What Is Impermanent Loss in DeFi? Beginner LP Definition and Why It Happens (2026)

— By Tony Rabbit in Tutorials

Learn what impermanent loss is in DeFi, why LP positions diverge from simply holding, and the basic conditions that make the loss grow or shrink.

Intent check: This page owns the beginner definition of impermanent loss and the intuition behind it. If you want worked liquidity-pool examples, break-even framing, and the deeper trade-off math, read Impermanent Loss in DeFi Liquidity Pools.

Impermanent loss is the most quietly damaging concept in DeFi. It does not show up as a single liquidation candle. It does not crash the pool. It just slowly underperforms a passive hold while the headline APY dashboard keeps you smiling. Many liquidity providers only realize it exists after they withdraw and notice that their final balance, despite good fees and good emissions, is still worse than just keeping the two tokens in their wallet.

Quick answer: Impermanent loss in DeFi is the underperformance an AMM liquidity provider experiences when the prices of the two pooled assets diverge from their starting ratio. The pool rebalances automatically using its constant-product math, leaving the LP with more of the underperforming asset and less of the outperforming one. The loss only becomes "impermanent" if prices return to the original ratio. In most real-world farming, they do not, and the loss is realized at withdrawal.

- Impermanent loss is a paper loss until you withdraw. If prices return to the starting ratio, the pool math fully reverses, but most pairs never go back.

- The size of the loss scales with price divergence. Small moves create small losses. Large moves create surprisingly large ones.

- Stablecoin pairs minimize it, volatile pairs amplify it. Near-pegged pairs are gentle. Volatile or trending pairs can wipe out APY headlines.

- Fees and emissions can offset it. A pool with strong volume and well-priced rewards can still beat a passive hold over time.

- Concentrated liquidity changes the math. Tighter ranges generate higher fees but raise impermanent loss exposure when price exits the range.

What impermanent loss actually is

Impermanent loss is a comparison, not a fee. It compares the value of the LP position with the value of simply holding the same two tokens outside the pool. If the pool position ends up with less value than a passive hold of the original deposit, the difference is the impermanent loss. The label exists because, in theory, the loss disappears if prices return to the original ratio. In practice, that rarely happens within the holding period most farmers actually use.

The reason this happens is the AMM rebalancing mechanism. Most basic DEXs use a constant-product formula, written as x times y equals k. The pool maintains the equality between the product of token A and token B by adjusting the ratio whenever traders swap. As price moves on the open market, arbitrageurs trade against the pool until its internal price matches the market. The pool's reserves shift in response, and the LP ends up holding the rebalanced reserves.

The constant-product formula in plain English

Imagine a pool with 10 ETH and 30,000 USDC. The product is 300,000. If ETH price doubles on the open market to 6,000 USDC, arbitrageurs will buy ETH from the pool until the pool's internal price also reaches 6,000. After all that arbitrage, the pool will hold less ETH and more USDC, even though the total dollar value still tracks the new market price plus accumulated fees.

The LP's share of the pool now contains more USDC and less ETH than at deposit time. If the LP simply held 10 ETH and 30,000 USDC outside the pool, the rebalanced position is worth less than the passive hold. That gap is the impermanent loss. Fees and rewards earned during the period reduce or sometimes overcome that gap, but the gap itself is created mechanically by the math.

Why the loss is "impermanent"

The label exists because if the price of ETH drops back to 3,000 in this example, arbitrage runs in reverse, and the pool's reserves rebalance back toward the original 10 ETH and 30,000 USDC. The LP would then end up roughly where they started, plus accumulated fees and rewards. That is the theoretical scenario where the loss truly was "impermanent." It is also the reason the term is misleading. Most volatile pairs do not return to their original ratios, and most farmers withdraw long before that hypothetical reversion ever happens.

How big can impermanent loss actually get?

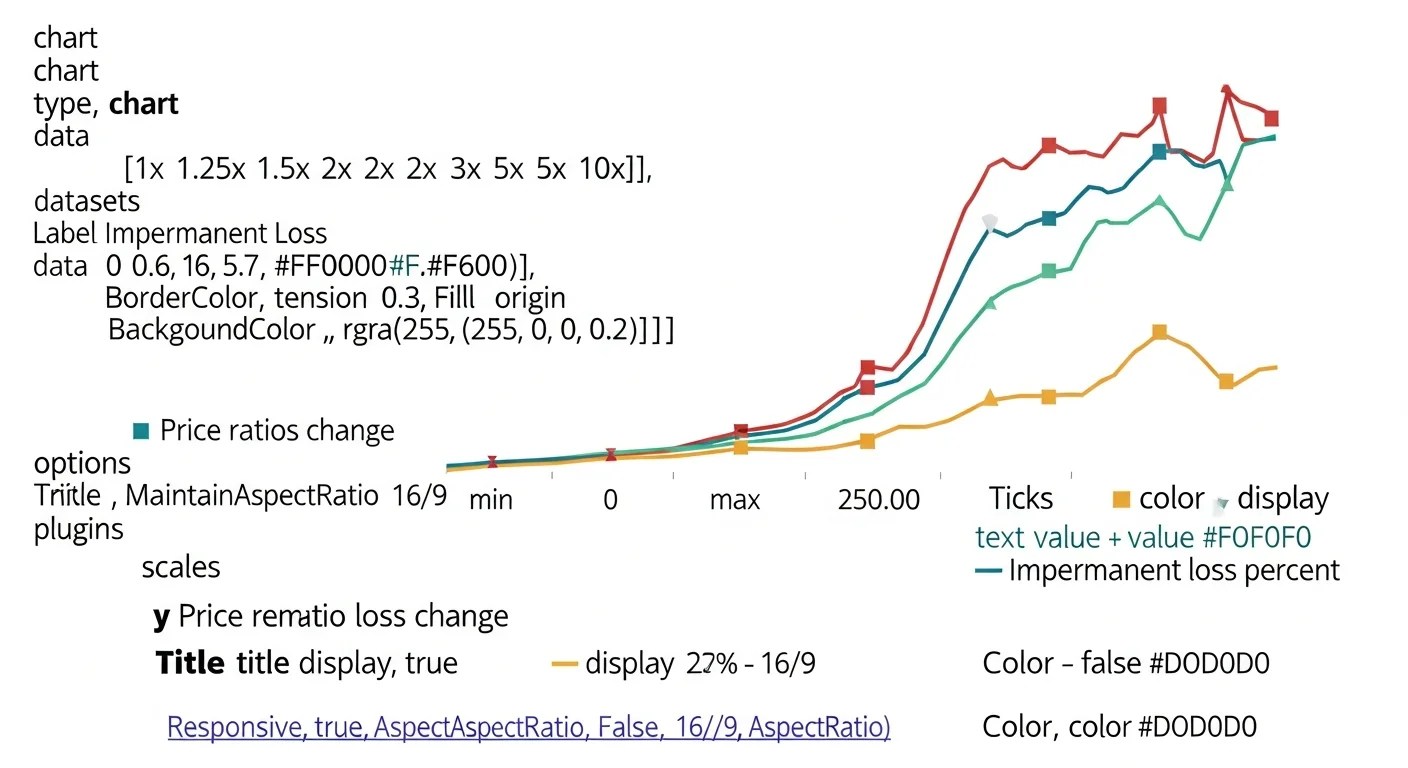

The famous reference table for a basic 50/50 constant-product pool is approximately this. Use it as a sense check, not as an exact rule for every protocol.

| Price change of one asset vs the other | Approximate impermanent loss | What this feels like |

|---|---|---|

| 1.25x | Around 0.6% | Barely noticeable, easily covered by fees |

| 1.5x | Around 2% | Visible but manageable on active pools |

| 2x | Around 5.7% | Real drag on returns even with strong APY |

| 3x | Around 13.4% | Most APY headlines now trail a passive hold |

| 5x | Around 25% | Major loss versus simply holding |

| 10x | Around 40% | Severe, hard for any APY to offset |

These numbers are symmetric. A 2x move up or a 2x move down produces roughly the same impermanent loss. Beginners often assume the pool only loses on big up moves of the volatile asset. The math does not care about direction. It only cares about how far the ratio has drifted from the deposit point.

When impermanent loss really hurts and when it does not

Impermanent loss is not a uniform danger. The same APY headline on two different pools can mean two completely different outcomes once you account for the underlying volatility profile.

Stablecoin pairs and pegged-asset pairs

Stablecoin-to-stablecoin pools are the gentlest case. As long as the pegs hold, the price ratio barely moves, and impermanent loss stays close to zero. The same is roughly true for pools between assets that are tightly correlated, such as ETH and a liquid staking version of ETH. The catch is that "as long as the pegs hold" hides serious tail risk. A depeg event can blow through years of accumulated fees in a few hours.

Volatile blue-chip pairs

Pairs like ETH paired with BTC, ETH paired with a top stablecoin, or BTC paired with a top stablecoin are the typical middle ground. Price divergence is normal but rarely extreme over short timeframes, which keeps impermanent loss in a manageable range as long as fees and rewards are real. Bull-market melt-ups and bear-market crashes are the moments where the math turns sharper.

Long-tail and meme coin pairs

Pools containing meme coins, micro-caps, or recent launches are where impermanent loss gets brutal. A token that runs 10x and then crashes 70 percent within the same farming period can leave LPs holding a bag of the depreciated asset, having "sold" the upside-trending token along the way through arbitrage. High emissions APYs on these pools often hide the fact that the realized PnL is deeply negative.

Paper loss versus realized loss

One of the most common framing errors is treating impermanent loss as already locked in just because the dashboard shows it. A paper impermanent loss is a snapshot of how the pool position currently compares with a passive hold. It can shrink or grow as prices move. It only becomes a realized loss when the LP actually withdraws.

This matters for two reasons. First, an LP who withdraws during a sharp move locks in worse math than if they had waited for prices to settle. Second, an LP who panics on a paper loss can end up converting a manageable drag into a hard-to-recover capital reduction. The decision to withdraw should be based on the same logic as any other position: thesis change, risk reassessment, or genuine liquidity need, not raw fear of a number on a dashboard.

How to limit impermanent loss in practice

You cannot eliminate impermanent loss on a volatile AMM pair, but you can keep it inside a tolerable band.

Pick correlated assets when possible

The simplest mitigation is to pair assets that tend to move together. Stablecoin-to-stablecoin pools, pegged-asset pools, and tightly correlated pairs like ETH paired with liquid-staked ETH dramatically reduce impermanent loss exposure. The tradeoff is lower APY, because lower volatility usually means lower swap volume and thinner emissions.

Choose pools with strong fee revenue

A pool with high real volume can offset meaningful impermanent loss through fees alone. Pools with paper-thin volume but loud emissions APYs are usually the worst case, because the rewards are inflationary and the impermanent loss is paid in real value.

Manage concentrated liquidity ranges actively

Concentrated liquidity DEXs let LPs concentrate capital inside a price range. That dramatically increases fee efficiency, but if price exits the range, the position becomes 100 percent of the worse-performing asset and impermanent loss becomes much sharper. Active range management, automation tools, or vault-style products can soften this, but none of them remove the underlying risk.

Right-size the position and accept the drag

The healthiest mental model is that impermanent loss is a cost of doing business, not a bug. If a position is sized so that even a worst-case impermanent loss does not break the broader portfolio, the trade is sustainable. If the same position would create real distress, it was sized wrong from day one.

Practical workflow for DEXTools and DeFi LPs

The cleanest workflow is to evaluate the pair, the protocol, and the volume profile before clicking deposit, not after the math turns ugly.

- Use DEXTools to confirm the pair has real volume and liquidity. An emissions APY on an empty pool is nearly always a trap.

- Estimate worst-case price divergence. Imagine a 2x or 3x move in the more volatile asset and confirm you can live with the resulting math.

- Check the source of yield. Real fees plus a rational emissions schedule beat huge inflation paid in a token already in downtrend.

- Plan your exit. Decide in advance what conditions would make you withdraw and reassess, instead of reacting to the dashboard.

If you also want to dive into surrounding topics, hand readers to yield farming, liquid staking, or protocol-owned liquidity instead of forcing all of DeFi into a single article.

Impermanent loss vs fees in one short comparison

| Force on LP returns | Direction | Main caution |

|---|---|---|

| Impermanent loss | Reduces returns relative to hodl when prices diverge | Symmetrical, hits up moves and down moves alike |

| Trading fees | Adds returns whenever volume runs through the pool | Can be small on quiet pools and great on busy ones |

| Token emissions | Adds nominal yield, but often inflationary | Paid in tokens that may lose value while you farm them |

Frequently asked questions

Q What causes impermanent loss in DeFi?

Impermanent loss is caused by AMM rebalancing as prices diverge. The pool's constant-product math forces the reserves to shift away from the original deposit ratio, leaving the LP with a worse position than simply holding both tokens outside the pool.

Q Can impermanent loss be avoided completely?

It cannot be eliminated on volatile pairs, but it can be minimized by choosing correlated or stable pairs, pools with strong fee revenue, and reasonable position sizes. Single-asset lending avoids it entirely because there is no pool ratio to drift.

Q Is impermanent loss real money?

It becomes real when you withdraw. Until then it is a paper underperformance versus a passive hold. If prices return to the deposit ratio before withdrawal, the loss disappears, but most pairs do not behave that way.

Q Does impermanent loss happen on stablecoin pools?

It is very small while pegs hold. Stablecoin-to-stablecoin pools and pegged-asset pools have minimal impermanent loss, but a depeg event can produce a sudden, severe shock that the math is unforgiving about.

Q How do I calculate impermanent loss?

Compare the current value of your LP share with the value of holding the original deposit outside the pool. The gap is the impermanent loss. Most DEX dashboards show this in real time, and standalone calculators exist for what-if scenarios.

Final takeaway: Impermanent loss is not a hidden trap, it is the price of using AMM pool math instead of holding tokens directly. Read the volatility profile, pick the right pair, weigh fees and emissions honestly, and treat impermanent loss as one cost in a real risk budget rather than a surprise at withdrawal.

Disclaimer: This guide is for educational purposes only and does not constitute investment, financial, legal, or trading advice. DeFi pool math is unforgiving, and APY headlines can hide real losses.

Related Guides

- Impermanent Loss in DeFi Liquidity Pools: Worked LP Math, Break-Even and Trade-Offs (2026)

- Liquidity Pool Economics: Fees, Slippage and Impermanent Loss

- Impermanent Loss Explained: Examples and How to Reduce It

- LP Lock Expiry Risk: What Happens When Token Liquidity Unlocks?

- Take Profit vs Stop Loss in Crypto: Key Differences, Trigger Logic and Fill Risk (2026)