What is Maple Finance? Institutional Lending Explained

Traditional DeFi requires massive over-collateralization, blocking real corporate scaling. We break down the underwriting, retail wrappers, and buyback tokenomics of Maple Finance.

The Corporate Credit Crunch on Maple Finance: Bringing Traditional Underwriting On-Chain

- Standard decentralized finance (DeFi) lending applications rely almost entirely on programmatic over-collateralization. While locking up more assets than you borrow works perfectly for anonymous retail traders and speculative margin loops, it creates a massive structural bottleneck for real-world corporations. Legitimate institutions (such as proprietary trading desks, market makers, and scaling hedge funds) do not operate by keeping idle crypto sitting as excess security bonds. They scale their businesses using credit lines backed by historical performance, robust balance sheets, and formal legal underwriting.

- Maple Finance bridges this gap. Operating as an on-chain capital marketplace built primarily on Ethereum, Maple introduces structured institutional credit markets to the blockchain ledger. By combining traditional underwriting compliance with public cryptographic rails, the protocol enables institutions to tap into deep stablecoin liquidity pools without being bound by rigid over-collateralization rules. This guide explores how Maple manages risk through credit experts, handles permissionless retail access via yield wrappers, and break downs its major tokenomic evolution to the SYRUP token.

1. The Underwriting Engine: Pool Delegates

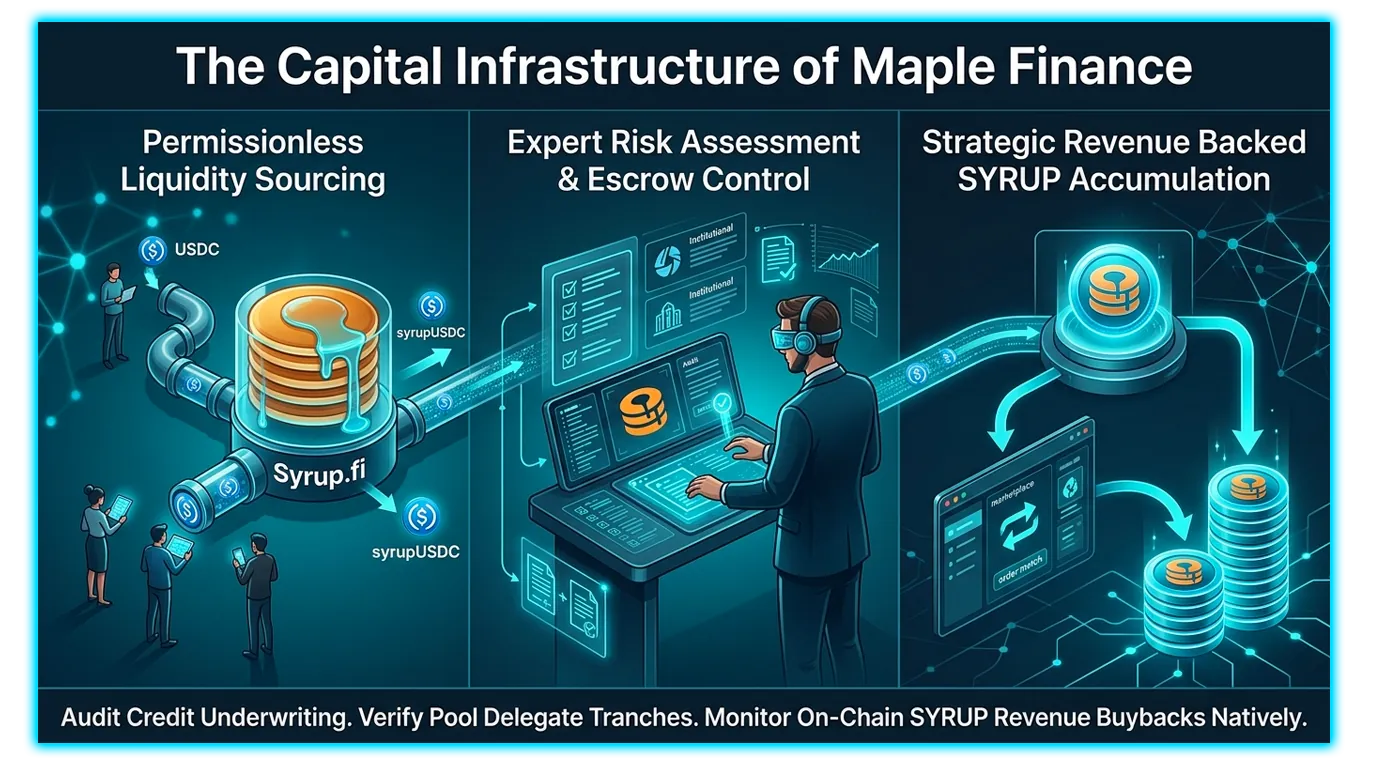

Unlike automated lending pools where smart contracts blindly check a mathematical liquidation threshold, Maple Finance delegates risk management to specialized entities known as Pool Delegates.

Pool Delegates act as decentralized credit officers and underwriting asset managers. Typically comprised of professional credit firms (such as Maple Direct, Room40, or AQRU), these delegates handle the critical operational components of a loan lifecycle:

Bespoke Underwriting: Delegates perform rigorous financial due diligence, assess historical trading records, and verify Know-Your-Customer (KYC) documents to establish explicit credit limits.

Setting Loan Terms: They negotiate custom fixed rates and tenors (typically 30- to 180-day repayment schedules) based on the borrower's risk profile.

Skin in the Game: To align incentives and shield lenders from systemic defaults, Pool Delegates are required to post a "first-loss" capital tranche into their own pools. If a borrower defaults, the delegate's capital is seized first to reimburse lenders.

2. Democratizing Access: Syrup.fi and syrupUSDC

Historically, interacting with Maple's premium credit markets required passing through institutional KYC compliance gates, locking out retail DeFi participants. The platform bypassed this friction via its retail-facing ecosystem extension, Syrup.fi.

Syrup acts as an accessible bridge that wraps institutional yields into a composable, liquid asset wrapper called syrupUSDC.

The Yield Pipeline: Retail users deposit standard USDC directly into the permissionless Syrup vault. The protocol automatically deploys these pooled stablecoins straight into Maple’s institutional lending books.

Instant Yield Accrual: In return, users receive

syrupUSDC. This token operates as an auto-compounding wrapper that accrues real-world interest generated from active corporate loan repayments (not speculative token print cycles) providing a stable yield (~4.6% APY) while allowing users to exit or trade their positions freely on secondary markets.

3. Tokenomic Evolution: The MPL to SYRUP Migration

The economic backbone of the protocol underwent a permanent structural upgrade following a landmark community governance vote (MIP-010).

To position the network for global fintech adoption, Maple completely retired its original token, MPL, replacing it with the SYRUP token. The migration allowed holders to convert assets at a fixed rate of 1 MPL : 100 SYRUP. Following final governance extensions, the conversion window closed permanently on May 21, 2025, leaving legacy MPL and xMPL completely stripped of utility and voting rights.

The Revenue-Driven Value Capture Model

Under the modernized tokenomics framework established by MIP-019, the network eliminated dilutive staking rewards, transitioning to a strict cash-flow model:

The Revenue Split: Instead of printing new tokens to reward holders, the protocol takes exactly 25% of all revenue generated across Maple’s lending pools and channels it directly into the Syrup Strategic Fund (SSF).

Automated Market Buybacks: The fund programmatically uses these corporate interest fees to buy back SYRUP tokens from open decentralized marketplaces, linking the asset's long-term market scarcity to the platform's real loan origination volumes.

Ecosystem Structural Matrix

| Asset / Actor | Target Market | Core Function | Value Sourcing |

| Pool Delegate | Corporate B2B | Underwrites risk | Pool management cuts |

| syrupUSDC | Retail DeFI | Liquid yield wrapper | Corporate loan interest |

| SYRUP Token | Global Governance | Protocol steering | 25% Revenue buybacks |

4. Monitoring Institutional Credit via DEXTools Telemetry

- Evaluating the macroeconomic flows, reserve liquidities, and secondary market valuations of enterprise lending assets requires real-time on-chain data clarity. Sourcing analytics through advanced decentralized charting architectures like DEXTools gives market participants an essential universal platform to monitor live token behaviors, evaluate pool depths, and inspect contract parameters across all public execution networks.

- By leveraging core features like the Pair Explorer, Live New Pairs dashboard, and the integrated Trade Story or Top Traders diagnostic tools, technical traders can seamlessly audit localized volume trends, track large whale wallet capital reallocations via the Big Swap Explorer, and check automated contract safety scores before initiating any on-chain interactions, ensuring your hardened hardware setup interacts safely with verified market venues.

You can access DEXTools here and start trading today!

What Is Maple Finance? Institutional DeFi Lending Guide 2026 RWA Liquidity Quality: Why Tokenized Assets Can Be Real but Still Hard to Trade Top 5 Real World Asset (RWA) Tokens in 2026: Tokenized Finance Goes Mainstream Liquid Bank: Solana Token Pays SOL Rewards to Holders (2026)Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any other kind of advice. DEXTools does not recommend buying, selling, or holding any cryptocurrency or token. Users should conduct their own research and consult with a qualified financial advisor before making any investment decisions. Cryptocurrency investments are volatile and high-risk. DEXTools is not responsible for any losses incurred.

Related Guides

- What Is Maple Finance? Institutional DeFi Lending Guide 2026

- How to Use Silo Finance Isolated Lending 2026

- How to Use Euler Finance: v2 Lending Tutorial (2026)

- Avalanche (AVAX) 2026: The Rise of Institutional L1s

- What Is TrueFi (TRU)? Uncollateralized DeFi Lending and Credit Guide 2026

Frequently Asked Questions

What is Maple Finance?

Maple Finance is a decentralized lending platform focused on connecting capital providers with borrowers, with an emphasis on institutional-style credit. It aims to offer on-chain lending markets that go beyond the heavy over-collateralization typical of many DeFi protocols.

How does institutional lending differ from typical DeFi lending?

Most DeFi lending requires borrowers to lock up more collateral than they borrow, which limits capital efficiency. Institutional lending models often rely on underwriting, reputation, or agreed terms so borrowers can access credit with different collateral arrangements.

What is over-collateralization in DeFi?

Over-collateralization means a borrower must deposit collateral worth more than the loan they take out. This protects lenders against price swings and default, but it ties up large amounts of capital that cannot be used elsewhere.

What are the risks of on-chain lending platforms?

Risks include borrower default, smart contract vulnerabilities, liquidity shortages when many lenders withdraw at once, and reliance on the platform's underwriting or risk controls. Lenders should understand how losses are handled before committing funds.