Aave Credit Markets Explained: Peer-to-Pool Lending, Collateral and GHO (2026)

A protocol-level guide to Aave as DeFi credit infrastructure, covering peer-to-pool liquidity, collateral design, liquidation mechanics, and where GHO fits.

Intent check: This page is the credit-markets explainer for Aave. If you want the cleaner overview of V3, GHO, and risk modes, read Aave Protocol Explained. If you want the hands-on walkthrough for deposits, borrowing, and Health Factor, read How to Use Aave.

The Financial Evolution: From Centralized Banking to Non-Custodial Credit

- The core promise of decentralized finance (DeFi) is the elimination of intermediary credit brokers. In traditional finance, commercial banks control capital allocation, dictating borrowing costs and deposit yields while introducing centralized counterparty risk.

- The cryptocurrency market replaces this legacy framework with autonomous smart contract structures. At the absolute center of this credit infrastructure sits Aave.

- Originally launched in 2017 as ETHLend before rebranding to its current architecture, Aave has matured into a foundational liquidity protocol of Web3. Operating across multiple blockchain layers with tens of billions in total value locked, the protocol provides an open marketplace for non-custodial lending and borrowing.

1. Core Infrastructure: The Peer-to-Pool Lending Model

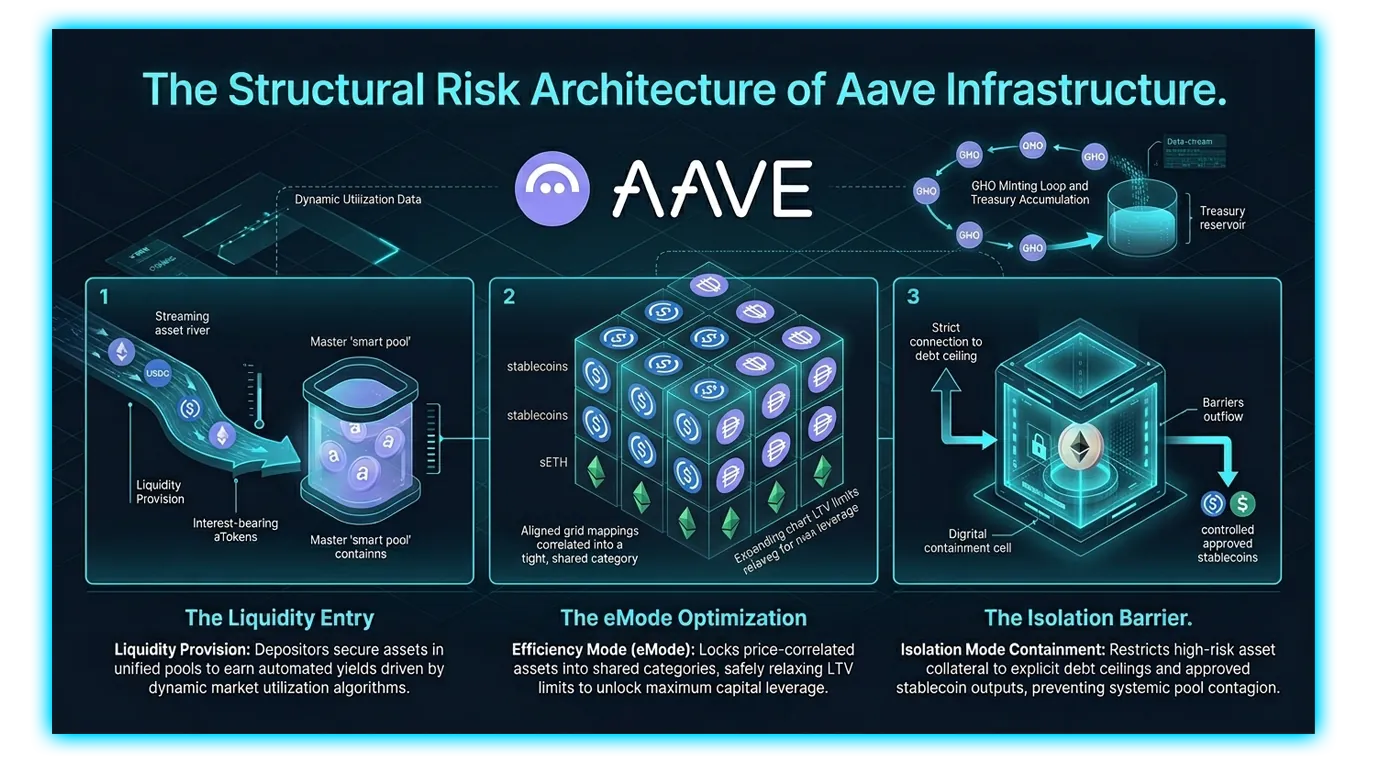

Early decentralized lending attempts relied on peer-to-peer matching engines, which suffered from low execution speeds and highly fragmented liquidity. Aave revolutionized this landscape by pioneering the peer-to-pool liquidity model.

Depositors and aTokens

Instead of waiting for a direct match, lenders deposit their digital assets into unified smart contract pools. The moment liquidity is provided, the protocol automatically mints and issues an equivalent quantity of derivative tokens known as aTokens (e.g., depositing USDC yields aUSDC).

These aTokens function as a cryptographic receipt of your deposit.

They continuously accrue interest directly inside your Web3 wallet, matching the real-time interest rate generated by the pool.

Lenders can redeem their aTokens to reclaim their original underlying principal plus all accumulated interest at any time, provided the pool maintains unborrowed liquidity.

Borrowers and the Dynamic Utilization Rate

- To withdraw assets from a pool, borrowers must provide independent, high-quality collateral that exceeds the value of the loan. This requirement ensures the protocol remains fully over-collateralized against market volatility.

- The interest rates paid by borrowers and earned by depositors are entirely automated. The protocol adjusts rates dynamically using an algorithm based on the Utilization Rate of each specific asset pool. When capital is abundant and the utilization rate is low, borrowing rates drop to entice capital withdrawal.

- Conversely, when the pool's liquidity tightens and utilization approaches maximum capacity, interest rates spike sharply. This mechanism encourages borrowers to repay their debts while rewarding depositors with higher yields, protecting the pool from liquidity exhaustion.

2. Aave V3 Architecture: Advanced Risk Containment

The introduction of the Aave V3 architecture shifted the protocol from an open lending marketplace into an institutional-grade risk management platform. V3 implemented modular asset categorization to prevent systemic contagion across volatile token pairs.

Efficiency Mode (eMode)

- Efficiency Mode, or eMode, is engineered to maximize borrowing capacity for price-correlated assets. When assets share highly correlated price movements, the structural risk of sudden collateral divergence is minimal.

- LPs can activate eMode when both their supplied collateral and borrowed assets belong to the same economic category, such as stablecoins or liquid staking derivatives (e.g., stETH collateral backing a WETH loan). Under an active eMode configuration, the protocol safely relaxes traditional borrowing constraints:

The Loan-to-Value (LTV) limit increases significantly, allowing users to unlock maximum capital efficiency.

The liquidation threshold is extended close to the parity line, enabling highly leveraged, low-risk delta-neutral looping strategies that would trigger instant liquidations in standard markets.

Isolation Mode

While eMode maximizes efficiency for safe assets, Isolation Mode acts as a containment shield for long-tail, exotic, or newly listed volatile assets. When Aave Governance approves a new asset with an isolation designation, it is walled off from the core protocol liquidity layers:

Users who supply an isolated token as collateral are restricted to a defined debt ceiling.

While using an isolated asset as backing, the user cannot enable any other assets as collateral within that wallet session.

The borrower is restricted to withdrawing only specific, highly liquid, governance-approved stablecoins, preventing an exploit or flash crash of an exotic token from draining premier crypto reserves like Ethereum or Bitcoin from the main protocol.

3. The GHO Stablecoin Facilitator

- To further internalize credit generation and create an independent revenue engine, the protocol launched GHO, Aave's native decentralized, over-collateralized stablecoin pegged to the U.S. Dollar.

- Unlike centralized stablecoins that rely on commercial bank reserves, GHO is minted directly on-chain by users utilizing their existing Aave V3 asset deposits as collateral. While your underlying collateral continues to earn baseline protocol yield, you can mint GHO against it to access liquid capital.

The Treasury Loop and Bridging Mechanics

- GHO introduces a highly sustainable revenue model for the platform. When a borrower repays their GHO position along with accumulated interest, 100% of that interest income is routed directly into the Aave DAO Treasury rather than being distributed to external liquidity suppliers. This capitalizes the platform's safety module and funds future development ecosystem rails.

- Furthermore, GHO utilizes advanced cross-chain facilitators powered by secure bridging infrastructure, allowing the asset to move between alternative Layer 2 execution environments without liquidity fragmentation.

4. Technical Trade-offs and Market Realities

Protocol Structural Matrix

| Risk Parameter | Standard Mode | Efficiency Mode (eMode) | Isolation Mode |

| Collateral Asset Type | Diversified Blue-Chip Assets | Price-Correlated Categories | Exotic / Long-Tail Tokens |

| Loan-to-Value Cap | Moderate (e.g., 70% - 80%) | Maximum Optimization (up to 90%+) | Constrained by Strict Debt Ceilings |

| Borrowing Asset Access | Unrestricted Protocol Assets | Restricted to Same Category | Approved Stablecoins Only |

| System Contention Risk | Systemic Portfolio Exposure | Restricted to Correlated Gaps | Complete Isolation Containment |

Systemic Vulnerabilities and Mitigation

The Liquidation Threshold and Health Factor: If market volatility causes the value of a user's collateral to decline relative to their debt, the position's automated Health Factor drops. If this metric dips below the safety baseline, the protocol permits decentralized liquidators to purchase a portion of the debt at a discount, instantly selling the underlying collateral to restore system solvency.

Smart Contract Dependency: Despite continuous multi-firm code audits, operating an extensive multi-chain lending engine introduces execution vulnerabilities, requiring the platform to maintain a robust Safety Module backed by staked assets to absorb potential bad debt events.

Remember that you can easily and securely swap tokens using the best DeFi tools with DEXTools. Click here to get started today.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.

Related Guides

- Aave Protocol Explained: V3, GHO, Risk Modes and How the Market Works (2026)

- How to Borrow on Aave Safely: Collateral, Health Factor and Repayment Flow (2026)

- What Is TrueFi (TRU)? Uncollateralized DeFi Lending and Credit Guide 2026

- Collateral Risks in DeFi Lending: A Crucial Insight

- How to Use Aave: Deposit, Borrow, Repay and Manage Health Factor (2026)

Frequently Asked Questions

What is Aave?

Aave is a decentralized lending protocol where users can supply assets to earn yield and borrow against collateral. It uses a peer-to-pool model rather than matching individual lenders and borrowers.

How does peer-to-pool lending work on Aave?

Lenders deposit assets into shared liquidity pools, and borrowers draw from those pools by posting collateral. Interest rates adjust based on how much of the pool's liquidity is being used.

What is GHO in the Aave ecosystem?

GHO is a stablecoin associated with the Aave ecosystem that can be minted against supplied collateral. As a stablecoin, it aims to maintain a stable value while integrating with the protocol.

What is liquidation on Aave?

Liquidation occurs when a borrower's collateral value falls too low relative to their loan, allowing part of it to be sold to repay debt. It is the mechanism that keeps the protocol solvent when positions become undercollateralized.