Impermanent Loss Explained: Examples and How to Reduce It

— By AliceOnChain in Tutorials

Impermanent loss is one of the most critical structural risks faced by decentralized finance liquidity providers. This guide breaks down the mathematics behind asset divergence, analyzes a practical market scenario, and provides actionable risk-management strategies using advanced on-chain metrics to preserve your crypto capital.

Impermanent Loss Explained: Examples and How to Reduce It

Automated Market Makers (AMMs) revolutionized the decentralized finance (DeFi) ecosystem by allowing users to trade digital assets without relying on traditional centralized order books. At the core of this financial infrastructure are liquidity providers (LPs), who deposit pairs of tokens into smart contracts to facilitate decentralized trading. In return for keeping the markets fluid, these providers earn a proportional share of transaction fees. However, this model introduces a unique economic risk for any DeFi liquidity provider, making it essential to have impermanent loss explained through practical examples so market participants can learn how to protect their on-chain capital.

While liquidity provision offers a compelling mechanism for generating passive yield, failing to monitor changing asset ratios can severely impact your portfolio. For anyone navigating decentralized markets-whether capitalizing on volatile trading pools or seeking steady returns on established pairs-having impermanent loss explained alongside actionable risk parameters is the first step toward effective crypto risk management.

This guide provides an analytical breakdown of how these shifts occur, clear mathematical examples, and strategic methods to reduce impermanent loss using advanced on-chain analysis and tools available on platforms like DEXTools.

Understanding Impermanent Loss in DeFi

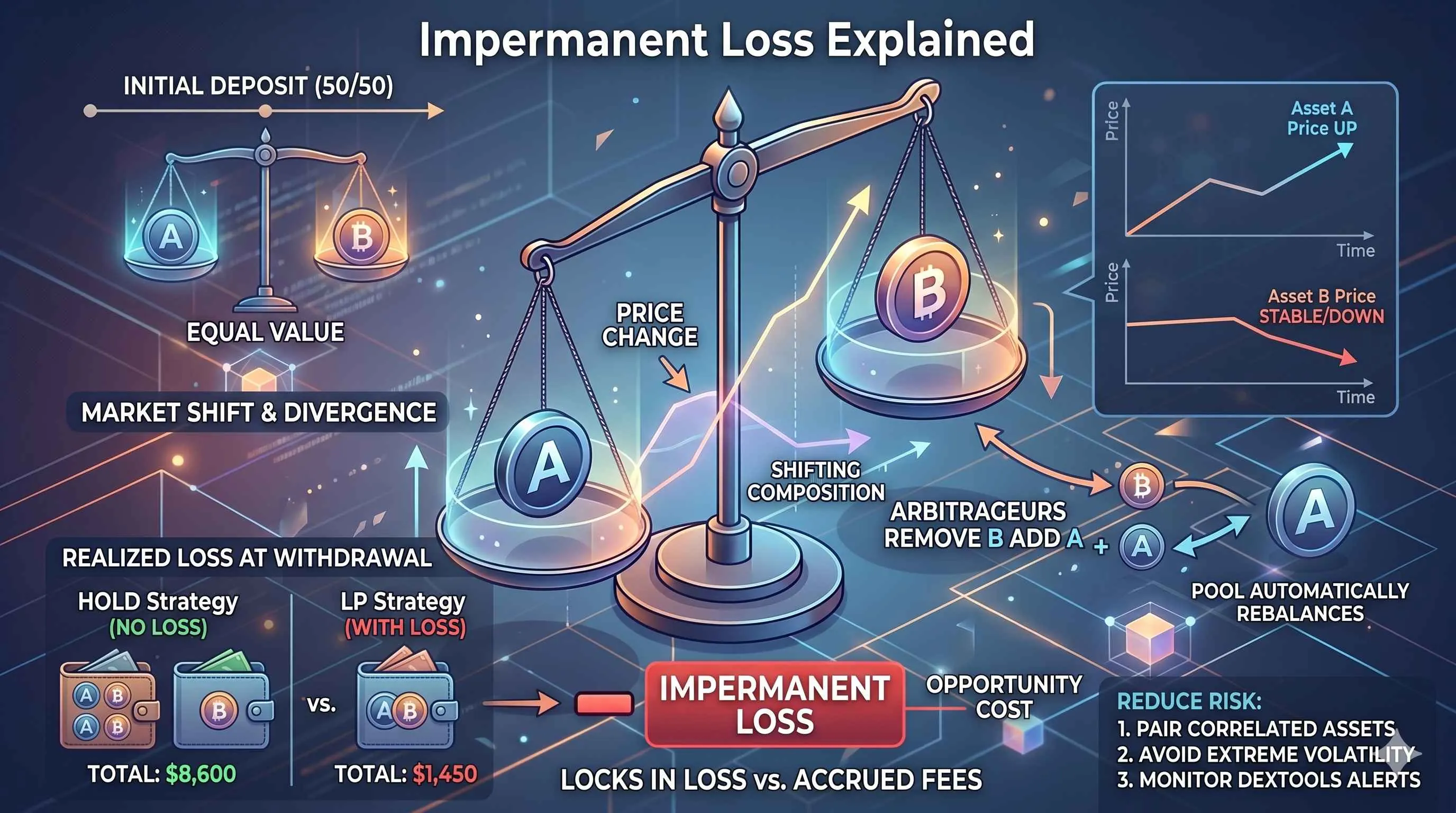

Impermanent loss occurs when a liquidity provider deposits a token pair into a liquidity pool, and the price ratio of those deposited assets changes relative to when they were first committed to the smart contract. When a price divergence happens, the mathematical formula governing standard constant product market makers ($x \times y = k$) automatically rebalances the pool to ensure both sides maintain equal dollar value.

Consequently, an LP’s share of the pool may contain more of the depreciating asset and less of the appreciating asset compared to simply holding the tokens outside the pool in a private wallet. To have impermanent loss explained simply: it represents the opportunity cost of providing liquidity versus holding the raw assets. The loss is termed "impermanent" because it only becomes permanent-or realized-the moment the liquidity provider withdraws their assets from the protocol. If the price ratio reverts to exactly what it was during the initial deposit, the loss disappears, leaving the provider with their original asset ratio plus accrued trading fees.

However, in fast-moving on-chain markets characterized by high volatility, price ratios rarely return to their exact entry points. For traders looking to reduce impermanent loss, treating this deficit as a structural cost of doing business in automated market makers is a more realistic framework than assuming a full price recovery.

Mathematical and Practical Examples of Impermanent Loss

To fully understand how these dynamics manifest during standard market cycles, let us look at a practical scenario where impermanent loss explained mathematically reveals the exact portfolio impact on an established pairing: Ethereum (ETH) and a dollar-pegged stablecoin (USDC).

The Initial Deposit

An investor wants to deposit assets into a standard 50/50 ETH/USDC liquidity pool.

Initial Asset Prices: 1 ETH = 4,000 USDC

LP Contribution: 1 ETH and 4,000 USDC

Total Value at Deposit: 8,000 USDC

At this stage, the constant product formula establishes a fixed relationship for this share of the pool. The asset ratio is balanced precisely at 50% value for each side.

The Market Shift

Over the subsequent weeks, positive market sentiment and an influx of buying volume drive the price of ETH up by 25%.

New Asset Price: 1 ETH = 5,000 USDC

Arbitrageurs immediately notice the price discrepancy between external exchanges and our decentralized liquidity pool. To profit from this imbalance, they swap USDC into the pool to buy underpriced ETH until the pool's internal price matches the external market price of 5,000 USDC.

The Realized Withdrawal

Because arbitrageurs have extracted ETH and added USDC, the internal composition of the LP’s pool share has shifted. If the provider decides to withdraw their liquidity at this exact moment, they will receive:

Withdrawn Assets: Approximately 0.894 ETH and 4,472 USDC

Total Portfolio Value at Withdrawal: 8,944 USDC

Calculating the Opportunity Cost

To measure the exact impact of this divergence, we compare the total portfolio value at withdrawal against the value of the same assets if the provider had simply held them in a cold wallet.

Value if Held (Buy-and-Hold Strategy): 1 ETH ($5,000) + 4,000 USDC = 9,000 USDC

Value if Provided Liquidity: 8,944 USDC

Net Loss Relative to Holding: 9,000 USDC - 8,944 USDC = 56 USDC (approximately 0.62%)

In this scenario, the liquidity provider still made a profit of 944 USDC due to the broad upward movement of the market. However, they underperformed a simple buy-and-hold strategy by 56 USDC. For the position to be truly profitable, the accumulated trading fees earned by facilitating swaps in the pool must exceed this 56 USDC threshold. Having this specific version of impermanent loss explained shows that overall market profitability does not mean your liquidity position outperformed a simple hold strategy.

Key Drivers of Impermanent Loss on-Chain

This phenomenon is not a static metric; its severity correlates directly with several on-chain factors that dictate how asset prices behave within automated market makers.

Asset Volatility and Divergence

The primary catalyst for asset divergence is how far apart the two assets move from their initial price ratio. It does not matter whether the price of one asset goes up or down; any significant shift accelerates the divergence. A sharp rally in one token or a catastrophic drop in another increases the structural deficit exponentially, making proper crypto risk management critical.

Liquidity Pool Composition

Standard pools require a 50/50 value split, which maximizes exposure to divergence. However, modern DeFi protocols feature weighted pools (such as 80/20 splits) or concentrated liquidity positions. Concentrated liquidity allows providers to bound their capital within specific price ranges. While this mechanism amplifies fee generation within that specific band, it also vastly accelerates potential divergence if the market price breaks out of the chosen boundaries, leaving the provider entirely in the depreciated asset.

Fee Volume vs. Divergence Speed

Liquidity provision is fundamentally a race between fee accumulation and price divergence. In highly utilized pools with substantial trading volume, the accrued transaction fees can easily outpace small or moderate losses. Conversely, if a token pair experiences low trading volume but high price volatility, the fees generated will fail to reduce impermanent loss, resulting in a net negative return for the provider upon withdrawal.

How to Reduce and Manage Impermanent Loss

While divergence risks cannot be completely eliminated in standard AMMs, sophisticated on-chain traders employ systematic crypto risk management strategies to minimize their exposure.

1. Select Low-Divergence Asset Pairs

The most direct way to reduce impermanent loss is to provide liquidity to asset pairs that inherently move in tandem or maintain stable values.

Stablecoin Pairs: Supplying liquidity to pairs like USDC/USDT yields virtually zero divergence risk because the asset prices are pegged to the same underlying currency. The primary risk here is the systemic de-pegging of one of the stablecoins.

Correlated Assets: Pairs such as wrapped ETH (WETH) against liquid staking derivatives like stETH exhibit high price correlation. Because their price ratio remains relatively constant, the structural deficit remains minimal, allowing providers to safely compound trading fees.

2. Analyze Volatility and Trends on DEXTools

Before committing capital to an LP pool, assessing the underlying asset's price action and historical market behavior is critical. Using DEXTools charts, traders can evaluate standard technical indicators to determine whether an asset is entering a period of consolidation or extreme expansion.

Monitoring structural support and resistance levels helps identify whether a token pair is trading within a reliable range. If an asset shows a stark RSI divergence on daily or weekly charts, it often signals an impending trend reversal or breakout. Providing liquidity right before a major technical breakout increases the probability of severe asset divergence, thereby increasing your risk. Conversely, entering a pool during a well-defined consolidation phase is an effective way to reduce impermanent loss during the duration of your deposit.

3. Track Liquidity and Smart Money Activity

Understanding the depth and distribution of a pool provides vital context on how resilient a pair is to sudden price swings.

On-Chain Liquidity Tracking: Utilizing the pair explorer on DEXTools allows users to observe real-time liquidity changes. Deep liquidity pools require significantly more capital to shift the asset price ratio, making them less susceptible to erratic, short-term price spikes caused by individual large orders.

Whale Activity and Distribution: Examining holder analysis tools and integrations like Bubblemaps helps identify wallet clusters. If a single whale or a small group of interconnected wallets holds a massive percentage of a token's circulating supply, the pool is at high risk of sudden, unidirectional price shifts. Monitoring top traders and whale activity can signal whether a pool's volume is driven by sustainable retail interest or speculative, highly concentrated trading that could leave a DeFi liquidity provider holding the depreciated asset.

4. Utilize Proactive Risk Tools

Active management is essential when dealing with volatile on-chain pairs. Implementing precise price alerts on DEXTools allows liquidity providers to monitor critical thresholds. If a volatile token approaches a major resistance level or a key structural breakdown point, a configured price alert gives the provider an early warning to withdraw their liquidity from the pool before the price ratio diverges too aggressively, effectively locking in fees and acting to reduce impermanent loss.

Evaluating the Trade-Off: Is Liquidity Provision Worth It?

Navigating decentralized liquidity pools requires a balanced view of risk and reward. With impermanent loss explained through historical market behaviors, it becomes clear that liquidity provision should not be viewed as a passive investment, but rather as an active yield strategy that requires ongoing monitoring of market sentiment.

When selecting pools, a high Annual Percentage Yield (APY) is often a reflection of the market pricing in extreme volatility and subsequent divergence risk. Capital allocators must determine whether the projected transaction fee volume over a specific horizon will sufficiently cover the mathematical drag of asset divergence. By combining strict risk parameters, technical chart analysis, and real-time on-chain liquidity tracking, market participants can successfully navigate the complexities of automated market structures while preserving their underlying crypto capital.

- How to Bridge Crypto Between Chains: Complete Cross-Chain Tutorial 2026

- How to Use 1inch for Swaps: Classic, Fusion and Limit Orders (2026)

- How to Use OKX Web3 Wallet: Multi-Chain DeFi Hub Guide (2026)

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.

Related Guides

- What Is Impermanent Loss in DeFi? Beginner LP Definition and Why It Happens (2026)

- Impermanent Loss in DeFi Liquidity Pools: Worked LP Math, Break-Even and Trade-Offs (2026)

- Liquidity Pool Economics: Fees, Slippage and Impermanent Loss

- How to Set Stop-Loss and Take-Profit in Crypto: Entry, Risk and R:R Setup (2026)

- MEV Risks for Crypto Traders: How to Reduce Losses

Frequently Asked Questions

What is impermanent loss?

Impermanent loss is the difference in value a liquidity provider can experience compared with simply holding the assets, caused by the prices of the pooled assets diverging. It becomes a realized loss only when you withdraw while that divergence remains.

Why does impermanent loss happen?

It happens because an automated market maker rebalances the pool as prices change, leaving providers with relatively more of the asset that fell and less of the one that rose. The larger the price divergence, the larger the potential impermanent loss.

Can trading fees offset impermanent loss?

Yes, the fees earned from providing liquidity can partly or fully offset impermanent loss depending on trading volume and price movement. Whether fees outweigh the loss varies by pool and market conditions.

How can liquidity providers reduce impermanent loss?

Providing liquidity for assets that tend to move together, such as similarly priced stable assets, can reduce divergence and therefore impermanent loss. Understanding the pool and price behavior before depositing also helps manage the risk.