What Is Funding Rate in Crypto? Complete Guide (2026)

— By Tony Rabbit in Tutorials

Learn how crypto funding rates work in perpetual futures, the 8-hour settlement cycle, basis trade APRs, and how to read funding extremes in 2026.

If you have ever opened a perpetual futures market and seen a tiny number like +0.0100% ticking next to a countdown timer, you have already met the funding rate. In 2026, with perpetual futures now responsible for the majority of crypto trading volume across both centralized exchanges (Binance, Bybit, OKX) and on-chain venues (Hyperliquid, dYdX v4, Vertex), the funding rate has become the single most quoted sentiment indicator in the derivatives market. Yet most traders still do not understand what it actually does or how to read it correctly.

The funding rate is a periodic payment exchanged between long and short perpetual futures traders that keeps the perpetual contract price tethered to the underlying spot price. It is not a fee paid to the exchange. It is a transfer between the two sides of the order book, and the exchange simply enforces the schedule. Positive funding means longs pay shorts. Negative funding means shorts pay longs. The rate adjusts dynamically based on how far the perpetual price drifts from spot.

This guide breaks down the mechanism, the formula, the standard 8-hour funding schedule used by most exchanges, the contrarian signals that funding extremes generate, the cash-and-carry basis trade that institutions use to harvest billions in funding annually, the difference between perp DEX funding and CEX funding, and the funding history of major 2024 to 2026 events including the spot ETF launches, the Bitcoin halving, and the Hyperliquid airdrop. By the end you will know how to read funding like a derivatives desk, not like a Twitter trader.

What Is Funding Rate in Crypto?

Funding rate is a periodic payment exchanged between long and short perpetual futures traders that keeps the perpetual contract price tethered to spot. When the perpetual trades above spot, funding turns positive and longs pay shorts. When the perpetual trades below spot, funding turns negative and shorts pay longs. The exchange never takes the funding payment, it only enforces the transfer between traders.

This mechanism replaces the natural expiry-driven convergence that traditional futures contracts use. Quarterly futures on CME or on the old crypto exchanges (BitMEX quarterly, Binance COIN-M quarterly) have a settlement date that forces the contract price to meet spot. Perpetuals have no expiry, so the funding rate does the same job by economic pressure rather than by calendar deadline.

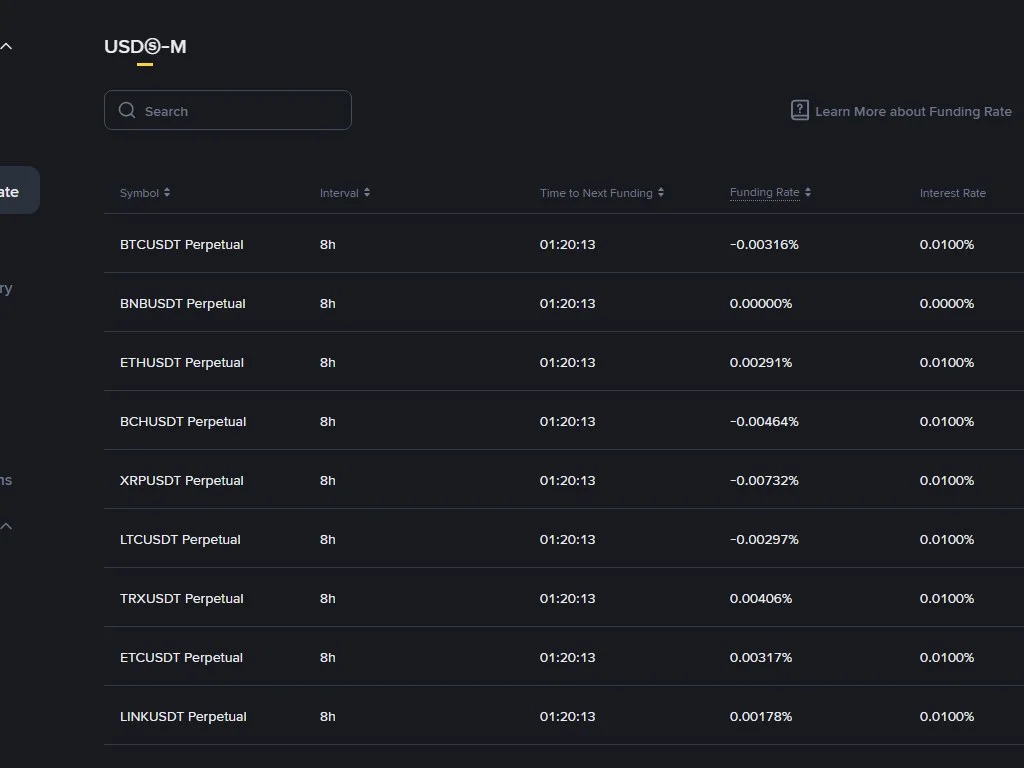

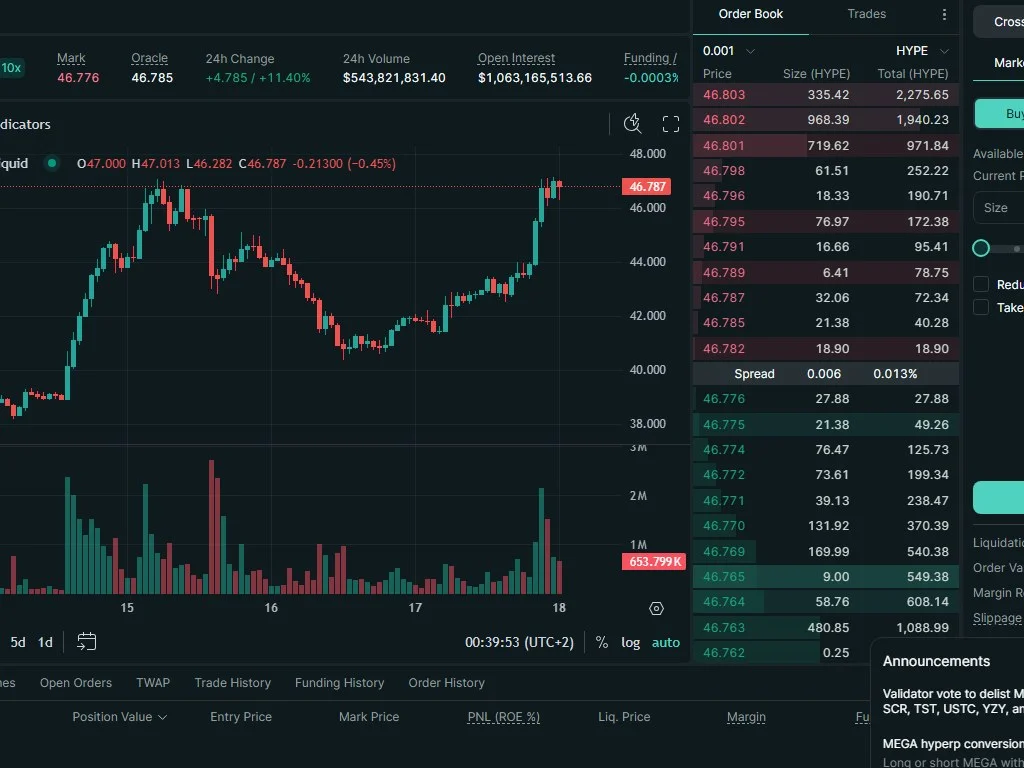

The standard funding interval on Binance, Bybit, OKX, Bitget, and most other large venues is every 8 hours, settling at 00:00, 08:00, and 16:00 UTC. Some venues run hourly funding (Hyperliquid uses 1-hour intervals as of 2026) and some use 4-hour cycles for low-liquidity pairs. The shorter the interval, the faster the contract price reacts to spot deviations.

Funding rate is a periodic payment between long and short perpetual futures traders that keeps the perp price tethered to spot. Longs pay shorts when funding is positive, shorts pay longs when funding is negative. Most exchanges settle funding every 8 hours.

History and Background: From BitMEX 2016 to Hyperliquid 2026

The perpetual futures contract was invented by BitMEX founder Arthur Hayes in 2016. Before perpetuals existed, crypto derivatives traders used quarterly futures with expiry dates, which forced them to roll positions every three months and absorb the basis differential at each roll. Hayes designed the perpetual swap to eliminate that friction by introducing a continuous funding mechanism that mimicked the convergence pressure of an expiry without the calendar deadline.

The first BitMEX XBTUSD perpetual launched in May 2016 with an 8-hour funding interval and quickly became the most liquid Bitcoin derivative in the world. By 2018 it was processing more daily volume than every other Bitcoin venue combined. The model was so effective that every major exchange copied it. Binance Futures launched USDT-margined perpetuals in September 2019. FTX brought multi-asset perpetuals in 2019 (before its 2022 collapse). Bybit, OKX, Deribit, Bitget, MEXC, and dozens of others adopted the same 8-hour funding cycle. By 2021, perpetual futures had decisively overtaken spot trading as the dominant crypto market structure.

On the on-chain side, perpetual DEXs took longer to mature. dYdX launched its v3 StarkEx-based perpetuals in 2021 and migrated to its own Cosmos appchain (dYdX v4) in late 2023, becoming the first major orderbook perp DEX with its own L1. GMX pioneered the peer-to-pool model on Arbitrum in 2021 with a unique borrowing-fee mechanism that differs from the orderbook funding model. Hyperliquid launched on its own L1 in 2023 and grew explosively through 2024 and 2025, eventually capturing the largest share of on-chain perp volume by early 2026 thanks to its 1-hour funding intervals, sub-second matching, and the November 2024 HYPE airdrop that distributed over $1 billion to early users. Vertex, Aevo, Drift on Solana, and a long tail of newer venues round out the modern perp DEX landscape.

The cash-and-carry basis trade, which is the dominant institutional strategy that harvests funding rate yield, became mainstream after the spot Bitcoin ETF launches in January 2024. With suddenly $20 billion plus of regulated spot demand chasing limited BTC supply, perpetual basis spreads widened to historically extreme levels, and funding rates on BTCUSDT perpetuals briefly exceeded 100% annualized in March 2024. The same dynamic repeated, with smaller magnitude, around the spot Ether ETF launch in mid-2024 and the spot Solana ETF launches in 2025. Every regulated spot ETF approval has compressed structural shorting capacity and pushed perp funding higher, often for months at a time.

How Funding Rate Actually Works: The Formula

The funding rate on most major exchanges is calculated using two components: the premium index and a fixed interest rate component. The combined formula looks like this:

The premium index (P) measures how far the perpetual contract is trading from the underlying spot index. It is sampled continuously throughout the funding interval and averaged. If the perpetual consistently trades above spot, P is positive. If it consistently trades below spot, P is negative.

The interest rate component (I) is a fixed value, usually 0.01% per 8-hour interval, which annualizes to roughly 10.95%. It represents the assumed cost of capital differential between the quote and base currencies. For USDT-margined perpetuals this is essentially a placeholder.

The clamp function dampens funding shocks. If the premium-interest gap is small, the funding rate equals the premium. If the gap is large, the funding rate adjusts within bounded thresholds to prevent extreme swings. Each exchange uses slightly different caps, which is why the same asset can show +0.012% on Binance and +0.0098% on Bybit at the same timestamp.

To convert an interval funding rate into an annualized rate, multiply by the number of intervals per year:

- 8-hour funding (Binance, Bybit, OKX): rate x 3 x 365 = APR. So 0.01% becomes 10.95%.

- 1-hour funding (Hyperliquid): rate x 24 x 365 = APR. So 0.00125% per hour becomes 10.95%.

- 4-hour funding (some altcoin pairs): rate x 6 x 365 = APR.

Positive vs Negative Funding: What the Sign Tells You

The sign of the funding rate is the first piece of information a derivatives trader looks at. It directly reveals which side of the market is more crowded and which side is paying to maintain that exposure. This is essential context for any long or short position in perpetuals.

Positive funding means the perpetual is trading at a premium to spot. Longs are aggressive enough that the price keeps drifting above the index. Funding becomes positive to incentivize shorts to step in and arbitrageurs to short the perp and buy spot. Sustained positive funding usually signals bullish sentiment or speculative crowding.

Negative funding means the perpetual is trading at a discount to spot. Shorts are aggressive, often during sharp sell-offs or coordinated bearish positioning. Funding becomes negative to incentivize longs to absorb that pressure. Sustained negative funding usually signals bearish sentiment or panic shorting.

Neutral funding (close to the baseline 0.01% interest component) means the perpetual is trading very close to spot and neither side has overwhelming pressure. Most quiet trending markets settle into a slightly positive baseline, which is mathematically the equilibrium when neither premium nor discount is meaningful.

Perp trading above spot. Bullish crowding. Often overheated above +0.05% per interval.

Perp trading below spot. Bearish crowding. Often overdone below -0.05% per interval.

Perp near spot. Quiet conditions or balanced positioning across both sides.

Severe crowding. Contrarian signal candidates if combined with structure.

Funding Rate Math: A Real Dollar Example

Funding stops being abstract the moment you translate it into a dollar number on a real position size. Let us walk through four concrete scenarios across different position sizes, leverage levels, and funding regimes. Every active perpetual trader should be able to do this math instantly on any position.

Scenario A: small retail long. You hold a $10,000 BTC perp long position into the 16:00 UTC funding settlement. The current funding rate is +0.0100%. Your funding payment is $10,000 x 0.0001 = $1.00 paid to shorts. Annualized, that is roughly 10.95% if funding stayed constant. Negligible for a single interval, but worth noting if you intend to hold the position through dozens of settlements.

Scenario B: medium leveraged long during an overheated rally. You hold a $100,000 ETH perp long with 5x leverage (so $20,000 margin). Funding spiked to +0.0750% for the next interval. Your funding cost is $100,000 x 0.00075 = $75 per 8 hours. That is $225 per day, or $82,125 annualized on a $20,000 margin commitment, a 410% drag on margin if the rate persists. This is why holding leveraged longs through extreme funding is dangerous. Even if the price keeps climbing, the funding bleed eats deeply into your realized profit.

Scenario C: short on Hyperliquid hourly funding. You short $50,000 of SOL on Hyperliquid where funding settles every hour. Current rate is +0.0040% per hour. Because you are short and funding is positive, you receive $50,000 x 0.00004 = $2.00 per hour, or $48 per day. Annualized that is roughly $17,500 in funding income on the short side, on top of any directional profit or loss. Hyperliquid's hourly settlement makes funding feel much more granular than the 8-hour CEX cadence.

Scenario D: basis trader earning yield. An institutional desk holds $10 million long BTC spot and $10 million short BTC perp, a market-neutral position. Funding is averaging +0.025% per 8-hour interval. They collect $10,000,000 x 0.00025 = $2,500 per interval, three times per day, every day. That is $7,500 per day or about 27.4% APR on the perp short notional. This is the cash-and-carry basis trade, and it scales to billions across institutional desks. Hedge funds, prop shops, and crypto-native yield desks compete fiercely for this trade whenever post-catalyst funding spikes appear.

Where and How to Check Funding Rates in 2026

You should never enter a perpetual position without checking the live funding rate first. Four data sources cover virtually all real-time and historical funding analytics in 2026:

- Coinglass (coinglass.com/FundingRate) - the de facto industry standard. Aggregates funding across 20+ exchanges with average, weighted average, and historical charts.

- CoinGecko Derivatives - cleaner UI, useful for cross-asset comparison and aggregated perp open interest.

- Exchange-native dashboards - Binance Futures, Bybit Derivatives, OKX Trading and Hyperliquid Stats all expose live funding plus historical curves on their platform.

- Velo Data and Laevitas - institutional-grade analytics with funding APR ranking, basis curves and predicted funding.

The pre-trade workflow should look like this: open Coinglass, check the funding rate on your target asset across at least three exchanges, look at the 7-day funding history chart to spot whether the current rate is normal or extreme by historical standards, then check the predicted funding for the next interval to know what you will pay if you hold through the timestamp.

The Cash-and-Carry Basis Trade: How Funding Becomes Yield

The cash-and-carry basis trade is the single most important institutional strategy in crypto derivatives. It converts the funding rate from a market signal into a steady yield stream. The setup is mechanically simple:

- Buy spot BTC (or any asset) on a regulated venue, usually $10 million plus in size for institutional execution.

- Short an equal notional BTC perpetual on a derivatives venue.

- Hold the market-neutral position and collect funding every 8 hours.

- Unwind both legs simultaneously when funding compresses or a better opportunity appears.

The position has near-zero directional risk because the spot and short perp cancel out. The only exposure is to funding rate compression, exchange counterparty risk, and execution slippage at entry and exit. In return the trader harvests whatever funding rate the perp pays the short side.

This trade exploded in volume after the January 2024 spot ETF launches. With BlackRock, Fidelity and other issuers bidding aggressively on regulated spot Bitcoin, the perpetual basis blew out and funding rates averaged 40 to 60% APR across Q1 2024. By mid-2024 the trade had attracted enough flow that funding compressed back to 15 to 25% APR ranges, still well above traditional fixed-income yields. The same pattern repeated around the November 2024 election rally and again following the spot ETH ETF approvals in 2024 and the spot SOL ETF approvals in 2025.

| Period | Asset | Avg funding APR |

|---|---|---|

| Mar 2024 (post-ETF mania) | BTC perp | 68% to 110% |

| May 2024 (halving aftermath) | BTC perp | 22% to 35% |

| Nov 2024 (election rally) | BTC and ETH perps | 45% to 80% |

| Q1 2025 (steady bull) | BTC perp | 15% to 28% |

| May 2026 (current) | BTC perp | 12% to 20% |

Funding Extremes as Contrarian Signal

One of the most powerful uses of funding rate is as a contrarian crowding indicator. When funding becomes extremely positive, it means longs are crowded and paying heavily to stay in the trade. That crowding makes the market vulnerable to a long squeeze if price stalls. When funding becomes extremely negative, shorts are crowded and the market is vulnerable to a short squeeze.

The key word here is combined. Funding extremes alone are not entry signals. Strong trends regularly carry extreme funding for days or weeks before any reversal. The trade only becomes high probability when funding extremes coincide with price exhaustion, declining market maker support, or position unwinding visible in liquidation zones.

Historical funding extremes that preceded major reversals include:

| Date | Event | Funding extreme | What followed |

|---|---|---|---|

| Apr 2021 | BTC top at $64k | +0.15% per 8h | 50% drawdown in 3 weeks |

| Nov 2021 | BTC ATH $69k | +0.12% per 8h | Multi-month bear market start |

| Mar 2024 | Post-ETF BTC $73k | +0.18% per 8h | 20% pullback over 2 months |

| Jul 2024 | German govt sell-off bottom | -0.08% per 8h | 15% rally in 2 weeks |

| Dec 2024 | Post-election BTC top $108k | +0.20% per 8h | 25% correction in Q1 2025 |

Perp DEX Funding vs CEX Funding: The Spread Opportunity

The rise of on-chain perpetual exchanges has created a new class of funding arbitrage. Perp DEX funding rates often diverge meaningfully from CEX funding rates for the same asset because the user bases, market making depth, and order flow differ in structural ways that the funding mechanism cannot instantly resolve.

Hyperliquid, for example, frequently shows funding rates 20 to 40% higher or lower than Binance during fast moves because Hyperliquid's user base is more retail-leveraged and reacts faster to news. dYdX v4 funding can run cooler than Binance because of its more institutional liquidity providers. GMX uses a fundamentally different peer-to-pool model where borrowing fees replace traditional funding, so it does not show comparable funding numbers in the same way. Vertex and Drift tend to track CEX funding more closely because of the integrated market maker infrastructure they share with centralized order flow.

This creates a cross-venue arbitrage where a trader can long the asset on the venue with cheaper funding and short it on the venue with expensive funding, capturing the spread. The opportunity is real but execution is hard because gas costs, withdrawal delays between centralized exchanges and chains, and counterparty risk all eat into the theoretical edge. Sophisticated desks that operate continuously across all major venues can capture even small persistent spreads, which is why structural divergences between CEX and DEX funding rarely persist beyond a few funding cycles for the largest assets.

For retail traders, the practical takeaway is simpler. If you are going to short on a perp DEX with persistently higher funding than Binance, you collect that extra yield as a tailwind. If you are going to long on the same venue, you pay the higher funding as a headwind. Always look up funding at your specific venue before deciding where to take the position, not just on the aggregate that Coinglass shows by default.

| Venue | Type | BTC funding | Interval |

|---|---|---|---|

| Binance | CEX | +0.0085% | 8h |

| Bybit | CEX | +0.0094% | 8h |

| OKX | CEX | +0.0078% | 8h |

| Hyperliquid | DEX | +0.0125% (annualized: 109%) | 1h |

| dYdX v4 | DEX | +0.0080% | 8h |

| Vertex | DEX | +0.0102% | 1h |

Funding Rate vs Open Interest: The Two-Variable Read

Funding rate and other derivatives metrics are most useful when combined with open interest. The two together reveal not just which side is paying, but whether the imbalance is growing or unwinding.

Open interest measures the total dollar value of outstanding perpetual contracts. Rising open interest with rising price plus positive funding means new longs are entering and pushing the rally. That is healthy at first but becomes overcrowded above certain thresholds. Rising open interest with falling price plus negative funding means new shorts are entering and pressuring the market. Falling open interest with extreme funding means positions are unwinding rapidly, which often precedes major moves.

Steady bullish trend with controlled crowding. Continuation likely until funding spikes.

Overcrowded longs. Vulnerable to long squeeze if momentum stalls.

Forced unwinding. Short squeeze setup if buyers step in.

Position closing without directional commitment. Often precedes a breakout either way.

Step-by-Step: How to Use Funding Rate Before Every Trade

Here is the disciplined pre-trade funding workflow that separates serious derivatives traders from casual leverage users:

- Open Coinglass and load your target asset. Check the current funding rate on the venue you plan to trade.

- Compare across at least three exchanges. If your venue is an outlier, consider switching to a cheaper funding venue or reducing size.

- Pull up the 7-day funding history chart. Is the current rate normal, extended, or extreme by recent context?

- Check the next funding timestamp. If you are likely to hold through the settlement, calculate the dollar cost on your position size.

- Compare with open interest. Is OI rising into a positive funding spike (crowding) or unwinding (capitulation setup)?

- Check predicted funding. Most exchanges show a forecasted next-interval rate. If predicted is higher than current, the crowding is accelerating.

- Reduce size or skip the trade if the funding cost exceeds 5% of your expected profit target. Carry should never dominate your thesis.

- Set an alert. If funding flips sign during your trade, that is a meaningful change in market structure.

Funding History: Major 2024-2026 Events

Looking back at how funding behaved during major market events teaches more than any theoretical model. These five inflection points define the modern funding regime:

January 10, 2024: spot Bitcoin ETF approval. The SEC approved 11 spot Bitcoin ETFs simultaneously. Within 72 hours, BTC perp funding on Binance jumped from a neutral 0.01% to over 0.08% per 8 hours. The cash-and-carry basis trade became the most lucrative low-risk strategy in finance, with annualized yields above 60%.

March 14, 2024: BTC ATH at $73,750. Funding peaked at extreme levels across all venues, briefly hitting 0.18% per 8 hours on Binance. This was a textbook contrarian extreme, followed by a 20% drawdown over the next two months.

April 20, 2024: Bitcoin halving. Funding had cooled to neutral territory in the lead-up to the halving as the rally consolidated. Post-halving, funding stayed unusually muted through mid-2024, reflecting cautious positioning and the German government BTC liquidation that capped enthusiasm.

November 5, 2024: US election rally. BTC perp funding spiked alongside the Trump victory rally, hitting +0.20% per 8 hours by early December. The contrarian signal worked again, with a 25% correction following in Q1 2025.

November 29, 2024: Hyperliquid HYPE airdrop. The HYPE token airdrop distributed over $1 billion to early users and cemented Hyperliquid as the dominant on-chain perp venue. Funding spreads between Hyperliquid and Binance widened in the following months as the retail-heavy Hyperliquid order flow created different positioning dynamics than the institutional flow on Binance.

Common Funding Mistakes to Avoid

Funding rate is powerful but easy to misuse. These are the five mistakes that crush traders who rely on funding without understanding it:

Extreme funding can persist for weeks in strong trends. Use it as filter, not signal.

On 10x leverage, a 0.05% funding rate is 0.5% per interval drag on margin. It adds up fast.

8-hour and 1-hour funding rates are not directly comparable. Always convert to APR first.

Even at funding extremes, trends can run further. Size contrarian fades small.

When funding flips sign during your position, the crowding side has changed. Reassess.

Funding can compress fast. Basis trades need an exit plan, not just an entry.

Risks of Trading Around Funding Rate

Funding-based trading carries specific risks that differ from pure directional trading. The first risk is that funding can flip suddenly. A trade that pays you funding on Monday can charge you funding by Wednesday if positioning shifts. Anyone relying on funding income should have alerts and an exit plan.

The second risk is execution slippage on basis trades. When you enter a $10 million cash-and-carry position, the spot leg and perp leg each move the price slightly during execution. If the basis compresses while you are still building the position, your expected yield erodes before you have even fully entered.

The third risk is counterparty risk on the exchange. The FTX collapse in November 2022 wiped out billions in basis trade positions where traders had spot on one venue and short perp on FTX. Always diversify across multiple exchanges and never park more than necessary on any single venue. Strong wallet and exchange security practices apply double here.

The fourth risk is liquidation cascades. Extreme funding extremes coincide with extreme leverage, and when those positions liquidate in clusters, the price moves can be violent enough to liquidate even reasonably sized positions on the same side. Always know where your liquidation price sits relative to current price and to nearby liquidation zones.

The fifth risk is exchange-specific mechanic differences. Some venues cap funding at +/- 0.75% per interval. Others adjust the index calculation during high volatility. Always read the funding methodology page for your chosen venue before depending on funding for income.

Best Practices for Funding Rate Trading

Putting it all together, the traders who consistently benefit from funding rate awareness share a small set of habits:

- Check funding before every perp entry, no exceptions. Even a 30-second glance prevents expensive surprises.

- Track funding by APR, not by interval rate. Mental math gets confused by interval differences across venues.

- Maintain a watchlist of funding extremes. Coinglass lets you sort by absolute funding to spot stretched markets across hundreds of assets.

- Use funding as a position-sizing input. The higher the funding cost, the smaller the position should be relative to your normal size.

- Combine funding with structure. A funding extreme at a key support or resistance level is far more meaningful than a funding extreme in the middle of a range.

- Learn the basis trade if you have meaningful capital. Even $50,000 deployed as cash-and-carry can produce meaningful tax-efficient yield in high-funding regimes.

- Backtest funding-based strategies properly. Use historical funding data alongside price for any backtesting workflow rather than assuming average rates.

- Stay current on venue mechanics. Exchanges occasionally change funding caps, intervals, or premium index methodology.

Frequently Asked Questions

Q Q Q What is funding rate in crypto?

Funding rate is a periodic payment between long and short perpetual futures traders that keeps the perp price tethered to spot. Longs pay shorts when funding is positive, shorts pay longs when funding is negative. Most exchanges settle funding every 8 hours at 00:00, 08:00 and 16:00 UTC.

Q Q Q Who actually receives the funding payment?

The other side of your trade. The exchange does not take the funding payment. If funding is +0.01% and you hold a long, the short side of the market receives your payment. The exchange only collects standard trading fees on entries and exits.

Q Q Q How do I convert funding rate to APR?

Multiply the interval rate by the number of intervals per year. For 8-hour funding: rate x 3 x 365. So 0.01% per 8 hours equals 10.95% APR. For 1-hour funding on Hyperliquid: rate x 24 x 365. So 0.00125% per hour also equals 10.95% APR.

Q Q Q Does high funding mean a price crash is coming?

Not automatically. Extreme positive funding signals overcrowded longs and adds reversal probability, but trends can persist with extreme funding for weeks. Use funding as confluence with price structure, open interest, and liquidation positioning rather than as a standalone reversal trigger.

Q Q Q What is the cash-and-carry basis trade?

A market-neutral strategy where you buy spot Bitcoin (or any asset) and short an equal notional perpetual contract. The position has near-zero directional exposure but collects the funding rate paid to shorts. During post-ETF March 2024, basis trade APRs exceeded 80% on BTC, attracting billions in institutional flow.

Q Q Q Why is Hyperliquid funding sometimes very different from Binance?

Different user bases. Hyperliquid is dominated by retail-leveraged traders and reacts faster to news, while Binance carries institutional flow that dampens extremes. Hyperliquid also uses 1-hour funding intervals versus 8-hour on Binance, so its funding adjusts much faster to spot deviations.

Q Q Q How often does funding rate settle?

Most CEX perpetuals settle funding every 8 hours, at 00:00, 08:00 and 16:00 UTC. Hyperliquid runs 1-hour intervals. Some altcoin pairs on certain venues use 4-hour intervals. Always check your specific market and exchange before holding a position into the funding timestamp.

Q Q Q Can I avoid funding by closing before the timestamp?

Yes. Funding is only paid if you hold a position at the exact funding timestamp. Closing before the timestamp and reopening after avoids the payment, though you incur trading fees on both legs. This is rarely worth it unless funding is exceptionally extreme.

Q Q Q What is the highest funding rate ever recorded?

During extreme bull market peaks, BTC perp funding has exceeded +0.20% per 8-hour interval on multiple occasions, including March 2024, December 2024, and the original April 2021 peak. Annualized, that is over 200%. Altcoin perpetuals during meme coin manias have temporarily exceeded +1% per 8 hours, which would be over 1000% APR.

Q Q Q Do perpetual DEXs like GMX have funding rates?

GMX uses a different model called borrowing fees rather than traditional funding. Traders pay an hourly borrowing fee to the liquidity pool based on utilization. Hyperliquid, dYdX v4, Vertex, and most orderbook-style perp DEXs use the standard funding rate model with longs and shorts paying each other.

Q Q Q How should beginners actually use funding rate?

Treat it as a filter, not a signal. Before entering any perpetual position, check the funding rate and ask yourself whether the trade still makes sense given the crowding context. If funding is extreme in the direction you want to trade, demand a better setup or reduce position size. Beginners should never trade based on funding alone.

Conclusion: Funding Rate Is the Pulse of Perp Markets

Funding rate started in 2016 as a clever engineering trick to keep BitMEX perpetual swaps anchored to spot. Ten years later it has become the single most important sentiment indicator in crypto derivatives, the foundation of institutional basis trading, and a key driver of multi-billion-dollar yield strategies. Whether you trade Bitcoin perpetuals on Binance, ETH perps on Hyperliquid, or run a cash-and-carry basis position to earn double-digit APR, funding rate is the variable that decides whether your trade pays you or costs you.

The mechanics are simple. Longs pay shorts when funding is positive, shorts pay longs when funding is negative, the rate adjusts dynamically based on the perpetual premium to spot, and most exchanges settle every 8 hours. The applications are deep. Funding tells you who is crowded, who is paying, when the market is overheated, when shorts are overdone, and how much yield you can harvest from a market-neutral basis trade. The risks are real. Funding can flip suddenly, basis trades can compress fast, and venue mechanics differ enough to catch unprepared traders off guard.

The best traders treat funding rate as one of three or four core inputs alongside price structure, open interest, and liquidation positioning. They never use it as a standalone trigger. They always convert interval rates to APR before comparing venues. They check funding before every entry and they size positions with funding cost in mind. Build the same habits and funding rate stops being a number on the screen and starts being a real edge.

Funding rate is one piece of the derivatives puzzle. Continue your education with these related DEXTools tutorials.

Disclaimer: This article is for educational purposes only and does not constitute investment, financial, legal, or trading advice. Perpetual futures and leveraged products are high-risk instruments. Funding rates, exchange mechanics, and venue rules change over time. Always verify the current funding methodology on the platform you use before deploying capital.

Related Guides

- What Is a Funding Wallet in Crypto? Explained 2026

- Coinglass Tutorial 2026: Liquidations & OI Master Guide

- How to Use Binance in 2026: Beginner Setup, Funding and Core Features

- Pendle Finance Explained: Yield Tokenization, PT, YT and Fixed-Rate DeFi (2026)

- What Is an RPC Rate Limit in Crypto? Explained 2026