Best Stablecoins for Saving in High-Inflation Countries 2026

The best stablecoins to protect savings from inflation in 2026. Compare USDT, USDC and yield options by safety, access and how to hold them securely.

USD-pegged stablecoins are the best stablecoins for saving in high-inflation countries, offering a digital alternative to physical U.S. dollar banknotes. For individuals in hyper-inflationary regimes, these digital dollars provide essential infrastructure for defending purchasing power and preserving wealth against rapidly devaluing local currencies like those in Argentina and Turkey.

A Real-World Capital Preservation Guide: the problem of inflation.

- Living in an economy experiencing double or triple-digit inflation transforms basic wealth preservation from a passive habit into an active survival strategy. In regions like Argentina and Turkey, local currencies function less as stores of value and more as melting ice cubes. Historically, the traditional escape hatch was physical U.S. dollar banknotes acquired via informal parallel markets. Today, that analog framework has been replaced by a digital layout: USD-pegged stablecoins.

- For individuals navigating hyper-inflationary regimes, digital dollars are not a speculative tool for chasing yield; they are the primary infrastructure for defending purchasing power. However, migrating your life savings onto blockchain rails introduces a distinct matrix of technical trade-offs, custody choices, and access points. This guide provides a objective framework for selecting stablecoins, utilizing peer-to-peer networks, and securing assets over multi-year horizons.

1. The Core Choices: Evaluating Capital Infrastructure

When your primary objective is capital preservation, your choice of stablecoin must prioritize liquidity depth, redemption resilience, and ease of access over speculative features.

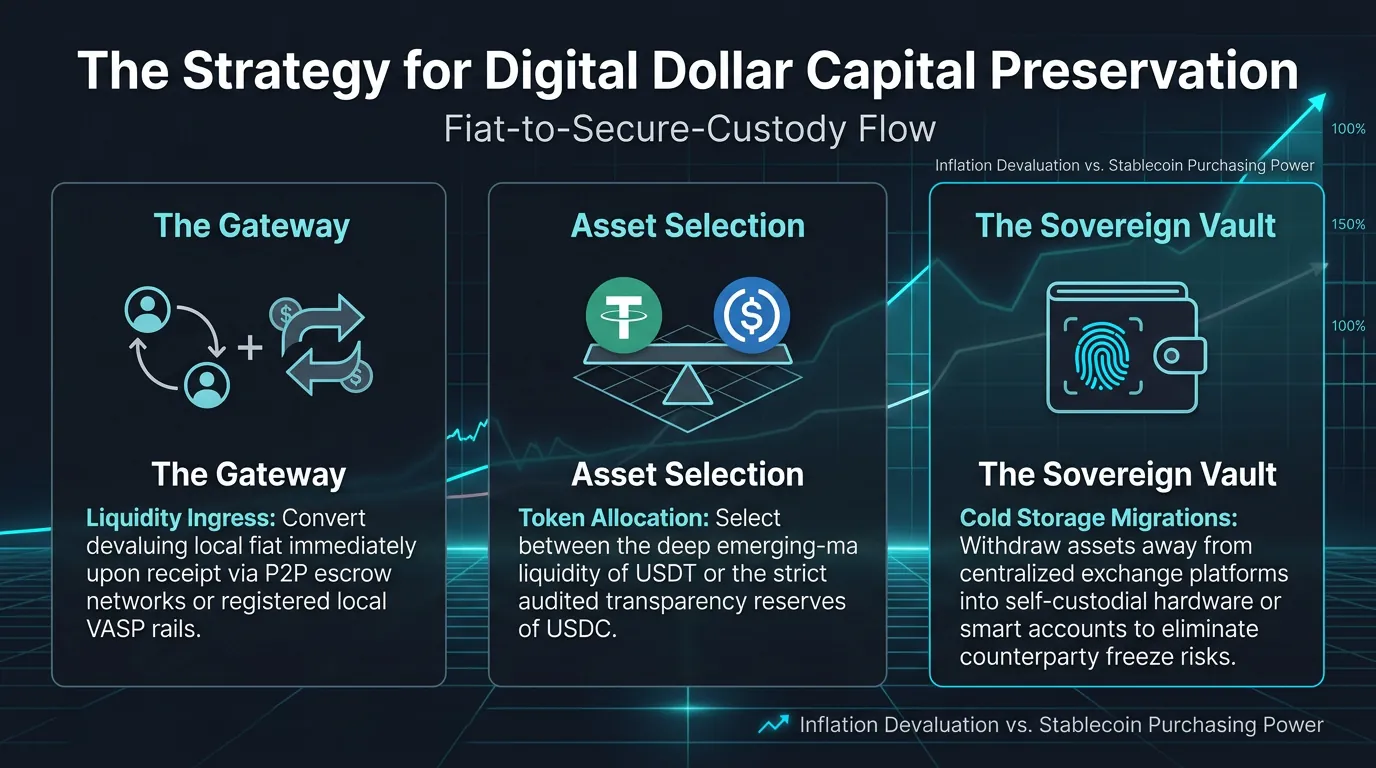

Tether (USDT): The Emerging Market King

Tether remains the undisputed base currency of global emerging markets. In high-inflation countries, USDT is often synonymous with the "digital dollar" itself.

The Liquidity Moat: USDT possesses the deepest liquidity pools across peer-to-peer networks and local centralized exchanges. When you need to quickly liquidate digital assets to pay for real-world expenses like rent or groceries, USDT offers the lowest execution friction where inflation is causing problems.

The Structural Risk: Tether operates out of offshore jurisdictions and provides lower reserve transparency compared to its primary competitors. While it has survived multiple market cycles and extreme stress tests, it carries a higher regulatory and counterparty risk profile.

USD Coin (USDC): The Transparency Standard

Issued by Circle, USDC is positioned as a highly transparent, fully audited digital dollar alternative, backed 1:1 by cash and short-term U.S. Treasury bills held in compliant U.S. banking custody.

The Institutional Rail: USDC is the preferred choice for international remote workers, contractors, and corporate treasury management. If you are receiving international payroll, USDC offers a seamless connection to compliant international fintech platforms.

The Liquidity Trade-off: In local peer-to-peer cash markets within developing nations, USDC liquidity can be thinner than USDT, occasionally resulting in wider spreads when converting back to local physical fiat.

2. Regional Case Studies: Financial Survival in Practice

The operational reality of stablecoin adoption is best understood by looking at the world's primary digital dollar testing grounds.

Argentina: The "Dólar Cripto" Economy

Argentina has become a global leader in cryptocurrency adoption out of pure macroeconomic necessity. The local market operates with multiple parallel exchange rates due to historical currency controls.

The Regulatory Landscape: The ecosystem has transitioned from an unregulated gray market into a structured environment. The government enforces a mandatory Virtual Asset Service Provider (VASP) registry under the National Securities Commission (CNV). Major international platforms and local fintech aggregators must register to operate legally.

The Stablecoin Payroll Paradigm: Stablecoins have become a standardized compliance rail for tech freelancers and contractors. Under regimes like the "Monotributo" (simplified tax framework), international contractors frequently receive 100% of their compensation in USDT or USDC, converting only what is necessary into Argentine Pesos to manage daily costs.

Turkey: The Lira-to-USDT Volume Dominance

In Turkey, the structural depreciation of the Turkish Lira (TRY) has driven retail participants directly into digital assets. The TRY/USDT pair consistently ranks among the highest fiat-to-crypto volume corridors globally on centralized exchanges.

Local Fintech Integration: Instead of relying entirely on decentralized apps, the Turkish ecosystem utilizes local digital ramps (such as Paribu or BtcTurk) tied directly to traditional tier-one banking networks.

The Asset Protection Vehicle: Unlike Western markets where crypto is treated as a high-risk tech stock alternative, Turkish savers use USDT exactly like a traditional foreign currency bank account, parking their capital in digital dollars to neutralize intra-month fiat devaluation.

3. Access Points: P2P Networks and Regional Rails

Acquiring stablecoins in an environment with inflation, requires navigating around restrictive local banking corridors.

Peer-to-Peer (P2P) Desks: P2P platforms serve as the primary decentralized escrow layer. A buyer transfers local fiat currency directly to a seller’s local bank account or fintech app, and the platform releases the corresponding stablecoins from escrow to the buyer's digital wallet. This mechanism bypasses international wire limitations and allows for localized price discovery.

Crypto Criptocuevas (Crypto Caves): In regions with dense urban populations like Buenos Aires or Istanbul, physical over-the-counter (OTC) desks operate openly. Users can walk into a physical office, hand over physical cash (local fiat or physical USD banknotes), and receive stablecoins directly to their self-custody wallets via a QR code scan.

Technical Trade-offs and Market Realities

Critical Analysis: Strengths and Limitations

Systemic Advantages

Instant Value Lock: Stablecoins allow users to convert local fiat into a dollar-denominated asset the exact moment they receive their salary, neutralizing the impact of mid-month inflation.

Frictionless Portability: Digital dollars are stored cryptographically. Unlike physical cash reserves, they cannot be seized at physical borders, lost in household accidents, or restricted by localized banking holidays.

Global Asset Market Access: Holding stablecoins connects individuals directly to global decentralized financial infrastructure, enabling access to tokenized real-world assets or international lending yields.

Structural Risks

Regulatory Compliance Shifts: As nations formalize VASP registries, the anonymity of localized exchange ramps is decreasing. Centralized exchanges are mandated to report transaction metrics to local tax authorities, altering the privacy profile of digital savings.

Smart Contract and Protocol Risk: Stablecoins are software. If an underlying issuer faces a catastrophic asset freeze, or if a cross-chain bridge suffers an exploit, your digital dollars can lose their peg or become completely illiquid.

Counterparty Isolation: Centralized issuers (Tether and Circle) retain the protocol-level capability to freeze wallet addresses globally under regulatory orders, meaning your financial sovereignty is ultimately subject to global compliance demands.

4. The Security Frontier: Custody Options

How you store your stablecoins determines your true level of financial protection. Leaving your entire life savings on a centralized local exchange (CEX) exposes you to the exact same counterparty risks as a traditional local bank account.

Centralized Exchanges (CEXs / Local VASPs)

The Reality: Convenient for daily transactions and quick fiat off-ramping.

The Risk: If the exchange faces corporate insolvency, local regulatory freezings, or operational pauses, your funds can be locked indefinitely.

Self-Custody (Hardware and Smart Accounts)

The Reality: True financial self-sovereignty. By holding your assets in a private wallet where you control the cryptographic keys, no corporate entity or local bank can freeze your account.

Modern Tooling: In the current wallet ecosystem, users can leverage Smart Accounts powered by biometric passkeys (FaceID/Fingerprints) or secure hardware wallets (Ledger/Trezor). This configuration removes the vulnerability of losing a physical 12-word paper seed phrase while maintaining absolute control over the underlying private keys.

5. On-Chain Telemetry and Capital Auditing via DEXTools

- When saving over long-term horizons, capital must occasionally be moved across different blockchain layers (e.g., Ethereum to Base or Arbitrum) to minimize gas fees. Before interacting with automated market makers, decentralized cross-chain bridges, or local wrapper tokens, independent data verification is required to prevent exposure to malicious smart contract traps or illiquid pools.

- Market participants use real-time data feeds from www.dextools.io to monitor asset status and trader activity in real time, as well as to assess a token’s liquidity and volume, and also its reliability through Audits and DEXTscore. You can access DEXTools today here and start trading easily and securely.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.

Related Guides

- TON Tokenomics: Toncoin Supply, Distribution and Inflation Explained (2026)

- What Is ETH ATH? Ethereum All-Time High Explained

- Solana All-Time High Explained: The ATH Run

- Where to Stake ETH: Top 2026 Platforms for High Yields

- How Stablecoins Keep Their Peg: Collateral Models, Depeg Risk and On-Chain Checks

Frequently Asked Questions

Why do people in high-inflation countries use stablecoins for saving?

Stablecoins are designed to track the value of a stable asset such as a major currency, which can help preserve purchasing power when a local currency loses value quickly. They offer a way to hold a more stable unit of value digitally.

What is a stablecoin?

A stablecoin is a cryptocurrency designed to maintain a steady value by being pegged to an asset like a fiat currency. The peg is maintained through mechanisms such as reserves or algorithms, depending on the stablecoin.

Are stablecoins safe for storing savings?

Stablecoins carry risks including the peg breaking, issuer or reserve problems, smart contract bugs, and regulatory changes. They reduce price volatility compared to other crypto but are not risk-free.

What is the difference between fiat-backed and algorithmic stablecoins?

Fiat-backed stablecoins aim to hold reserves of currency or equivalents to back each token, while algorithmic stablecoins use code and incentives to maintain their peg. Algorithmic designs have historically carried higher risk of losing their peg.