanding debt measures the total amount of debt still active in the protocol.

If users borrow assets and keep their loans open, outstanding debt remains. If users repay loans, outstanding debt decreases.

Outstanding debt is a stock metric because it shows the current level of active borrowing.

This metric helps traders understand how much credit exposure remains inside the protocol.

Loan Origination vs Outstanding Debt: The Key Difference

The key difference is new borrowing vs active borrowing.

Loan origination shows how much new debt is being created.

Outstanding debt shows how much debt remains open.

A protocol can have high loan origination but stable outstanding debt if users borrow and repay quickly. A protocol can have low loan origination but high outstanding debt if existing borrowers keep positions open.

Both metrics matter for understanding lending momentum.

Why Loan Origination Matters

Loan origination shows whether borrowers are actively entering the market.

If new loans are increasing, the protocol may be gaining demand. Users may be finding opportunities, using leverage or relying on the protocol for liquidity.

Rising origination can be a sign of momentum, especially when it comes from many borrowers and multiple assets.

However, new borrowing is not always sustainable.

If users borrow only for short term farming or speculative loops, origination may fall when incentives decline.

Why Outstanding Debt Matters

Outstanding debt shows how much borrowing remains active.

A protocol with growing outstanding debt may have users who continue to rely on its lending markets. This can support ongoing interest revenue and deeper credit activity.

Outstanding debt can also reveal protocol risk.

If debt grows too quickly or becomes concentrated in risky collateral, the protocol may face higher liquidation risk.

Strong outstanding debt is positive only when it is supported by healthy collateral, liquidity and risk parameters.

When High Loan Origination Can Mislead

High loan origination can look bullish, but it may hide short term churn.

Users may open loans for a brief period and repay quickly. This can create strong origination numbers without building durable lending demand.

Loan origination may also spike during incentive campaigns, airdrop farming, leverage trends or market volatility.

If outstanding debt does not grow alongside origination, traders should ask whether demand is temporary.

When High Outstanding Debt Can Mislead

High outstanding debt can also be misleading.

A protocol may have large active loans, but if new loan origination is slowing, growth may be weakening.

Outstanding debt may also be concentrated in a few whale positions. If those borrowers repay or get liquidated, the protocol can lose activity quickly.

Traders should analyze debt quality, not only debt size.

Four Lending Growth Scenarios

High Origination and Rising Outstanding Debt

This is usually a strong growth signal. New borrowers are entering, and debt remains active.

If collateral quality is strong, this can suggest healthy lending momentum.

High Origination and Flat Outstanding Debt

This may suggest borrowing churn. Users are opening loans but repaying quickly.

This can still generate fees, but it may not show durable demand.

Low Origination and High Outstanding Debt

This may suggest mature but slowing lending activity.

Existing borrowers remain, but fewer new borrowers are entering.

Low Origination and Falling Outstanding Debt

This can suggest weakening demand.

Borrowers are repaying or leaving, and fewer new loans are being created.

Why This Matters for DeFi Protocols

Lending protocols need both new borrowers and durable debt.

Loan origination shows whether the protocol attracts fresh demand. Outstanding debt shows whether borrowing activity remains in the system.

A healthy protocol should not rely only on one.

If new loans rise but borrowers leave quickly, growth may be shallow. If outstanding debt is high but origination slows, future growth may be limited.

What Traders Should Analyze

Before judging lending growth, traders should ask:

Are new loans increasing?

Is outstanding debt growing too?

Are users repaying quickly?

Is borrowing demand spread across assets?

Are whales driving most new loans?

Is debt backed by liquid collateral?

Are rates stable?

Is growth organic or incentive driven?

Are liquidations rising with debt?

These questions help traders separate durable lending growth from short term activity.

Why This Matters for Tokenholders

Lending protocol tokens often depend on narratives around usage, revenue and risk.

If loan origination and outstanding debt both grow in a healthy way, token sentiment may improve. If growth is driven by temporary borrowing or risky debt, the token may face greater volatility.

Tokenholders should care not only about how much borrowing exists, but also whether borrowing is sustainable.

Good lending growth is balanced, diversified and supported by sound collateral.

How DEXTools Can Help

DEXTools can help traders review how lending protocol tokens react to changes in borrowing activity. Price action, liquidity, volume and transaction flow can reveal whether the market believes the lending growth story.

If loan activity looks strong but token liquidity is weak, risk remains.

Combining protocol metrics with live market data gives traders a better view.

Final Thoughts

Loan origination and outstanding debt are both important for analyzing DeFi lending growth.

Loan origination shows new borrowing demand. Outstanding debt shows active borrowing exposure.

The strongest lending protocols usually show healthy new loan creation, durable outstanding debt, diversified borrowers and controlled risk.

For traders, the key is not just whether borrowing is happening. The key is whether borrowing is growing in a sustainable way.

In DeFi lending, new loans show momentum. Outstanding debt shows commitment.

How to Bridge Crypto Between Chains: Complete Cross-Chain Tutorial 2026 How to Use 1inch for Swaps: Classic, Fusion and Limit Orders (2026) OKX Web3 Wallet Tutorial 2026: Multi-Chain Setup GuideThe Velocity of Capital: Beyond Static Debt

While outstanding debt provides a snapshot of current capital deployment, and origination illuminates fresh demand, neither metric fully captures the *velocity* of capital within a lending protocol. Capital velocity, in this context, refers to how frequently borrowed funds are repaid and subsequently re-lent. A high velocity suggests efficient capital cycling and robust market activity, even if outstanding debt remains relatively stable. Conversely, low velocity might indicate stagnant capital, where loans are long-term and infrequently revolved, regardless of high origination numbers.

Understanding capital velocity is crucial for assessing a protocol's long-term health and its ability to weather market shifts. Protocols with high velocity are often more resilient, as they demonstrate a continuous feedback loop of demand and supply. This dynamic interplay can lead to more stable interest rates and a more efficient allocation of capital over time, benefiting both lenders and borrowers.

Implications for Protocol Health and Risk

- High velocity can signal a vibrant and active user base, with frequent borrower turnover.

- It can also indicate shorter loan durations, potentially reducing long-term exposure for lenders.

- Low velocity might suggest a greater proportion of "sticky" capital, locked in long-term positions.

- Protocols with low velocity could be more susceptible to liquidity crunches if a large portion of debt matures simultaneously.

- Analyzing repayment patterns and average loan durations can offer insights into capital velocity.

Related Guides

- Fee Payer Growth vs Transaction Count: Which Better Shows Real Network Adoption?

- Liquidation Volume vs Bad Debt in DeFi Lending

- Token Transfer Velocity vs Holder Retention: What Shows Real Conviction?

- Settlement Volume vs Transfer Count: Which Better Shows Real On Chain Value Movement?

- Fee Revenue per Active Wallet vs Total Fees: Which Shows Real dApp Monetization?

Frequently Asked Questions

What is loan origination in DeFi lending?

Loan origination is the volume of new loans created over a period in a lending protocol. It reflects fresh borrowing demand rather than the total amount currently owed.

What is outstanding debt in a lending protocol?

Outstanding debt is the total amount currently borrowed and not yet repaid across the protocol. It shows the current size of the loan book at a point in time.

How do origination and outstanding debt differ?

Origination measures the flow of new lending activity, while outstanding debt measures the existing stock of loans. A protocol can have high outstanding debt even if new origination has slowed.

Which metric shows real lending growth?

New loan origination often gives a clearer view of fresh demand and growth than outstanding debt alone, which can stay high from older loans. Looking at both together gives a fuller picture of lending health.