What Is a Mint Function in Crypto? Guide (2026)

— By Tony Rabbit in Tutorials

Mint function explained: learn how it expands token supply and why ongoing mint permissions are a real dilution and governance risk for investors.

Intent check: This page owns the general concept of a mint function across token contracts and why it affects supply risk. If you want the Solana-specific control surface around who can mint and revoke rights, read What Is Mint Authority on Solana?.

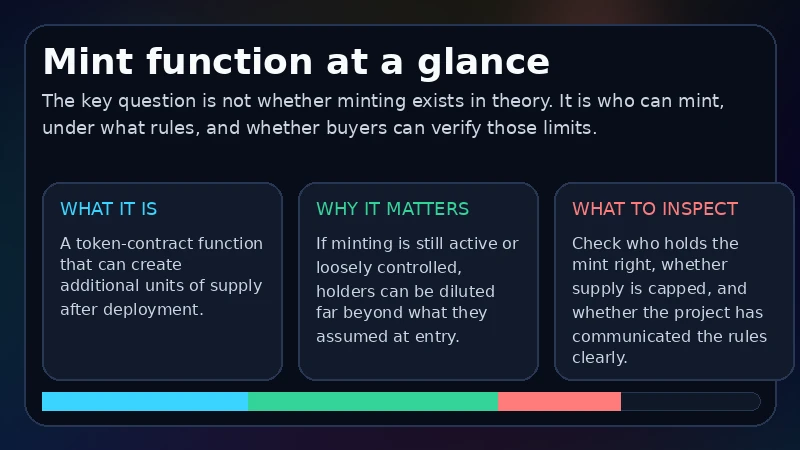

A mint function in crypto is the part of a token contract that allows new tokens to be created after deployment. That sounds technical, but the user-facing consequence is simple: supply can still expand. For buyers, that matters because token price is never just a story about hype or demand. It is also a story about who can create more units and under what constraints.

A lot of traders hear that a token is "mintable" and stop there. That is too shallow. The real questions are whether minting is capped, whether the right still exists, who controls it, and whether the project uses it for normal operations, emissions, or something far more toxic. Those answers determine whether minting is a normal design feature or a live dilution risk.

Quick answer

- A mint function allows a contract to create new tokens after launch.

- The key risk is not minting by itself. The key risk is who controls it and how transparent the limits are.

- Before buying, check whether the token supply is capped, whether the mint right is still active, and how that interacts with FDV, unlocks, and treasury control.

Intent split

- This page is the contract-level mint-right guide: who can create new supply and what that means for holders.

- For the broader concept of a token that can be minted, read What Is a Mintable Token in Crypto?.

- For the Solana-specific control model, read What Is Mint Authority on Solana?.

What the Mint Function Actually Does

In practical terms, a mint function is the mechanism that increases token supply. Sometimes that is expected. Stablecoins may need controlled issuance against reserves. Protocols may use emissions schedules. Projects may mint into treasuries or reward pools. None of that is automatically illegitimate. The problem begins when buyers assume supply is mostly fixed while the contract still allows a privileged actor to expand it later.

That is why contract rights matter as much as token branding. A project can market scarcity aggressively while still holding a live mint path in the contract. If traders only look at current circulating supply and never inspect who controls future issuance, they are reading tokenomics at the surface level instead of the power level.

Why the mint function deserves direct attention

How This Topic Differs From Nearby Tokenomics Pages

Mint function pages can cannibalize with mintable token, mint authority, token unlock, or FDV explainers if they are written too broadly. The clean way to avoid that is to stay centered on the contract right itself. This page is not mainly about scheduled vesting, not mainly about Solana authority design, and not mainly about market-cap math. It is about the existence and control of the mint path.

That distinction helps readers too. Token unlocks describe pre-agreed distribution events. Mint authority on Solana describes a chain-specific permission model. FDV describes a valuation lens. A mint function article answers a more immediate question: can someone still create more units, and if so, what protects the market from abusive issuance?

How the mint-function page fits the supply cluster

How to Inspect Mint Risk Before Buying

Start by treating supply as something you need to verify, not something you inherit from marketing copy. Check the contract, the docs, and any scanner or explorer information that shows whether minting is still possible. Then check who controls the right. A renounced or burned privilege has a different risk profile from an active owner or upgrade admin that can still change behavior.

Then move from raw capability to practical context. If the project can mint, what is the stated reason? Treasury funding, emissions, or collateralized issuance can all be legitimate if the rules are clear and the community understands them. The warning sign is vagueness. If the supply story depends on trust alone, the contract right matters more, not less.

A smarter mint-risk checklist

Common Supply-Analysis Mistakes Around Minting

The biggest mistake is confusing visible distribution with full control. Traders read circulating supply, glance at holder concentration, and stop there. But a contract-level mint path can matter just as much as the current holder table because it defines who gets to change the table later.

Mistakes worth avoiding

Frequently Asked Questions

Q Is a mint function always bad for a token?

No. Some tokens need controlled issuance for legitimate reasons. The risk comes from weak governance, unclear limits, or misleading supply narratives.

Q How is a mint function different from a token unlock?

An unlock releases tokens that already existed but were restricted. Minting creates new supply that was not circulating before.

Q What should I check first on a mintable token?

Check whether minting is still active, who controls it, and whether the stated tokenomics explain that control clearly.

Q Does FDV fully solve mint risk?

Not by itself. FDV is helpful only if the assumptions about total supply and future issuance are realistic and transparent.

Q Why does chain context matter for mint analysis?

Because the control may appear differently depending on the chain. Solana authority models and EVM owner privileges are not presented the same way to the user.