NFT Lending Explained: How to Borrow Against Your NFTs

Digital collectibles no longer need to sit as dead capital inside web3 wallets. We break down how NFT-Fi credit architectures generate instant liquidity loans using smart contracts.

NFT Lending: the Financialization of Digital Property

- NFT Lending (or NFT-Fi) completely tears down this barrier. By combining immutable smart contracts with real-time price feeds, NFT-Fi protocols allow collectors to use their digital property as collateral to secure instant, permissionless loans in liquid assets like ETH or stablecoins. This guide explores the architectural differences between peer-to-peer and peer-to-pool lending models, analyzes dominant platforms like NFTfi, Blend, and BendDAO, and details the liquidation mechanics that manage risk across the space.

- For years, the primary structural critique of non-fungible tokens (NFTs) was their extreme capital inefficiency. Unlike highly liquid fungible tokens that can be instantly swapped or deployed into yield-bearing decentralized finance (DeFi) primitives, NFTs behaved like physical fine art. To unlock the equity trapped inside an expensive digital collectible, a holder had only one real choice: sell the asset entirely, forfeiting any future upside.

1. Peer-to-Peer (P2P) Lending: Custom Terms and Direct Matches

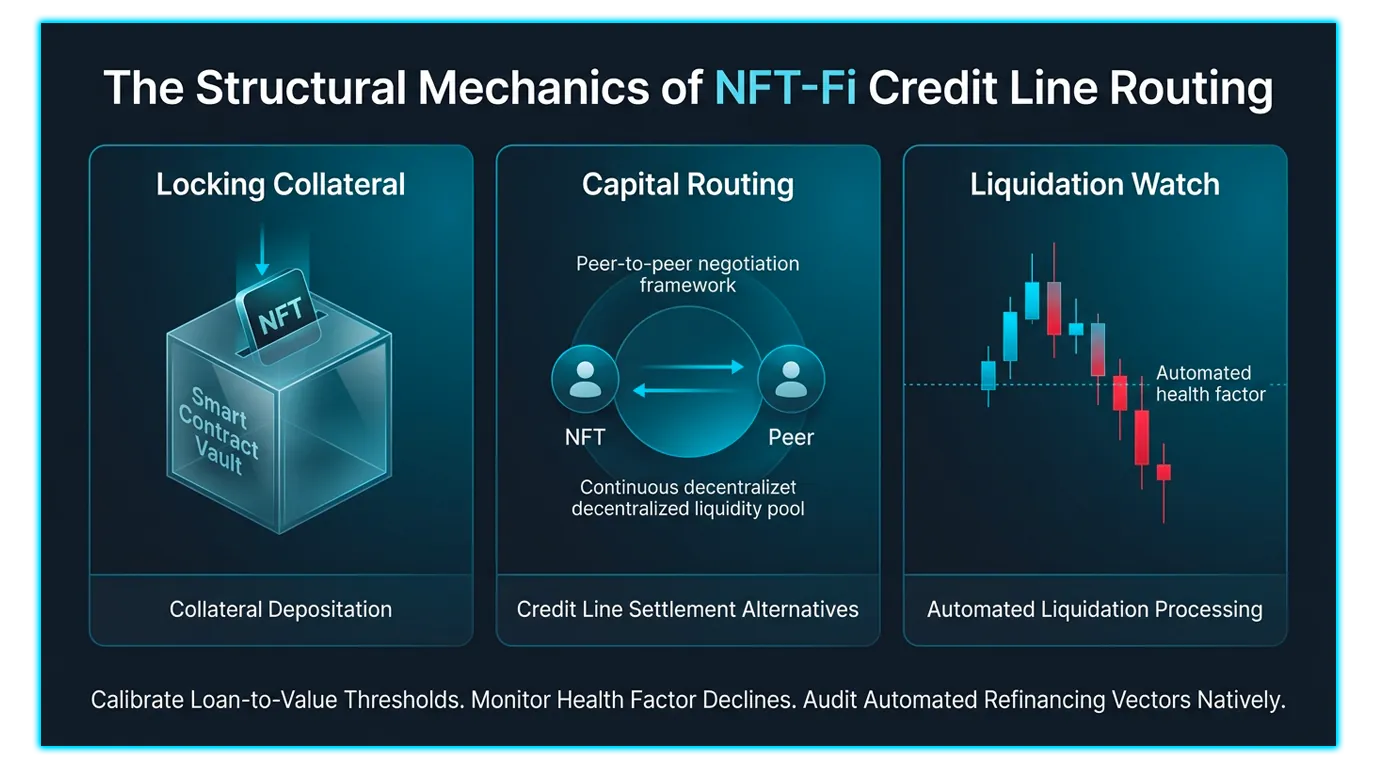

The earliest form of decentralized luxury credit infrastructure operates on a Peer-to-Peer (P2P) framework. In this model, the protocol acts as a trustless matchmaking escrow, allowing individual borrowers and lenders to negotiate loan parameters directly.

Traditional P2P: NFTfi

- On platforms like NFTfi, the NFT lending process begins when a borrower lists their asset as collateral and proposes preferred loan terms. Lenders browse the marketplace and submit custom counter-offers, defining the exact loan amount, duration (e.g., 30, 60, or 90 days), and the annualized percentage rate (APR).

- Once both parties sign off, the NFT is locked inside a secure cryptographic escrow contract. The borrower receives the liquidity immediately. If the borrower repays the principal plus accrued interest before the fixed deadline, the smart contract unlocks and returns the NFT, successfully completing the NFT lending cycle.

Perpetual P2P: Blur’s Blend

Blend completely overhauled the P2P space by introducing perpetual lending with no fixed expiry dates.

Instead of forcing a fixed repayment window, a Blend loan continues indefinitely until one of two triggers occurs:

The Borrower Repays: The borrower chooses to close the debt line by paying off the principal.

The Lender Calls the Loan: If a lender wants their ETH back, they trigger an automated auction. The protocol gives the system 24 hours to find a replacement lender willing to take over the debt at a competitive interest rate. If no new lender steps in, the loan is liquidated.

2. Peer-to-Pool NFT Lending: Instant Liquidity Pools

When a collector requires capital instantly and cannot afford to wait days for a peer to review their listing, Peer-to-Pool architectures provide a high-speed alternative.

Protocols like BendDAO operate much like Aave or Compound, but use NFTs as the underlying collateral layer.

The Sourcing Engine: Liquid providers deposit native crypto assets (like ETH) into a massive, unified lending pool to earn passive interest yields.

Instant Borrowing: Borrowers deposit a supported "blue-chip" NFT directly into the pool vault. Backed by decentralized pricing oracles (like Chainlink) that track the aggregate market floor price, the smart contract instantly calculates the asset's maximum borrowing capacity, distributing the capital to the user within a single block confirmation.

3. Risk Protocols: Navigating Liquidations

Borrowing liquidity against highly volatile digital assets requires strict risk management parameters to prevent systemic bad debt from breaking the underlying protocol vaults.

Loan-to-Value (LTV) and Health Factors

Every loan is strictly bound by a maximum Loan-to-Value (LTV) ratio, which usually caps maximum borrowing lines at 30% to 50% of the collection's verified floor price.

In peer-to-pool networks, the safety of a loan is tracked by a real-time Health Factor. If a collection's floor price drops rapidly, the debt value rises relative to the collateral value. If the calculated Health Factor drops below a critical threshold (typically 1.0), the smart contract automatically initiates a liquidation protocol.

The Execution Divide

The penalty for a failing loan varies drastically based on the platform's architectural model:

In Traditional P2P (NFTfi): If the fixed expiration clock hits zero and the borrower hasn't paid, the contract triggers a default. The underlying NFT is instantly transferred directly to the lender's wallet box, closing the loop with zero auction delays.

In Peer-to-Pool (BendDAO): The protocol opens a 24-hour liquidation auction grid. The system gives the original borrower a final grace period to repay the debt along with a nominal liquidation fee. If they fail to clear the debt, the NFT is sold to the highest bidder on the open market, and the proceeds are routed back to reimburse the global lending pool.

NFT-Fi Architecture Comparison Matrix

| Model | Matching | Liquidation | Key Example |

| P2P | Direct user | Instant/Default | NFTfi |

| Perp P2P | Automated | 24h Refinance | Blend |

| P2Pool | Instant pool | Health auction | BendDAO |

Analyzing NFT Governance Tokens via DEXTools Telemetry

- Analyzing the capital trends and pricing fluctuations within the NFT-Fi ecosystem requires advanced on-chain data telemetry. Accessing deep decentralized data grids via platforms like DEXTools arms market participants with a premier command deck to keep tabs on real-time token shifts, verify trading pool densities, and review contract logic across multiple public ledgers.

- By checking the telemetry inside the Pair Explorer, tracking emerging project launches via the Live New Pairs feed, or studying market sentiment via the Trade Story or Top Traders dashboards, analysts can break down regional volume movements. Furthermore, observing large institutional reallocations inside the Big Swap Explorer allows traders to audit automated contract safety grades before committing funds, keeping your hardened hardware storage setups interfacing exclusively with legitimate and secure market hubs.

You can access DEXTools here and start trading today!

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.

Deeper Dive: Underwriting and Risk Mitigation in NFT Lending

While the promise of instant liquidity for your digital assets is compelling, it is crucial to understand the underlying mechanisms that enable these loans and the risks involved. Unlike traditional asset-backed lending where physical collateral can be easily appraised and liquidated, NFTs present unique challenges due to their illiquidity, price volatility, and the subjective nature of their value. NFT lending platforms employ sophisticated underwriting models to assess risk and protect both lenders and borrowers.

The core of NFT lending's risk mitigation lies in its overcollateralized nature and the automated enforcement of smart contracts. Most protocols require the value of the NFT collateral to significantly exceed the loan amount, providing a buffer against price drops. If the NFT's floor price falls below a predetermined liquidation threshold, the smart contract automatically triggers the sale of the NFT to repay the loan, protecting the lender. This automated process removes the need for human intermediaries and reduces counterparty risk.

Understanding Liquidation Mechanics

- Loan-to-Value (LTV) Ratio: This defines the maximum loan amount you can receive relative to the appraised value of your NFT. A lower LTV means less risk for the lender.

- Liquidation Price: The specific price point at which your collateral NFT will be automatically sold to cover the outstanding loan.

- Grace Period: Some platforms offer a short grace period after the liquidation price is hit, allowing borrowers to top up collateral or repay the loan.

- Oracle Integration: Decentralized oracles are used to feed real-time floor price data for various NFT collections to the smart contracts, enabling accurate liquidation triggers.

- Whitelisted Collections: Many platforms only accept NFTs from established, high-liquidity collections to minimize price manipulation risk and ensure potential buyers exist during liquidation.

Despite these safeguards, borrowers must remain vigilant regarding market fluctuations. A sudden downturn in the NFT market can quickly push an asset toward its liquidation price, potentially resulting in the loss of your valuable digital collectible. Understanding these mechanisms is paramount for responsible participation in the NFT lending ecosystem.

Related Guides

- JustLend Tutorial: Lend and Borrow on TRON 2026

- How to Use Aave: Deposit, Borrow, Repay and Manage Health Factor (2026)

- Borrow Cap vs Supply Cap: How Lending Limits Protect DeFi Markets

- What are Ordinals? Bitcoin NFTs Explained

- TON NFTs and Telegram Gifts: Complete Guide (2026)

Frequently Asked Questions

What is NFT lending?

NFT lending lets owners use their non fungible tokens as collateral to borrow crypto without selling them. It turns otherwise idle digital assets into a source of liquidity.

How does borrowing against an NFT work?

A borrower locks an NFT as collateral and receives a loan, usually for a portion of the asset's estimated value. If the loan is not repaid under the agreed terms, the lender can claim the NFT.

What are the risks of NFT lending?

Key risks include losing the NFT if you default, volatile and uncertain NFT valuations, and smart contract vulnerabilities. Sudden drops in floor prices can also trigger liquidation.

Why use NFT lending instead of selling?

Borrowing against an NFT can unlock liquidity while letting the owner keep long term exposure to the asset. This appeals to holders who need funds but do not want to give up their NFTs.